The Floor System Fails

The technical nature of monetary policy obscures a basic fact: Governments created central banks for fiscal reasons. As a result, public finance considerations receive little attention in monetary policy debates. For example, while economists have rightly criticized the Federal Reserve’s policy of paying interest on reserves because it undermines the Fed’s independence and weakens inter-bank monitoring, there has been little criticism of the inconsistency between this policy and basic public finance principles.

Rather than adjust the supply of reserves to achieve its federal funds rate target, as it did before 2008, the Fed now adjusts the interest it pays banks holding the large supply of reserves it has created. As a result, the federal funds rate closely tracks the interest rate paid on reserves. Indeed, that is why this system is called a floor system: The interest rate paid on reserves creates a floor for the federal funds rate.

Some economists argue that the floor system is consistent with Milton Friedman’s view of the optimum quantity of money. In brief, people will adjust the assets they hold in their portfolio until the risk-adjusted rates of return are equal. If the rate of return on money is less than similar assets, people will hold too little money. To ensure the public holds the right amount of money (what Friedman calls the optimum quantity), the central bank must ensure that money pays a rate of return comparable to similar assets. Economists call this policy the Friedman rule. One way to ensure the public holds the optimum quantity of money is for the Fed to generate a mild deflation, such that zero-nominal-interest money earns a positive real rate of return. An alternative would be for the Fed to pay interest on banks’ reserve balances. If the banking system is reasonably competitive, this policy would ensure that the interest payments ended up in the public’s bank accounts. Since currency is a small fraction of the money supply, paying interest on reserves would come reasonably close to implementing the Friedman rule.

However, even if we assume the Fed sets the rate of interest on reserves in a manner consistent with the Friedman rule, this argument has a fundamental problem: the rule only applies in a world without distorting taxes. We do not live in such a world, of course. Income taxes, sales taxes, and capital gains taxes all distort economic activity. Consequently, there is a a deadweight loss of taxation—that is, a reduction in wealth that results when people adjust their behavior because of taxes.

A basic principle of public finance is that efficient taxation requires an extra dollar raised from different taxes to generate the same deadweight loss. If this condition does not hold, we could all be better off by lowering taxes on those activities where the deadweight losses are large and raising taxes on those activities where the deadweight losses are small. The same logic applies to the inflation tax, which is a tax on holding money balances. Thus, the optimal inflation tax is not zero in a world with distorting taxes.

What does this principle have to do with the floor system?

Before 2008, the Fed varied the quantity of reserves in the banking system by issuing non-interest-bearing reserves, which it used to purchase interest-bearing government bonds. The interest-rate spread between these bonds and reserves represented the Fed’s seigniorage revenue from monetizing Treasury debt, most of which the Fed remitted to the Treasury. Under the current floor system, however, the Fed must pay interest on the reserve balances it issues out of the interest income it earns from its asset portfolio.

Using the floor system to implement the Friedman rule would require the Fed eliminate the spread between government bonds and reserves, thereby eliminating seigniorage revenue. If government spending does not decrease by the same amount, the lost seigniorage revenue must be offset by raising taxes elsewhere. Consequently, the deadweight losses from the other taxes must increase, as the government now relies on sources of revenue that, at the margin, involve larger deadweight losses than the inflation tax.

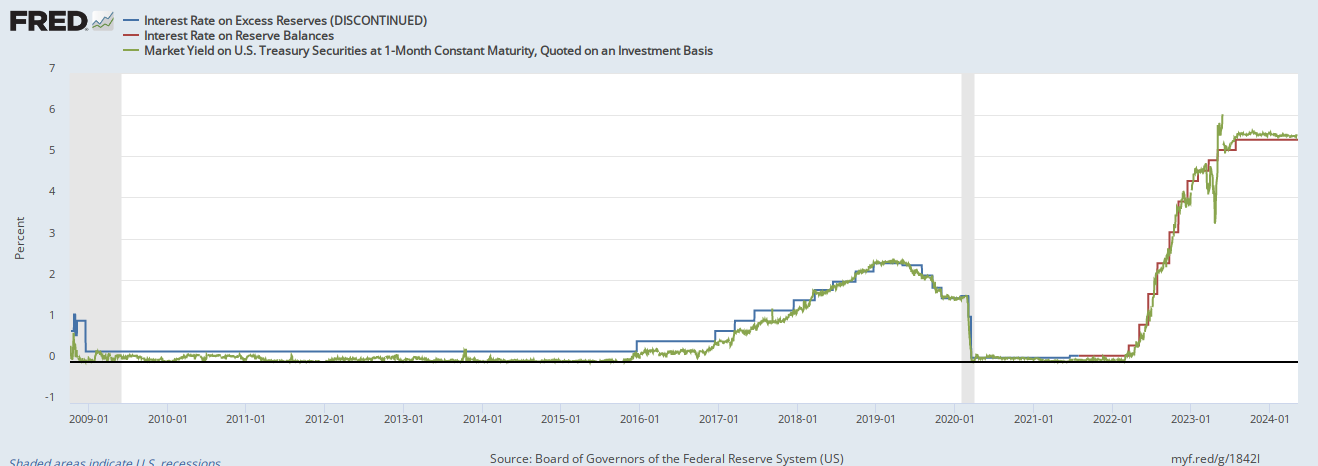

The upshot is that the Friedman rule justification for the floor system conflicts with the principle of optimal taxation. Basic public finance considerations suggest that the spread between government bonds and reserves should be slightly positive. In theory, a floor system drives this spread to zero. In practice, it has been slightly negative, as Congress prohibited the Fed from paying interest on the reserve balances that government-sponsored enterprises keep on account at the Fed. In other words when the Fed buys a one-month Treasury bill, the purchase costs the taxpayer more than if it had not, as the figure below illustrates. Thus, whatever the merits of the floor system may be in theory, its real-world implementation has been a failure.

During normal times, when inflation is low and stable, the floor system increases the burden on taxpayers. The burden is even larger when inflation is high, as it has been over the past two years: the Fed has realized significant losses, which taxpayers must ultimately bear. If Fed officials paid for their mistakes, they would have likely abandoned the floor system long ago. But Fed officials do not pay for their mistakes. We do.

Louis Rouanet

Louis is an assistant professor at the University of Texas at El Paso and affiliated faculty with the Center for Free Enterprise. He received his degree in 2021 from George Mason University.

{kind=link}