Strong GDP Headline Masks First-Quarter Weakness

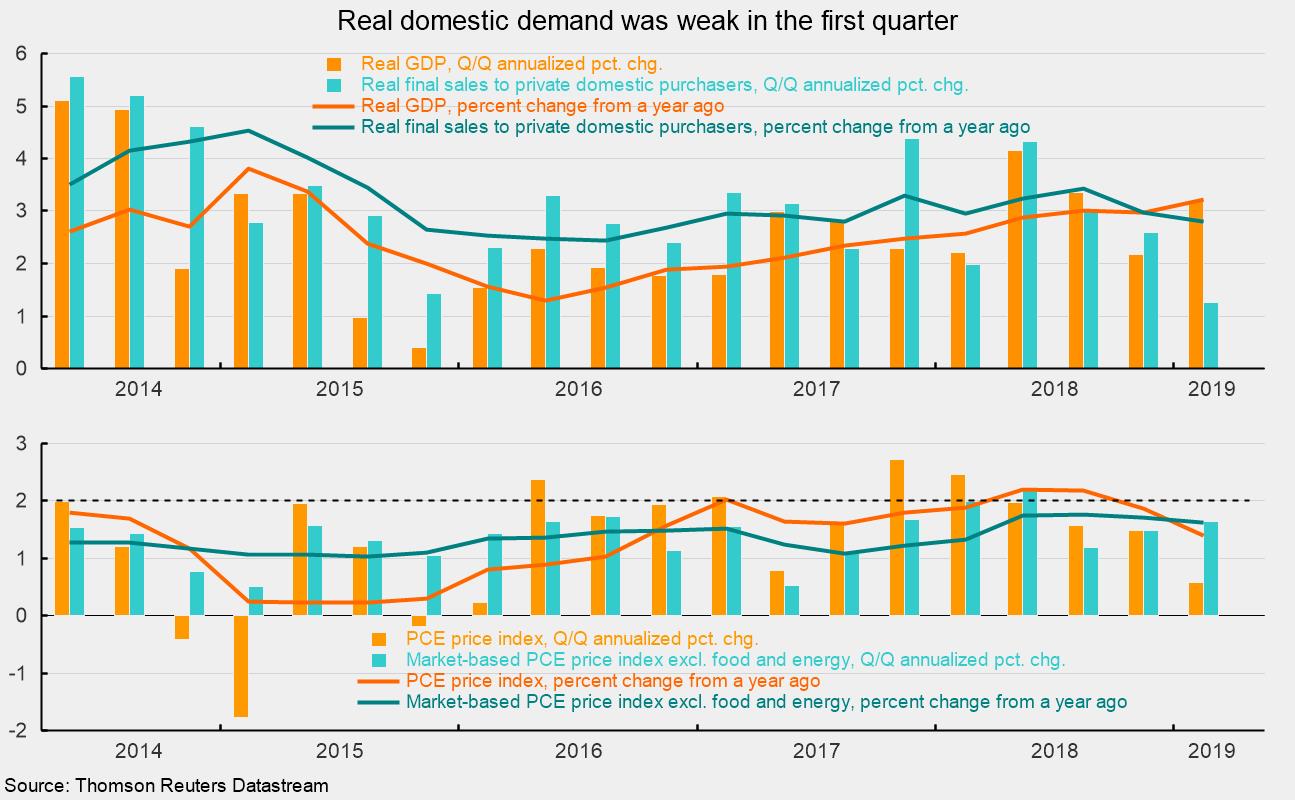

Real gross domestic product rose at a 3.2 percent annualized rate in the first quarter, up from a 2.2 percent pace in the fourth quarter of 2018, according to the Bureau of Economic Analysis. Over the past four quarters, real gross domestic product is up 3.2 percent, the fastest pace since 2015 (see chart).

Despite the strong headline growth rate, many components of domestic demand were weak, but they were offset by inventory accumulation and lower imports (imports count as a negative in the calculation of GDP). Weakness in domestic demand in the first quarter was expected as the government shutdown in December and January affected economic activity.

Consumer spending decelerated sharply in the first quarter, rising at a lethargic 1.2 percent pace compared to a 2.5 percent growth rate in the fourth quarter. The deceleration was mostly the result of a drop in spending on goods, with durable-goods growth declining from a 3.6 percent pace of growth in the fourth quarter to a 5.3 percent rate of decline in the first quarter. Nondurable-goods spending rose at a 1.7 percent pace versus a 2.1 percent rate in the previous quarter. Spending on services slowed slightly, from 2.4 percent to 2.0 percent.

Business investment rose at a 2.7 percent annualized rate in the first quarter of 2019. That gain was led by an 8.6 percent gain in intellectual-property investment. Spending on equipment rose 0.2 percent versus a 6.6 percent gain in the previous quarter while spending on structures fell 0.8 percent, better than the 3.9 percent drop in the prior quarter. Spending on nonresidential structures has fallen for three consecutive quarters.

Residential investment, or housing, fell 2.8 percent in the first quarter compared to a 4.7 percent decline in the prior quarter. Housing has decreased for five straight quarters. Altogether, business and residential investment contributed 0.27 percentage points to total GDP growth compared to a 0.54 percentage-point contribution in the fourth quarter.

Inventory accumulation by businesses accelerated in the first quarter, adding 0.65 percentage points to first-quarter growth after contributing 0.11 percentage points in the prior quarter. Inventory accumulation has boosted real gross domestic product for three consecutive quarters.

Exports rose at a relatively robust 3.7 percent pace, adding 0.45 percentage points, while imports declined at a 3.7 percent rate. Since imports count as a negative in the calculation of gross domestic product, a drop in imports is a positive for GDP growth.

Government spending rose at a 2.4 percent annualized rate in the first quarter compared to a 0.4 percent decrease in the fourth quarter, contributing 0.41 percentage points to growth versus a 0.07-point reduction in the final quarter of last year.

Real final sales to private domestic purchasers, a key measure of private domestic demand, rose at a weak 1.3 percent annualized rate in the first quarter, down from a 2.6 percent pace in the fourth quarter (see chart). The first-quarter gain was the slowest since 2013. Over the past four quarters, real private domestic demand is still up at a 2.8 percent rate, slightly below the 3.0 percent gain for the four quarter of 2018 (see chart).

Consumer price measures were subdued in the first quarter. The personal-consumption price index rose at a 0.6 percent annualized rate, down from a 1.5 percent pace in the fourth quarter (see chart). From a year ago, the index is up 1.4 percent, well below the Federal Reserve’s 2 percent target. Excluding the volatile food and energy categories, the market-based core PCE (personal consumption expenditures) index rose at a 1.6 percent pace, the third quarter in a row below 2 percent (see chart). From a year ago, the market-based core PCE index is up 1.6 percent and has been below 2 percent since 2012.

The strong headline gain masked the poor performance of domestic demand in the first quarter. However, the weakness was partially due to the government shutdown, which ended in January. While the effects were sizable, the impact is fading. Though economic data are still somewhat mixed, some recent positive signs are emerging.

The underlying trend in real private domestic demand remains fairly well-supported by continued job creation, rising wages, generally healthy corporate and consumer balance sheets, solid corporate-sales and corporate-earnings growth, and favorable levels of business and consumer confidence. The virtuous cycle between the consumer and corporate sectors is likely to provide ongoing support for further gains in real private domestic demand, suggesting continued economic expansion in the months and quarters ahead, but caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.