Catch-up Inflation

In recent days, we’ve seen that real median household income in the United States fell for the third year in a row, and that union strike activity is on the upswing. The more well-known strikes include the Hollywood writers and the United Auto Workers. These two things — the fall of real income and the rise of strike activity — are connected.

During the pandemic and shutdown, the government blanketed the country with money bombs. Hundreds of millions of dollars in spending turned into billions, and then billions turned into trillions. As the money spigots were thrown open, the US Treasury started selling its new debt directly to the Federal Reserve for new cash, Latin American-style. This new cash entered the economy and started us on an inflationary spiral. And I remind everybody that this began under Trump.

As the inflation first started to manifest, Treasury and Fed officials claimed the inflation was “transitory,” due to disruptions of the supply chain, bottlenecks, and the hoarding of toilet paper and cleaning supplies. But, as the inflation continued even as the supply chain got put back together, the claim that the inflation was transitory wore thin. The Fed would have to start raising interest rates to choke off the inflation, and the Treasury would have to worry about the implications of rising interest rates for the budget.

I talked about the burst of inflation, mostly unanticipated, in a recent article.

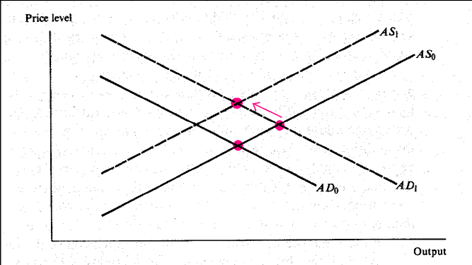

Here, I’ll illustrate what has been happening – and what may soon happen – in a different way. In the following chart, I show Step 1. This step involves a burst of inflation while inflation expectations are well-anchored. The increased spending of the new money increases aggregate demand (from AD0 to AD1), increasing production and employment, and also increasing prices.

Step 1. A burst of inflation when inflation expectations are well-anchored.

Along with the higher prices, workers found their money didn’t go as far as it previously did. Buying Happy Meals, cans of soup, and filling up the tank became challenging. More and more people told survey-takers they couldn’t make ends meet. Consumer confidence started to fall even though unemployment was low.

How dare the American people not embrace Bidenomics!

The next chart shows Step 2. This is when workers start to act on the burst of inflation. Where there is collective bargaining, workers go on strike to demand higher wages in order to catch-up to inflation. Elsewhere in the economy, individual workers bargain for higher wages with their current employer, or begin searching for better-paying jobs. Companies find they have to deal with the problem of “compression,” meaning paying pimply-faced new hires more than their seasoned-veterans, a situation that can only last so long.

But notice that as a result of wages catching-up, there is further inflation, and workers might not actually regain their former purchasing power. This is another period of frustration.

Step 2. Workers notice they’ve lost purchasing power to inflation and seek higher wages.

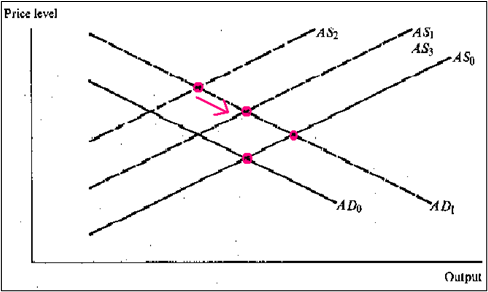

We now come to Step 3, shown in the next chart. Workers seek yet higher wages since they now expect inflation to continue. But, Step 3 is a doozy. It involves a reduction of production and employment from their normal levels. We risk slipping on Step 3 and falling into a recession. This is where we are now. I’ve been predicting a recession for a while. The recession is overdue. But maybe the economy will just continue to sputter along at a slow rate of growth, and we settle into the equilibrium defined by AD1 and AS1, shown in Step 2, and not go to Step 3.

Step 3. Inflation expectations become persistent.

Should we actually fall into a recession, we have to eventually recover from it. This will occur when workers moderate their wage demands. So, if we have a Step 3, we will eventually have a Step 4. In 1984, this was called “Morning in America.”

Step 4. Unemployment sobers up the labor market.

Clifford F. Thies

Clifford F. Thies is a Professor of Economics and Finance at Shenandoah University, He is the author, co-author, contributor and editor of more than a hundred books, encyclopedia entries and articles in scholarly journals.

He is a member of the editorial board of the Journal of Private Enterprise and is a former Bradley Resident Scholar at the Heritage Foundation. He is a past president of the faculty senates of Shenandoah University and the University of Baltimore. He also served in the U.S. Army and the Army Reserve.