May 2020 Business Conditions Monthly

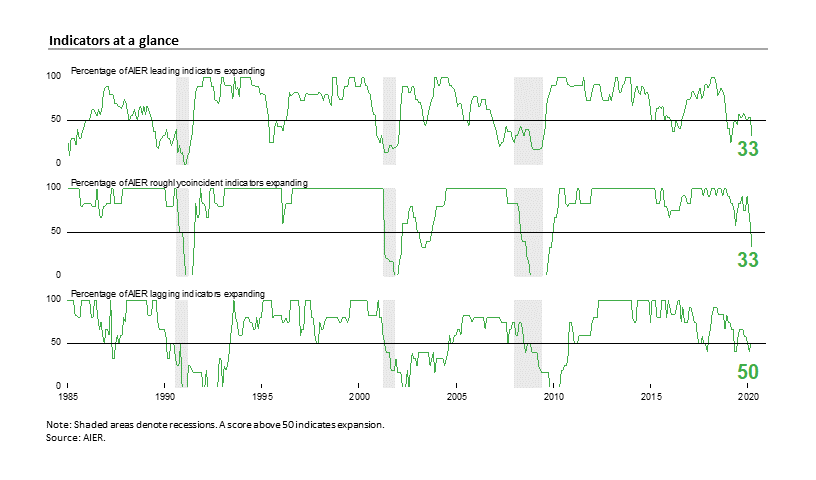

AIER’s Leading and Roughly Coincident Indicators Indexes Drop to 33.

AIER’s Business Cycle Conditions Leading Indicators index and Roughly Coincident Indicators Index both dropped to 33 in April. The Roughly Coincident Indicators index is at its lowest level since December 2009, just after the end of the Great Recession (see chart). The latest results provide additional evidence that the U.S. economy has likely entered a recession, ending the longest U.S. economic expansion on record.

The plunge in economic activity and devastation caused to the labor market is a result of COVID-19 and subsequent Federal and state policy responses. Government mandates to close nonessential businesses and require people to shelter-in-place in order to contain the spread of COVID-19 has resulted in unprecedented job losses, plunging sales in many industries, and sharply rising risks of personal bankruptcies, small business closures, and loan and bond defaults across the economy.

In response, the Federal government has enacted multi-trillion-dollar efforts to support consumers and businesses while the Federal Reserve has driven interest rates down close to zero and resumed and expanded bond-buying programs from the Great Recession. The recovery path of the economy and labor market remain dependent on the pace of normalization and extent of the damage done to the economy.

Leading and Roughly Coincident indicators indexes fall well below neutral in April

The AIER Leading Indicators index was 33 in April, down from 54 in the prior month while the Roughly Coincident Indicators index fell to 33 from 58 in March. April was the first month since August 2009 that both indexes were below the neutral 50 threshold.

Overall, just 3 of the 12 leading indicators maintained a positive trend in April compared to 5 in March, while 7 were trending lower versus 4 in the prior month, and 2 indicators were neutral, down from 3 previously. Initial claims for unemployment insurance have been making headlines for the past six weeks, shattering previous levels. In just six weeks, more than 30 million people have filed for unemployment insurance. For comparison, the entire drop in payroll employment during the Great Recession totaled less than 9 million from peak to trough. The surge in claims pushed the trend from positive last month to a negative trend in the latest period.

Among the other leading indicators, the University of Michigan index of consumer expectations moved from a neutral trend last month to a negative trend as did real retail sales and food services. Real new orders for consumer goods dropped from a positive trend to a neutral trend.

The roughly coincident indicators fell to 33 in April, down 25 points from 58 in March following 17-point drops in each of the prior two months, making the three-month change a whopping 59-point plunge. Two indicators changed direction in April. The real personal income excluding transfers indicator fell to a negative trend from a positive trend in the prior month while the industrial production indicator fell from neutral to a negative trend. Overall, two indicators were still trending higher, four were trending lower and none were neutral versus three trending higher, three trending lower and no neutrals in March.

Overall, the weak results for both the Leading Indicators index and the Roughly Coincident Indicators index suggest the economy is likely in recession. Furthermore, government mandates for shuttering of nonessential businesses and sheltering-in-place for workers and consumers are an unprecedented source for economic disruption and recession, at least in modern U.S. economic history. Historical analysis is unlikely to provide useful guides for depth and duration of the current contraction. Rather, careful monitoring of progress in understanding and treating COVID-19, the progression of the lifting of restrictive policies (normalization), and the destructive impacts across the economy and financial system are likely to be the most useful source of information.

AIER’s Lagging Indicators index was unchanged in the latest month, holding at a reading of 50 in April. Three indicators had net offsetting changes in April, leaving two indicators trending higher, two trending lower, and two neutral.

Measuring the COVID-19 Recession

Real gross domestic product fell at a 4.8 percent annualized rate in the first quarter, down sharply from a mediocre 2.1 percent pace in the fourth quarter of 2019, the worst performance since the final quarter of 2008 when the economy plunged 8.4 percent. Over the past four quarters, real gross domestic product is up just 0.3 percent, the slowest pace since the final quarter of 2009. On a nominal basis, gross domestic product fell 3.5 percent in the first quarter, putting the change from a year ago at 2.1 percent.

Declines were widespread across the different areas of the economy though there were a few positives. Consumer spending declined sharply in the first quarter, falling at a 7.6 percent pace compared to a 1.8 percent growth rate in the fourth quarter. The decline was the result of sharp drops in spending on durable-goods (down 16.1 percent) and services (-10.2 percent) partially offset by nondurable-goods spending which rose at a 6.9 percent pace in the first quarter versus a 0.6 percent drop in the previous quarter. Within the gain in nondurables, food and beverages spending surged 25.1 percent and the catchall other nondurable goods category jumped 12.9 percent while spending on clothing and shoes tumbled 36.0 percent and gasoline and other energy goods spending dropped 5.5 percent. Within the consumer services category, medical care, transportation, recreation, and food services and accommodation all posted sharp double-digit declines.

Business investment fell at an 8.6 percent annualized rate in the first quarter of 2020. That decline was led by a 15.2 percent fall in spending on equipment while spending on structures fell 9.7 percent. Intellectual-property investment rose 0.4 percent versus a 2.8 percent gain in the previous quarter. The first quarter rise was all due to an 8.2 percent increase in software while spending on research and development and entertainment, literary and artistic intellectual property posted declines.

Residential investment, or housing, jumped 21.0 percent in the first quarter compared to a 6.5 percent gain in the prior quarter. Housing has increased for three straight quarters though gains are unlikely to continue in the second quarter.

Businesses liquidated inventory in the first quarter, subtracting 0.53 percentage points from first-quarter growth after subtracting 0.98 percentage points in the prior quarter. Inventory liquidation has reduced real gross domestic product for four consecutive quarters.

Exports declined at an 8.7 percent pace, subtracting 1.02 percentage points, while imports declined at a 15.3 percent rate. Since imports count as a negative in the calculation of gross domestic product, a drop in imports is a positive for GDP growth. Net trade, as used in the calculation of gross domestic product, added 1.3 percentage points to overall growth.

Government spending rose at a 0.7 percent annualized rate in the first quarter compared to a 2.5 percent gain in the fourth quarter, contributing 0.13 percentage points to growth versus a 0.44-point contribution in the final quarter of last year. Within that total, federal government spending rose 1.7 percent while state and local governments saw a 0.1 percent rise.

Real final sales to private domestic purchasers, a key measure of private domestic demand, fell at a 6.6 percent annualized rate in the first quarter, versus a 1.4 percent rise in the fourth quarter. Over the past four quarters, real private domestic demand is unchanged.

Consumer price measures were subdued in the first quarter. The personal-consumption price index rose at a 1.3 percent annualized rate, down from a 1.4 percent pace in the fourth quarter. From a year ago, the index is up 1.6 percent, well below the Federal Reserve’s 2 percent target. Excluding the volatile food and energy categories, the core PCE (personal consumption expenditures) index rose at a 1.8 percent pace. From a year ago, the core PCE index is up 1.8 percent and has been at or below 2 percent since 2012.

Overall, the first quarter saw a plunge in real gross domestic product along with surging unemployment and a collapse in consumer attitudes. While there are some early efforts to return to normal life, the process appears to be slow, suggesting that second quarter economic growth is also likely to be sharply distorted.

Initial claims slowing but still enormous

Initial claims for unemployment insurance totaled 3.8 million for the week ending April 25. However, on a somewhat positive note, the latest tally is the fourth week of declines in the number of initial claims since the 6.87 million claims during the week of March 28.

Initial claims for unemployment insurance have totaled more than 30 million over the last six weeks. To help put these numbers in perspective, during the Great Recession in 2008-09, total payroll job losses were 8.8 million over 25 months. The peak number of unemployed people for the Great Recession, as measured in the household survey portion of the monthly Employment Situation report, actually occurred in October 2009, four months after the official end of the recession, and was 15.4 million.

As of the March 2020 Employment Situation report, there were 7.1 million unemployed in the United States, resulting in an unemployment rate of 4.4 percent. The April report is due out on Friday, May 8. Current consensus estimates are for payrolls to drop by 20 million and the unemployment rate to surge to 14 percent. The previous cycle peak in the unemployment rate was 10 percent in October 2009 while the highest unemployment rate since 1950 came in November 1982 at 10.7 percent. Though data collection was much less reliable, the unemployment rate following the Great Depression was estimated to have peaked at 25 percent in 1933.

Consumer surveys are down sharply

The Consumer Confidence Index from The Conference Board fell sharply again in April, dropping 31.9 points to 86.9, the lowest level since June 2014. The drop was driven by the present situation component. The present-situation component fell to 76.4 from 166.7, the lowest since December 2013. The April drop of 90 points is the largest on record. The expectations component gained 7 points to 93.8 from 86.8 in the prior month.

According to The Conference Board report, “Consumer confidence weakened significantly in April, driven by a severe deterioration in current conditions. The 90-point drop in the Present Situation Index, the largest on record, reflects the sharp contraction in economic activity and surge in unemployment claims brought about by the COVID-19 crisis. Consumers’ short-term expectations for the economy and labor market improved, likely prompted by the possibility that stay-at-home restrictions will loosen soon, along with a re-opening of the economy. However, consumers were less optimistic about their financial prospects and this could have repercussions for spending as the recovery takes hold. The uncertainty of the economic effects of COVID-19 will likely cause expectations to fluctuate in the months ahead.”

The Conference Board results are mostly in line with the final results from the University of Michigan. The final April results from the University of Michigan Surveys of Consumers show overall consumer sentiment fell sharply from the final March result, registering the second double-digit percentage decline in a row. Consumer sentiment decreased to 71.8 in April, down from 89.1 in March, a 19.4 percent decline. From a year ago, the index is down 26.1 percent. March and April combined show a two-month drop of 29.2 Index-points.

Both sub-indexes in the University of Michigan survey posted sharp declines in April. First, the current-economic-conditions index dropped to 74.3 from 103.7 in March. That is a 29.4 point or 28.4 percent decline following a 9.7 percent fall in March. From a year ago, the current conditions index is down 33.8 percent.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — sank a much-less-severe 9.6 points or 12.0 percent for the month to a reading of 70.1 and is 19.8 percent below the prior year. While the 12.0-point decline puts the index at the lowest level since March 2014, the less severe drop in the expectations index relative to the current conditions index perhaps indicates an underlying optimism about the future.

According to the University of Michigan report, “While the decline in both indices indicates an ongoing recession, the gap reflects the anticipated cyclical nature of the coronavirus. In the weeks ahead, as several states reopen their economies, more information will reach consumers about how reopening could cause a resurgence in coronavirus infections. Consumers’ reactions to relaxing restrictions will be critical, either putting further pressure on states to reopen their economies or exerting added pressure to extend the restrictions even if it has negative consequences for economic prospects. The risks associated with these decisions are not equally balanced, with an incorrect decision to reopen having serious repercussions. The necessity to reimpose restrictions could cause a deeper and more lasting pessimism across all consumers, even those in states that did not relax their restrictions.”

Retail sales growth plunged to lowest level since 2009

Retail sales and food-services spending plunged 8.7 percent in March following a 0.4 percent drop in February. Excluding the volatile auto and energy categories, core retail sales and food services were down 3.1 percent in March after a fall of 0.2 percent in February. Over the past year, total retail sales and food services were down 6.2 percent through March, the worst performance since September 2009, while core retail sales and food services have increased 0.2 percent, the slowest pace since January 2010.

Unit auto sales continued to drop in April

Sales of light vehicles totaled 8.6 million at an annual rate in April, down sharply again from an 11.4 million pace in March and a 16.8 million pace in February. The pace of sales in April is lower than the 9.0 million trough from February 2009 during the Great Recession, and is about half the 17-million average pace over the last five years.

For the month of April, light-truck sales totaled 6.6 million at an annual rate, while cars managed just 1.9 million, the lowest on record going back to 1967. That puts the light-truck share at 77.3 percent, a new record high and completely dominating the car share of 22.7 percent.

Manufacturing-sector struggles worsen

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell to a 41.5 percent reading in April, down from 49.1 percent in March. Overall, the report notes, “Comments from the panel were strongly negative (three negative comments for every one positive comment) regarding the near-term outlook, with sentiment clearly impacted by the coronavirus (COVID-19) pandemic and continuing energy market recession. The PMI indicates a level of manufacturing-sector contraction not seen since April 2009, with a strongly negative trajectory.”

Many of the key components of the Purchasing Managers’ Index have already fallen to levels not seen since the lows of the Great Recession in 2008-09. The New Orders Index came in at 27.1 percent, down from 42.2 percent in March and the lowest since December 2008; the New Export Orders Index came in at 35.3 percent in April, down 11.3 percentage points from a 46.6 percent result in March; the production index was at 27.5 percent in April, down from 47.7 percent in March and a new record low since the survey began in 1948; and the employment index fell 16.3 percentage points to 27.5 percent in April, versus 43.8 percent in March, and the lowest reading since June 1949.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.