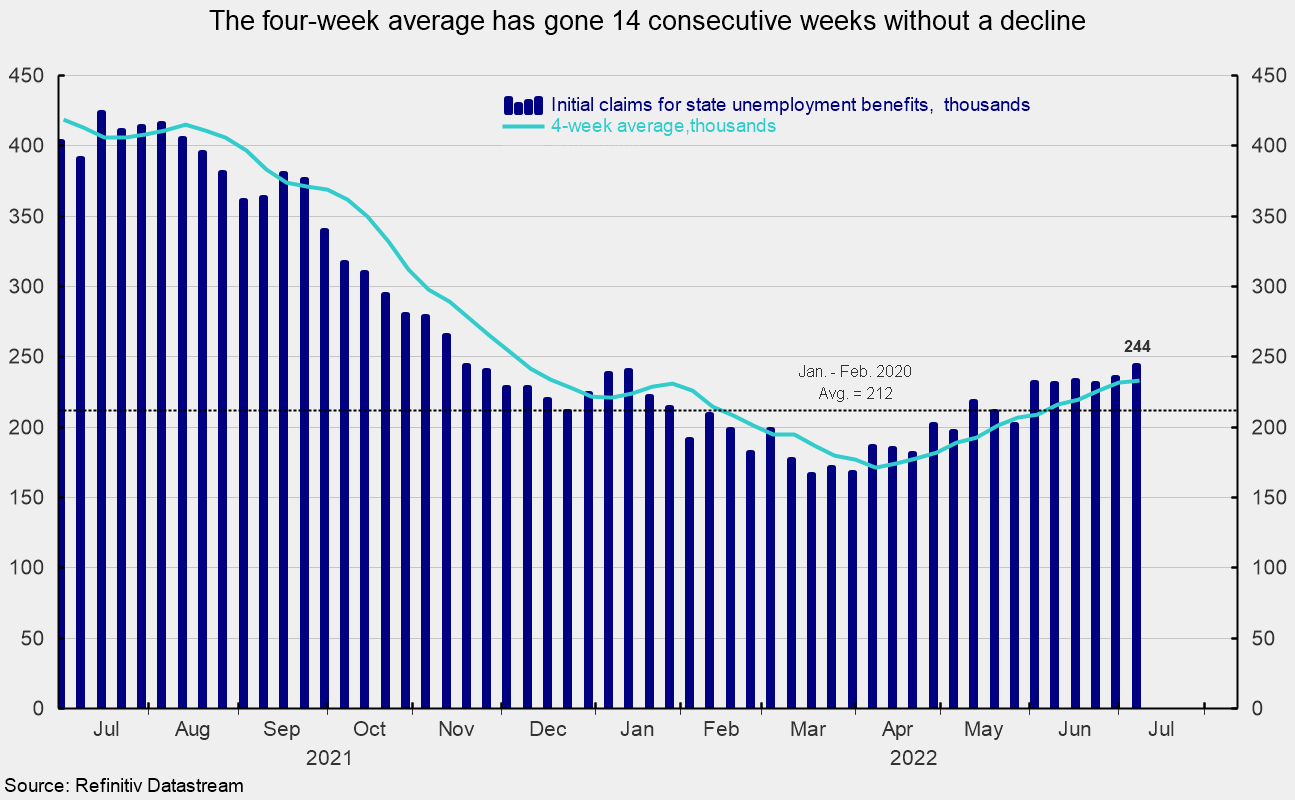

Weekly Initial Claims Rise to the Highest Level Since November

Initial claims for regular state unemployment insurance rose 9,000 for the week ending July 9th, coming in at 244,000. The previous week’s 235,000 was unrevised from the initial tally (see first chart). Weekly claims are at the highest level since November 20th. However, by long-term historical comparison, initial claims remain very low. The four-week average rose for the thirteenth time in the last fourteen weeks (the four-week average was unchanged in one week), coming in at 235,750, up 3,250 from the prior week and at the highest level since February 19th. Weekly initial claims data continue to suggest a very tight labor market, though the recent upward trend is a growing concern. Sustained elevated rates of price increases, an intensifying Fed tightening cycle, and fallout from the Russian invasion of Ukraine represent risks to the economic outlook.

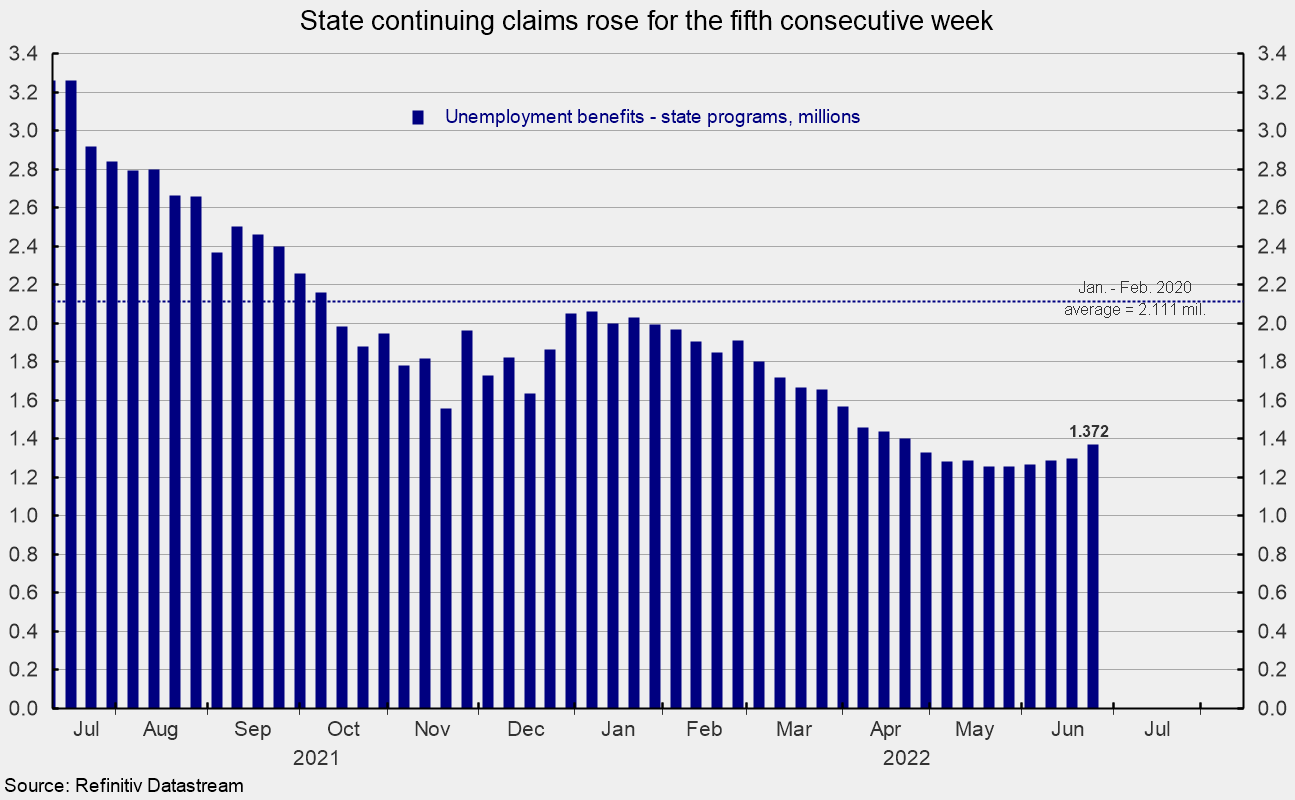

The number of ongoing claims for state unemployment programs totaled 1.372 million for the week ending June 25th, a rise of 72,968 from the prior week (see second chart). State continuing claims have now risen in six of the last seven weeks and are at the highest level since April 23rd, though the level remains very low by longer-term comparison (see second chart).

The latest results for the combined Federal and state programs put the total number of people claiming benefits in all unemployment programs at 1.400 million for the week ended June 25th, an increase of 72,511 from the prior week. The latest result is the highest since April 23rd but is the twentieth week in a row below 2 million.

Initial claims remain at a very low level by historical comparison, but recent weeks have seen a clear upward trend. Weekly initial claims for unemployment insurance is an AIER leading indicator, and if the trend continues on an upward trajectory, it may be an early warning sign. Furthermore, the number of open jobs in the country has receded for two consecutive months, though the level remains very high by historical comparison.

While the overall low level of claims combined with the high number of open jobs suggest the labor market remains very tight, both measures are showing signs of softening. The tight labor market is a crucial component of the economy, providing support for consumer spending. However, persistently elevated rates of price increases already weigh on consumer attitudes, and if consumers lose confidence in the tight labor market, they may significantly reduce spending. The outlook remains highly uncertain.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.