Your Signature No Longer Matters

All the major credit card companies have announced that they will no longer be requiring signatures at the point of purchase. “Later this month, four of the largest networks — American Express, Discover, Mastercard and Visa — will stop requiring them to complete card transactions,” reports the New York Times.

This is to confirm what you have probably already discerned: your signature is no longer a useful guarantor of your identity. What is? Well, the other day at the airport, I had the creepy experience of having my personal identity at the airport confirmed by Delta’s Clear system via a retina scan. I stared into a small camera and my identity popped up on a screen. I didn’t know whether to be impressed or alarmed, but it did happen.

In other cases, it is all about what we know: last four digits of the social security number, the zip code, a passphrase or PIN number, mother’s maiden name, and so on. All of these represent iterations of the great problem of knowing how to establish trust. It’s about preventing fraud and securing the system’s confidence that you can and will pay.

The Origins of Trust

As a young man, one of my father’s first jobs was working in the newly born credit-card industry. He told me the story of its origins decades earlier. It began in single stores with customers that were well known by the proprietor. Rather than pay purchase by purchase, the customer could come in anytime and walk out with merchandise. He or she would receive a single bill at the month. The store could benefit from the convenience that the customer experienced. Everyone won.

This was apparently in the early fifties. All records of credit-card owners were kept by the accounting office. Over time, companies saw advantages in institutionalizing this practice. American Express had begun as a shipping company in the 19th century, became a money-order company, and finally started issuing cards. Visa came along in 1956 and Mastercard in 1966. As sophisticated as these became over time, the model remained the same: if you can be proven to be good for the money, you get a card.

I can recall my first trip to the college bookstore came with piles of offers for credit cards, which were extremely easy to get in those days. I got one, filled it up to my limit in a month or so, and paid high interest paying it off for the next year. I realized my mistake. Many friends of mine did not, and instead began to play credit-card roulette, rolling balances between old and new cards, and eventually ending up with a drawer full of cards and six figures of debt.

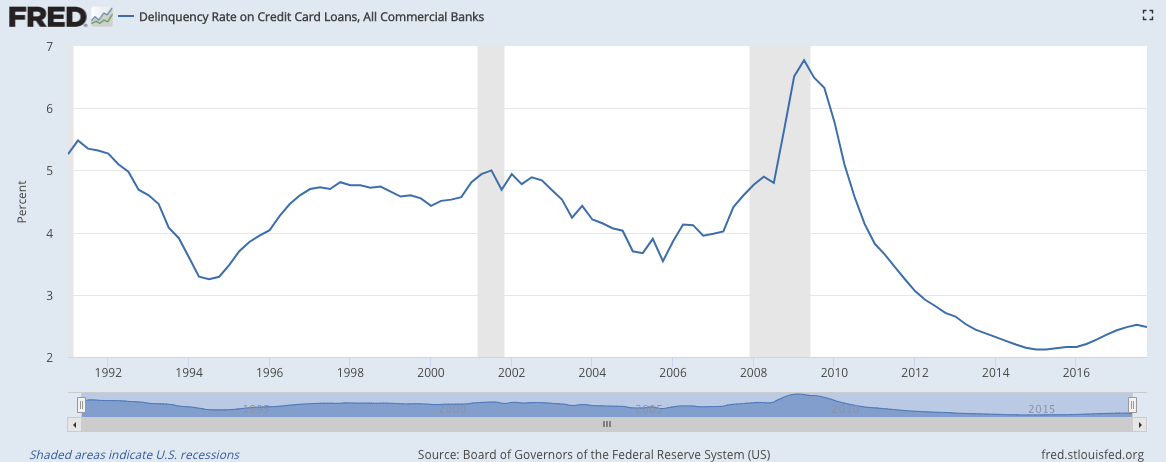

It’s not so easy anymore. Banks clamped down after 2008 and, thanks to both risk aversion and new regulations, started getting fussy again, and for good reason. Now you can’t get a new card without prepaying your credit line for a year, showing the bank that you can manage your money and pay your bills on time. The results are apparent. Delinquency rates are down dramatically since 2008.

The Signature Was Everything

In those days, the signature really did matter. Young people had to practice their unique signature, as if to define their personalities for life, except that it kept changing as the years went on. We must have admired the way our parents signed things with such elan, exactly the way the president signs executive orders today.

You can tell how much people invested in their signatures in the day. We sat in school and practiced them. We used them for papers, and, importantly, for yearbooks. Then the time came when we could sign for the credit-card receipts and its importance grew. Our signature was the way we ported out status as a human being from the heart and mind to the paper and thus toward the acquisition of goods and services.

It was our personality become art. We could reproduce it on demand as an extension of ourselves. Except that, over time, the status of signature started mattering less and less. I have a vague memory of realizing this at the grocery store when the electronic signature pad came along. It dawned on me – and probably millions of others at the same time – that it didn’t matter what I scrawled in that box.

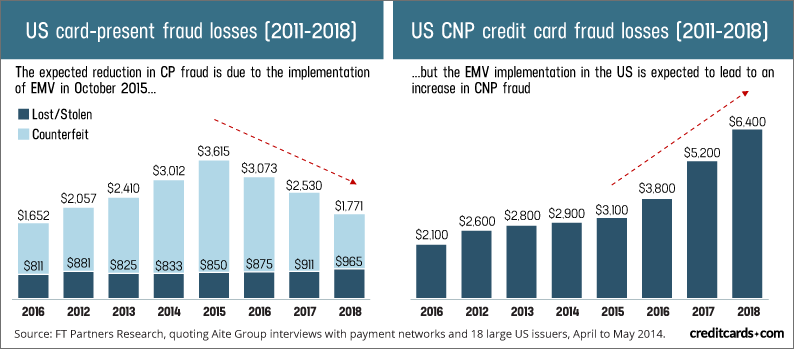

The advent of Internet commerce introduced a new challenge. Card companies had to deal with the problem of “card not present” transactions, further diminishing the status of signatures. It was controversial at first but progress demanded the change in policy. That unleashed an amazing amount of fraud but also the response in fraud-protection techniques. Rather than getting better, however, the problem is getting worse. Nearly half a million Americans report having their credit card numbers stolen every year, resulting in canceled cards and tremendous inconvenience, not to mention the constant threat of data breaches and billions spent to prevent them.

Trust or Verify?

Despite all the technological advances in the credit-card industry, including the newest recognition that a handwritten signature is completely worthless for verifying identity, the core model of credit hasn’t changed since the industry began. Whether you can buy things online comes down to establishing an identity between the decision maker and the real person behind the identity.

This will remain true even if Amazon credit gradually comes to replace the function of banks, as Chloe Anagnos predicts. “Shopping with an Amazon checking or savings account would not only be convenient for customers,” she writes, “it would cut out credit-card companies entirely—thus saving Amazon and consumers substantially on interchange fees.”

Even so, it’s all about who you are. Before blockchain technology came along, it wasn’t obvious how this trust-based system could be replaced with anything. Then came the White Paper, which claimed to establish:

A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double-spending. We propose a solution to the double-spending problem using a peer-to-peer network. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work.

As for signatures, yes, there would be those except digital using double-key cryptography. Fraud (pretending you are someone you are not), however, is prevented through a different technique: proof of both ownership and authority to access a distributed network is verified by evidence of your use of CPU power. In other words, with blockchain technology, it is not about who you are. It’s about what you own and your authority to dispose of it. You don’t have to rely on someone’s truth or benevolence. In many ways, it is the largest leap in our commercial relationships in the postwar period.

The new system is still in its experimental stages, but we’ve already gained a glimmer of the possibilities, including money that operates outside the nation state or the necessity of third-party institutions, smart contracting, as well as the ability to raise capital for enterprises from the broadest swath of humanity.

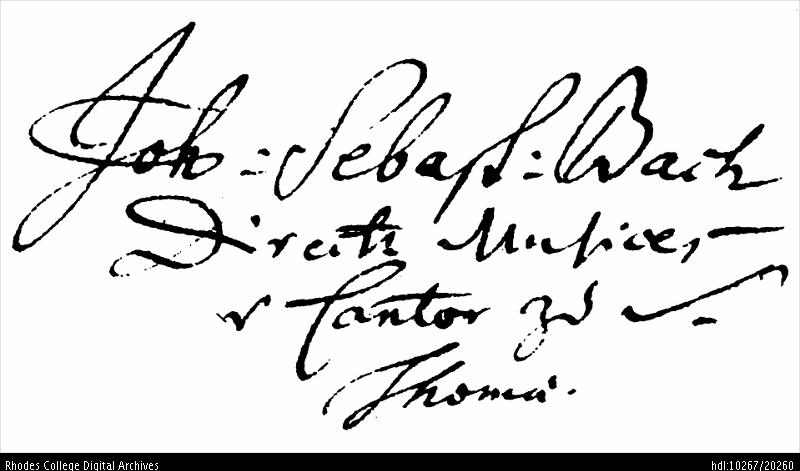

The personal signature has a notorious history: J.S. Bach’s on his compositions, the founding fathers on the Declaration of Independence, Picasso on his paintings, and the president’s today on executive orders. Creating your own was a right of passage.

With credit card companies admitting the obvious that it does nothing to verify your identity, does it matter anymore? The signature isn’t going away. It has just changed forms.

Jeffrey A. Tucker

Jeffrey A. Tucker served as Editorial Director for the American Institute for Economic Research from 2017 to 2021.