Will Lower Inflation Halt Rate Hikes?

The Federal Reserve raised its federal funds rate target range to 5.25 to 5.50 percent on Wednesday. In June, the median member of the rate-setting committee projected the federal funds rate would climb to 5.6 percent this year. That suggests another rate hike is on the horizon.

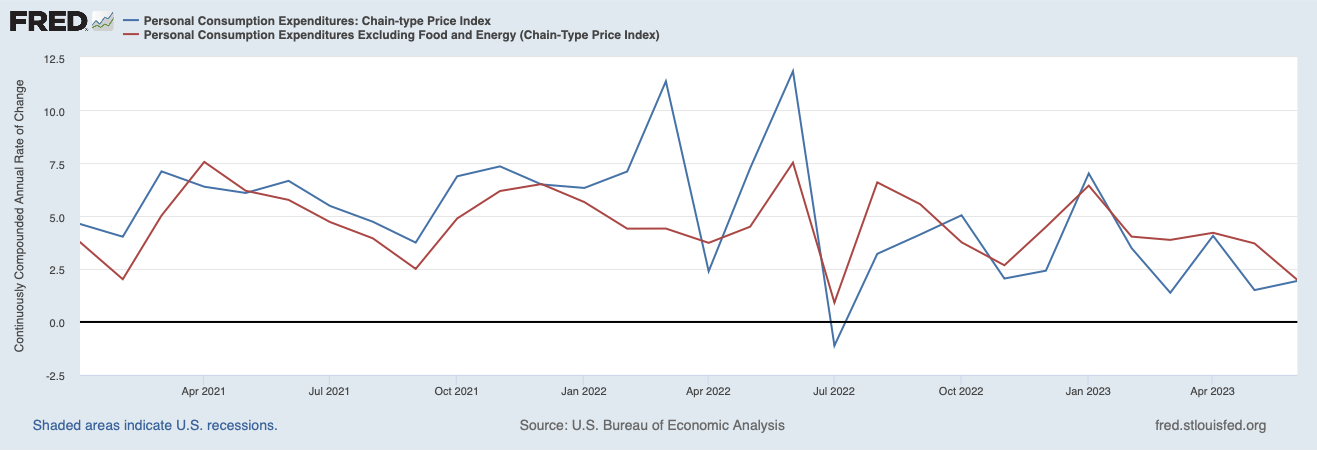

The Personal Consumption Expenditures Price Index (PCEPI), which is the Fed’s preferred measure of inflation, grew at a continuously compounding annual rate of 2.9 percent from June 2022 to June 2023. It grew at an annualized rate of 2.5 percent over the last three months and just 1.9 percent over the last month. In other words, inflation is falling fast.

Core PCEPI, which excludes volatile food and energy prices and is therefore thought to be a better predictor of future inflation, is also falling. Over the 12-month period ending June 2023, core PCEPI grew at a continuously compounding annual rate of 4.5 percent. It grew at an annualized rate of 3.9 percent over the last three months and just 3.7 percent over the last month.

Figure 1. Headline and Core PCEPI Inflation, January 2021 to June 2023

Will lower inflation cause Fed officials to forego further rate hikes? Maybe. Disinflation passively increases the real (i.e., inflation-adjusted) federal funds rate. When inflation falls faster than Fed officials expect, real interest rates rise faster than Fed officials intended when they set the nominal interest rate target. If the real rates rise high enough, Fed officials might be able to achieve their desired level of tightness without pushing its nominal rate target higher.

Judging by interest rates, monetary policy looks sufficiently restrictive. The Federal Reserve Bank of New York estimates the natural rate of interest at 0.58 to 1.14 percent. Using the prior month’s core PCEPI inflation rate of 3.7 percent as an estimate of expected inflation implies the real federal funds rate target range is 1.55 to 1.80 percent—well above the natural rate. If one were to use last month’s headline PCEPI inflation rate instead, it would imply the real federal funds rate target range is even higher: 3.35 to 3.60 percent. No matter how you slice it, real rates look sufficiently restrictive to bring down inflation. Indeed, they may be overly restrictive at this stage in the tightening cycle.

Nominal spending growth also suggests monetary policy is sufficiently restrictive. In the 10-year period prior to the pandemic, nominal spending grew at a continuously compounding annual rate of 3.9 percent. Nominal spending surged in 2021, growing 11.5 percent. But it has fallen in the time since. In 2022, it was 7.1 percent. It grew at an annualized rate of 6.0 percent in Q1-2023, and just 4.6 percent in Q2-2023. Although it is not yet back to the pre-pandemic average growth rate, it is on track to normalize by the end of the year.

If monetary policy is already sufficiently restrictive, why is it not so clear that the Fed will forego further rate hikes? In brief, some Fed officials are not yet convinced they’ve done enough—and don’t want inflation to resurge on their watch.

Governor Christopher Waller made the case for further rate hikes in a recent speech. Waller argues that monetary policy lags are much shorter following large shocks, like the 525 basis point increase in the federal funds rate that has occurred since February 2022. Whereas people might be rationally inattentive to small shocks and, as a consequence, react slowly, they cannot help but notice large shocks and, hence, respond more quickly. Waller also argues that the start of the lag beggins not when the Fed raises its federal funds rate target but rather when it announces it will raise its federal funds rate target in the future—at least so long as such announcements are deemed credible.

If monetary policy lags are shorter and start sooner than more conventional estimates suggest, “the bulk of the effects from last year’s tightening have passed through the economy already” and “we can’t expect much more slowing of demand and inflation from that tightening. To me,” Waller concludes, “this means that the policy tightening we have conducted this year has been appropriate and also that more policy tightening will be needed to bring inflation back to our 2 percent target.”

If Waller’s argument carries the day, Fed officials will raise the federal funds rate target range another 25 basis points in September or November. If disinflation continues over the next few months, such a hike could prove devastating—not merely wiping out inflation, but economic growth and employment as well.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.