Retail Sales Plunge in March

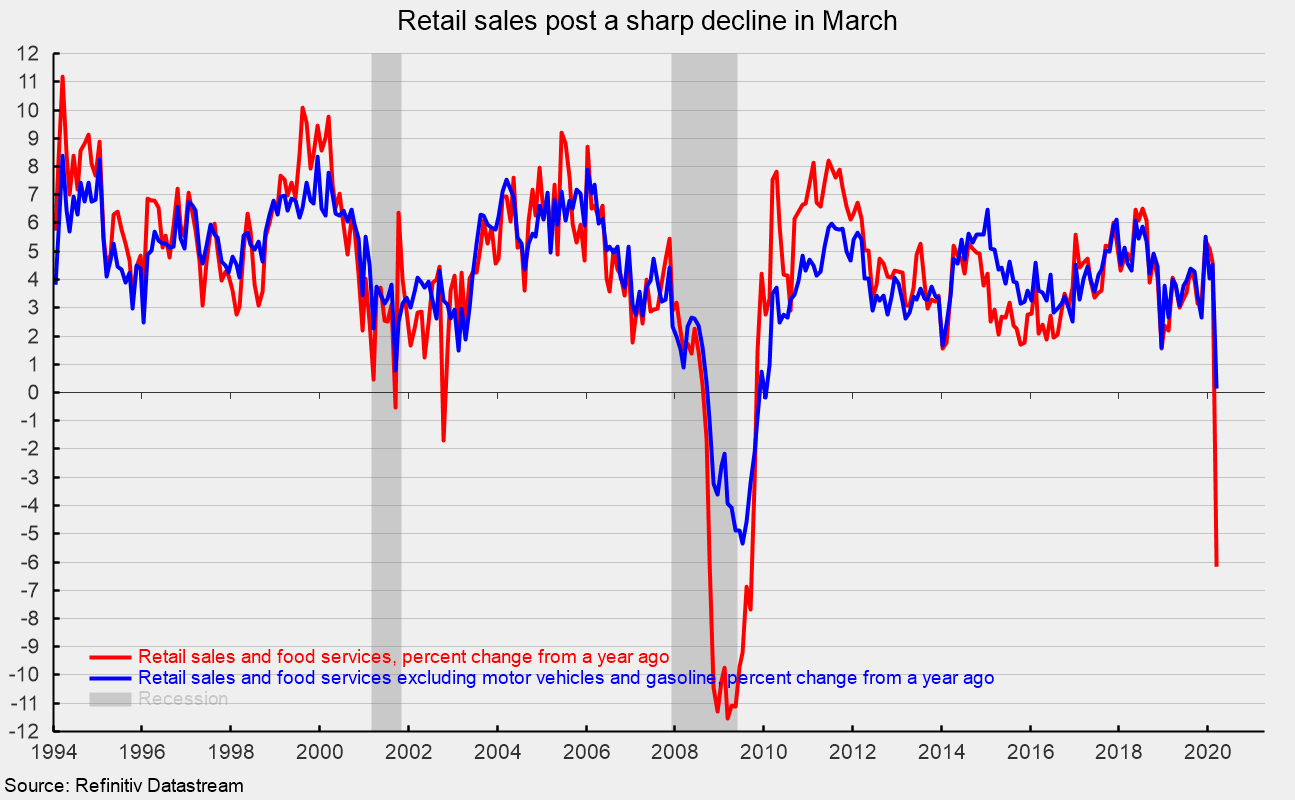

Retail sales and food-services spending plunged 8.7 percent in March following a 0.4 percent drop in February. Excluding the volatile auto and energy categories, core retail sales and food services were down 3.1 percent in March after a fall of 0.2 percent in February. Over the past year, total retail sales and food services were down 6.2 percent through March, the worst performance since September 2009, while core retail sales and food services have increased 0.2 percent, the slowest pace since January 2010 (see first chart).

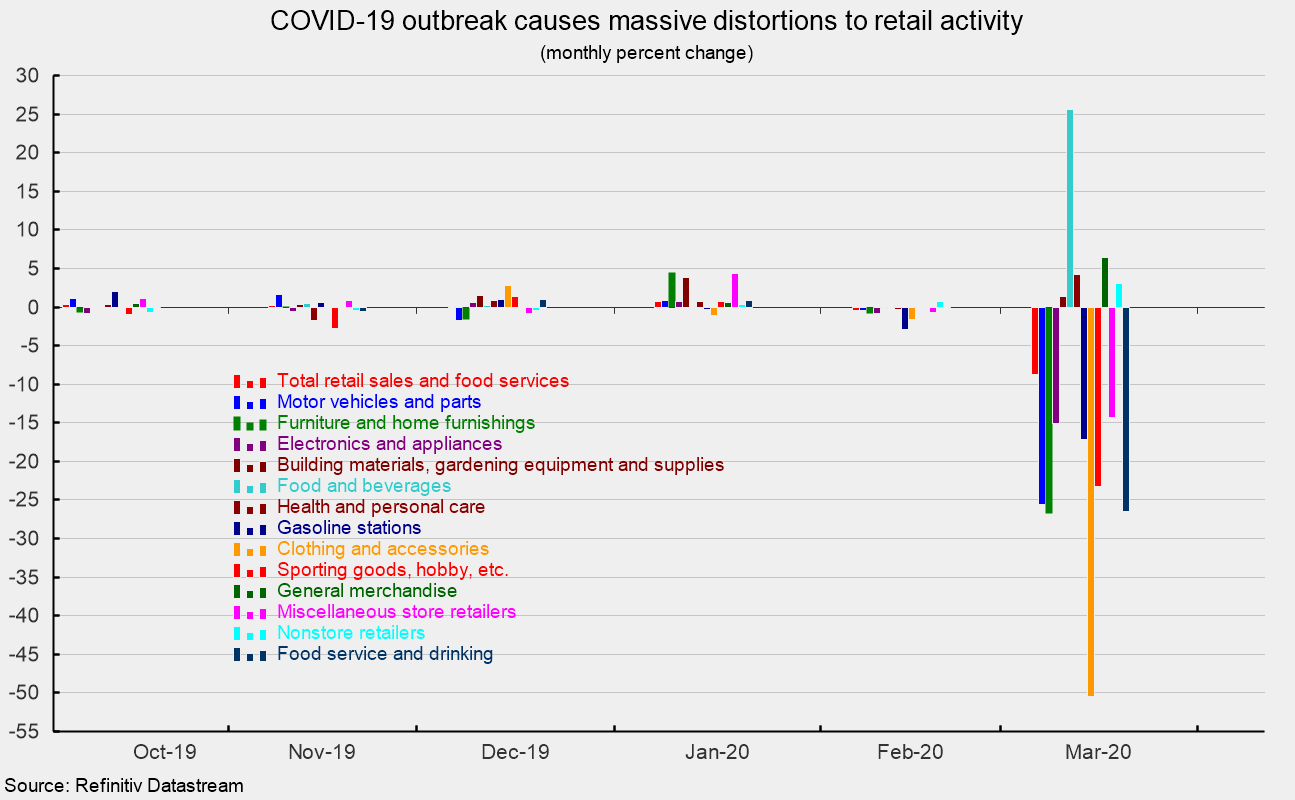

Industry performance in March was extremely diverse as the COVID-19 outbreak caused massive disruptions to economic activity. There were declines in eight retail-spending categories, with all eight posting double-digit declines. Five categories posted gains with one posting a double-digit pace (see second chart). Declines were led by a 50.5 percent drop for clothing and accessory stores, followed by a 26.8 percent fall for furniture and home furnishings, a 26.5 percent decline for food services, 25.6 percent drop for motor vehicle and motor vehicle–parts dealers, a 23.3 percent drop in sporting-goods, hobby, musical-instrument, and bookstores, a 17.2 percent decline for gas station sales, a 15.1 percent decline for electronics and appliance stores, and a 14.3 percent decrease for miscellaneous store sales.

On the positive side, there was a 25.6 percent surge for food and beverage stores, general merchandise store sales rose gained 6.4 percent, health and personal care store sales increased 4.3 percent, nonstore retail sales rose 3.1 percent, and there was a 1.3 percent gain for building-material, garden-equipment, and garden-supplies dealers.

Retail sales were sharply weaker in aggregate in March. However, industry performance varied widely. Retail sales are likely to show significant weakness in April as the effects of widespread quarantines and lockdowns continue. Businesses and consumers may adapt somewhat but a full recovery is unlikely to occur for several months.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.