MMT’s Inflation Battle Will End In A Draw

Charles Goodhart, a brilliant banking historian and professor at the London School of Economics, recently said that “I have never seen a theory so criticized, in theory, and actually followed in practice.” He was talking about MMT, Modern Monetary Theory.

Some of last year’s pandemic measures, and even more so the latest $1.9 trillion deficit-funded package, look suspiciously like an MMT moment: fiscal policy is willing to shower money on anything and everything they like, while everyone else worries about inflation numbers. The Federal Reserve backstops the bond market by buying hundreds of billions worth of bonds every month. Unbelievably large, and largely unprecedented, the Federal government deficit last year (over $3 trillion and on track to rival that this year), has the Treasure wrestling economic control from an otherwise supreme central bank.

In a recent interview on Bloomberg’s Odd Lots podcast, Stephanie Kelton, one of this fringe economic theory’s foremost proponents, responded to co-host Tracy Alloway’s question about what would make her reconsider the MMT position. The answer: “If all these stimulus packages were passed by Congress and the checks somehow bounced.”

What she means, technically, is that the Treasury General Account (TGA) at the Fed could go as negative as Congress wants it to. If it doesn’t, that is if the Fed doesn’t allow the Treasury an overdraft – let alone an unlimited such – MMT’s supposedly objective description of the world is undermined.

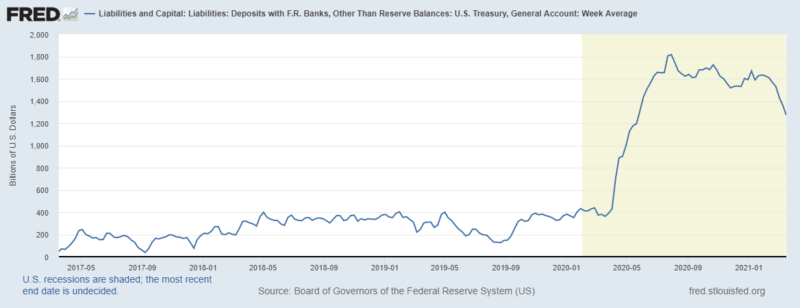

What’s revealing about this interchange is that it also undermines the narrative of 2020 and 2021 as an MMT moment; we haven’t had the ultimate test of the theory, and the TGA balance tells us so:

For a vindication of the MMT position, we need (large) government expenditures not pre-funded by taxation or debt issued on the bond market.

During 2020, the Treasury, anticipating large government stimulus, issued more debt than needed to fund the government deficit – to the tune of about a trillion-and-a-half. This is public finance as usual, not an MMT revolution. At the same time, the Fed was purchasing outstanding bonds at two or three times its current rate, explosively increasing its balance sheet from around $4 trillion before the pandemic to around $7.7 trillion today. The result was a piling up of reserves, both in the TGA account and at commercial banks’ account at the Fed:

With the new round of stimulus rolled out in the beginning of 2021, the TGA balance has already fallen by about $600 billion since January, mechanically increasing commercial banks’ deposits as the newfound money arrives to households. We have some way left for Kelton’s own MMT test to even come into play.

More importantly, nothing but the size in last year’s policies is unconventional from standard macroeconomic theory and models. In a review article for Economic Affairs, I wrote “A charitable interpretation turns MMT policy proposals into a garden-variety counter-cyclical Keynesianism under conditions of large output gaps.” We are in a situation of large output gaps, albeit self-imposed and engineered by a government throwing everything and the kitchen sink against a comparatively mild virus – to the detriment of any other concerns.

What Kelton, whose popular book was written before the pandemic, favors are these sorts of extreme government policies at times when unemployment was an endangered species and labor force participation increased after falling for a decade or more. The real test of MMT is to throw $3 trillion stimulus packages at that kind of economy.

Will We Have Hyperinflation?

No. Only because Ms. Kelton’s position is so far not vindicated, despite the stars aligning, we shouldn’t conclude that her most staunch opponents – those chanting “hyperinflation” in increasingly synchronous chorus – are therefore right. Most likely, we’ll end up somewhere in between.

Even though monetary aggregates like M2 stand 26% above its pre-pandemic level, velocity – how quickly that stock of money, new and old, churns – was at least 30% below its already-depressed pre-pandemic level. If the left-hand-side of the equation of exchange (M*V = P*Y) is roughly constant, nothing much happens in the real economy – at least that we can blame on the money markets. The inflation thesis ultimately hinges on velocity returning, either to where it was before March 2020 – or to its high points in the 1990s or before the financial crisis.

Right now, households have bloated savings accounts but aren’t spending and banks are flushed with reserves but aren’t lending. For the inflation thesis to play out, this has to reverse: consumers have to buy things; banks have to lend, or at least buy assets in a way they are reluctant to do (and might not be regulatorily allowed to).

And even that’s not enough, as once any such a move starts to overshoot the Fed’s tolerance for inflation, it’s unlikely that the FOMC rate-setting members will stomach very much. While the Fed can’t directly affect velocity, it can scoop up enough liquidity in the banking system to have the same effect.

What households have done with the stimulus checks so far is also weighing against a return of massive inflation: they used much of it to pay down debt, making a sudden return of a spending spree somewhat less likely.

In a way, 2021 has echoes of the Great Inflation Debate from the years after the financial crisis. Very similar arguments, often advanced by the same people, are voiced today. That time, following the extremely fast and large expansion of the Fed’s balance sheet and the monetary base, the inflation threat that people like Peter Schiff and Bob Murphy projected didn’t manifest itself. It didn’t emerge, precisely for the same reason that the stimulus doves (the Paul Krugmans or Janet Yellens of the world) were thwarted in the labor market wonders they envisioned: the new money didn’t go where they thought it would.

In the years after 2008, the Federal Reserve’s policy of paying interest on excess reserves above similar market rates scooped up much of the large increases in money supply – and the new money just sat at the commercial banks’ account with the Federal Reserve, earning a nice and safe interest on their excess reserves. We didn’t get the inflation pop projected from watching the money supply increase, but we also didn’t get the stimulus that the policy wonks hoped for.

The inflation debates of 2020-2021 feels a little like Groundhog Day. Unless the new money finds a way to exit en masse, we won’t get the stimulus effect that the Biden administration hopes for – but also not the inflation that deficit hawks fear.

It’s tempting to cry wolf when Fed and Treasury actions seem to be beyond all proportion. Maybe this time is different, and perhaps this is the turning point – for MMT or for inflation. More likely, the fears and the ebullient promises will converge in a middle-of-the-way third option similar to what we saw after 2008: Politicians, pundits, economists, and central bankers talk, yet nothing much happens.

Joakim Book

Joakim Book is a writer, researcher and editor on all things money, finance and financial history. He holds a masters degree from the University of Oxford and has been a visiting scholar at the American Institute for Economic Research in 2018 and 2019.

His work has been featured in the Financial Times, FT Alphaville, Neue Zürcher Zeitung, Svenska Dagbladet, Zero Hedge, The Property Chronicle and many other outlets. He is a regular contributor and co-founder of the Swedish liberty site Cospaia.se, and a frequent writer at CapX, NotesOnLiberty, and HumanProgress.org.