Inflation is Slowing. Will the Fed?

The latest data from the Bureau of Economic Analysis (BEA) shows that inflation is slowing. The personal consumption expenditures price index, which is the Federal Reserve’s preferred measure of inflation, grew at a continuously compounding annual rate of just 1.5 percent in May 2023, down from 4.4 percent in the prior month. Prices have grown 3.8 percent over the last year.

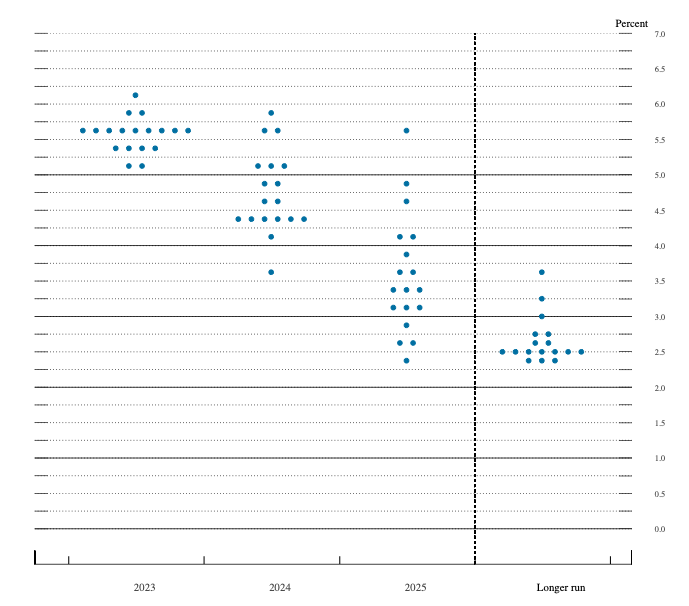

The latest data would seem to confirm that the Fed is on track to bring inflation back down to 2 percent, as promised. But Fed officials don’t see it that way. In June, nearly all members of the Federal Open Market Committee (FOMC) projected further rate hikes this year. The median FOMC member projected two additional 25 basis point hikes, which would put the federal funds rate target range at 5.5 – 5.75 percent by December.

Figure 1. FOMC participants’ assessments of appropriate monetary policy: Midpoint of target range or target level for the federal funds rate. Summary of Economic Projections, June 2023.

What are Fed Officials Thinking?

Although headline inflation has fallen, Fed officials are concerned about core inflation, which excludes volatile food and energy prices and is thought to be a better predictor of future inflation. Core PCEPI grew at a continuously compounding annual rate of 3.8 percent in May, compared with 4.5 percent in the prior month. It has grown 4.5 percent over the last year.

As the Fed tightens monetary policy, “the risks of doing too much versus doing too little become more in balance,” Powell said on Wednesday. “I wouldn’t say they’re in balance yet, but they’re becoming closer to balance. I still believe—and the committee clearly believes—that there’s more work to do, that there are more rate hikes that are likely to be appropriate, though.”

Bond markets are currently pricing in a 25 basis point hike in July.

What Should Fed Officials Be Thinking?

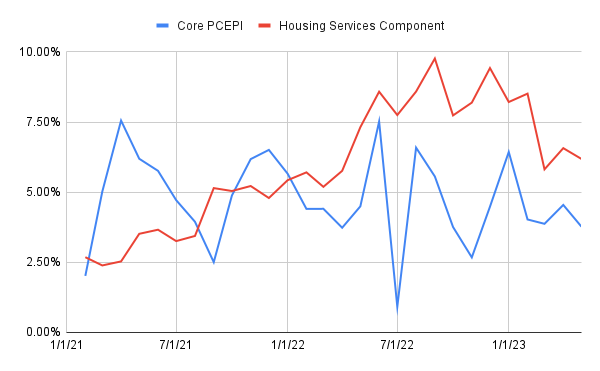

While core inflation remains elevated, there are reasons to think it is overestimating future inflation at present. Most notably, the estimated price of housing services tends to adjust with a long lag. As a consequence, core inflation will initially underestimate inflation following a positive nominal spending shock and then overestimate inflation as that shock dissipates. Indeed, we can see this in the data reproduced in Figure 2.

Figure 2. Core PCEPI and the Housing Services Component

Following the surge in nominal spending in 2021, core PCEPI growth picked up. However, the housing component generally grew slower than core PCEPI growth over 2021. Then, when core PCEPI growth began to slow in the back half of 2022, the growth of the housing component remained elevated, and did not start to slow until March 2023.

Since the estimated price of housing services adjusts with a considerable lag and housing services is such a large component of core PCEPI, it follows that (1) core PCEPI was underestimating inflationary pressure (to a lesser and lesser extent) throughout 2021 and (2) is overestimating inflationary pressure today.

Some Cause for Concern

Although my general view is that inflation is coming down and the risks of doing too much are now greater than the risks of doing too little, there is still some cause for concern. Nominal GDP growth in Q1-2023 was revised up on Thursday. The BEA had previously said nominal spending grew 5.4 percent on an annualized basis in Q1-2023. Its final estimate shows nominal spending grew 6.1 percent. In other words, nominal spending growth has not slowed as much as we had thought. And, since the surge in nominal spending is the primary reason why prices have grown so much, the revised data suggests prices might not come down as quickly as we had previously thought.

Nonetheless, the policy rate appears to be sufficiently restrictive. Using the prior month’s core PCEPI reading as a measure of expected inflation, the real federal funds rate target is between 1.2 percent and 1.45 percent. The New York Fed provides two estimates of the neutral real rate. The Holston-Laubach-Williams estimate was 0.58 percent for Q1-2023, while the Laubach-Williams estimate was 1.14 percent. Both suggest policy is sufficiently restrictive at present. And that’s before making any adjustments to core PCEPI to account for problems with the housing component.

The Fed’s decision to pause in June was probably the right call. Monetary policy works with long and variable lags. Inflation is slowing, but it will take some time to come down. Fed officials should not be too concerned about elevated core inflation. Unless the data show a clear reversal in the disinflationary process, the Fed should continue holding its target rate range where it is. Further tightening seems unnecessary at this point.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.