Did Government Red Ink Make the US More Dynamic than Europe?

I like to entertain seriously views I disagree with, but it’s hard to describe a new hypothesis on the left about the United States’ economic dynamism relative to Europe’s as anything other than “cockamamie.” The claim from Rogé Karma in The Atlantic is that “the US economy is doing spectacularly well,” and the reason for this performance is that America is “stealing from Europe’s big-government, welfare-state playbook.” By spending $5 trillion on pandemic relief, but letting people lose their jobs, so the argument goes, the US shuffled the labor market and got people into better, more productive jobs:

This labor-market reshuffling, argues Adam Posen, the president of the Peterson Institute for International Economics, is the most plausible explanation for why American workers experienced a sudden spike in productivity in the second half of 2023 — one that didn’t occur in Europe. ‘The pandemic response convinced people that government ultimately had their back,’ Posen told me. ‘And that allowed people to take bigger risks than normal.’

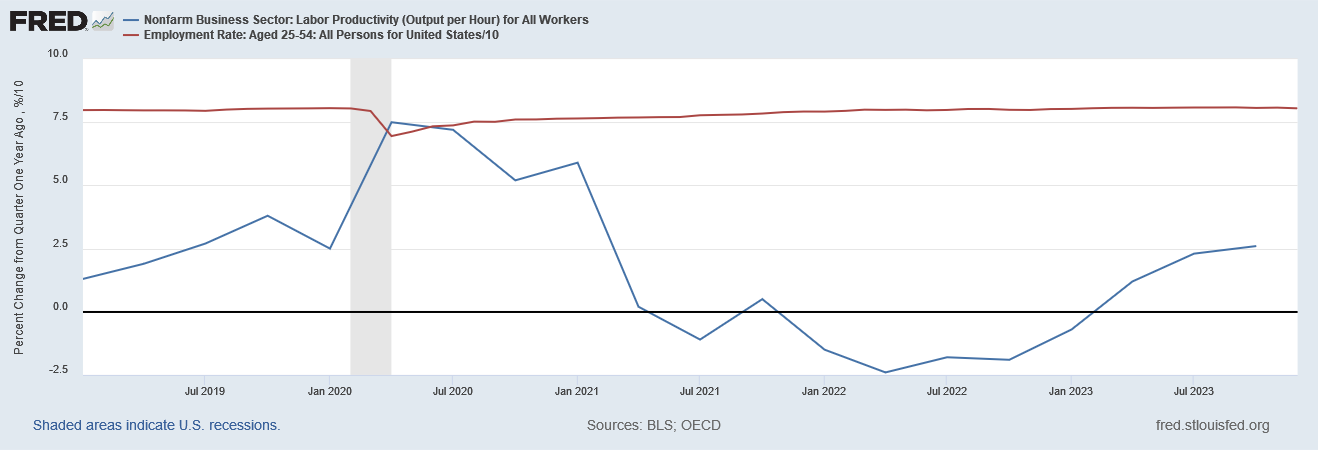

Let’s look at the evidence. If this theory is right, then productivity should have spiked just after Americans returned to work. The figure below plots percent change over the previous year in real output per hour, from the first quarter of 2019 to the fourth quarter of 2023, alongside the prime-age employment rate. We do indeed see productivity increasing in the latter half of 2023.

But what’s happening with the employment rate? It has recovered almost all of its pandemic losses by March 2022. Total quits also peaked in April 2022, implying that the job market reshuffling started slowing down then. It’s pretty arbitrary to attribute the productivity growth in 2023 to job reshuffling, when the latter process was more than 90 percent complete a year and a half before. More likely, falling inflation is the dominant reason productivity grew in late 2023.

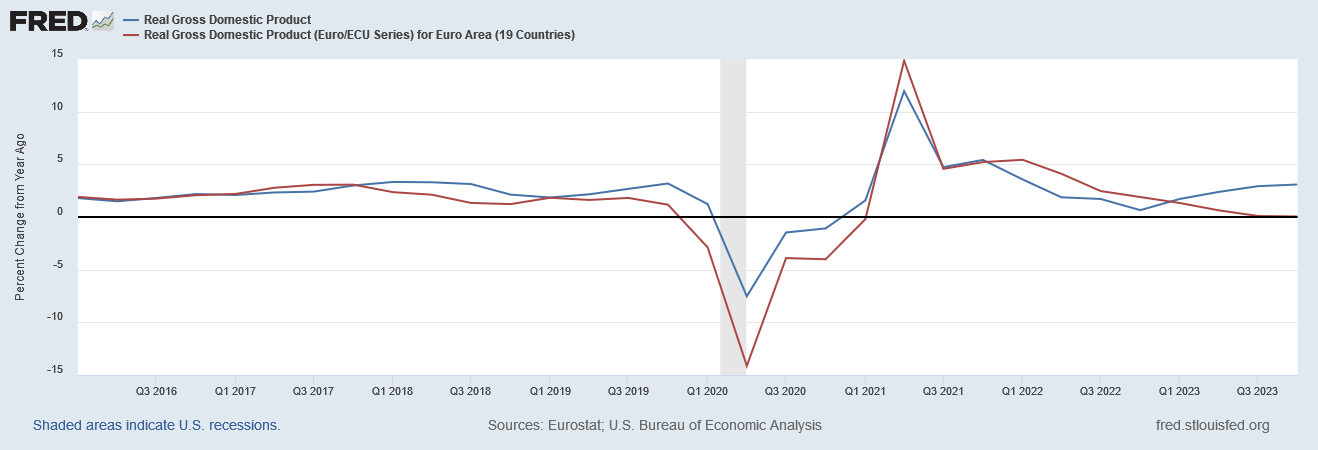

The other piece of evidence that fits poorly with Karma’s claim is the fact that the US has been more dynamic than Europe for a long time. The figure below plots real GDP growth (percentage change from a year ago) for both the US and the Eurozone.

How can anyone look at these numbers and say that pandemic spending is what caused the US to outpace Europe? From Q4 2017 through Q1 2021 — 14 consecutive quarters — US growth beat the Eurozone’s. Then, from Q2 2021 through Q4 2022, with the sole exception of two quarters, the Eurozone outpaced the US. Only in the four quarters of 2023 has the US again taken a lead on the Eurozone. A more natural reading is that the US generally has higher growth than the Eurozone, but something happened in 2021 and 2022 to disrupt that usual pattern. One could as easily make the case that large federal deficits and inflation hurt the US relative to Europe.

Taking a step back, it’s hard for me to reconcile this new “social democratic” interpretation of the pandemic with the way that social democrats have interpreted, well, just about everything else. They want to say that mass unemployment was good this time because it allowed people to quickly find new jobs where they were more productive. That sounds a lot like the “liquidationist” perspective that influenced the Fed in the late 1920s as it crushed the stock market boom. Do Karma and Posen think that the Fed should be celebrated for having responded too late to the Great Recession that hit in 2008? That we should welcome a big financial crisis now and then? Was the Fed justified in letting the US slip into depression in the early 1930s?

Now, presumably, they would respond that mass unemployment is only good if people can get rehired quickly, which wasn’t the case during the Great Depression, nor the Great Recession. Still, the logic suggests that the workers would be better off if government periodically encouraged employers to fire many of their workers to help “reshuffle” the labor market.

On theoretical grounds, the hypothesis makes little sense either. Do businesses really keep around workers who are making a lot less than their marginal product for a long time? Do people really give up on growing in their career once they have a job?

The new “reshuffling” thesis of American recovery doesn’t make much sense on the evidence or economic theory. It serves a convenient political purpose in helping to justify massive federal stimulus that otherwise looks like a costly waste, ahead of an election, but that’s about all that can be said for it.

For sources of American economic recovery, let’s look instead at the belated recovery of macroeconomic stability, which has allowed America’s natural dynamism to come through.

Jason Sorens

Jason Sorens, Ph.D., is Senior Research Fellow at AIER. He is also Principal Investigator on the New Hampshire Zoning Atlas. Jason was formerly the director of the Center for Ethics in Society at Saint Anselm College. He has researched and written more than 20 peer‐reviewed journal articles, a book for McGill‐Queens University Press titled Secessionism, and a biennially revised book for the Cato Institute, Freedom in the 50 States (with William Ruger).

His research is focused on housing policy and land-use regulation, U.S. state politics, fiscal federalism, and movements for regional autonomy and independence around the world. He has taught at Yale, Dartmouth, and the University at Buffalo and twice won awards for best teaching in his department. He lives in Amherst, New Hampshire.