Real GDP Gain Masks Slowdown in Private Domestic Demand

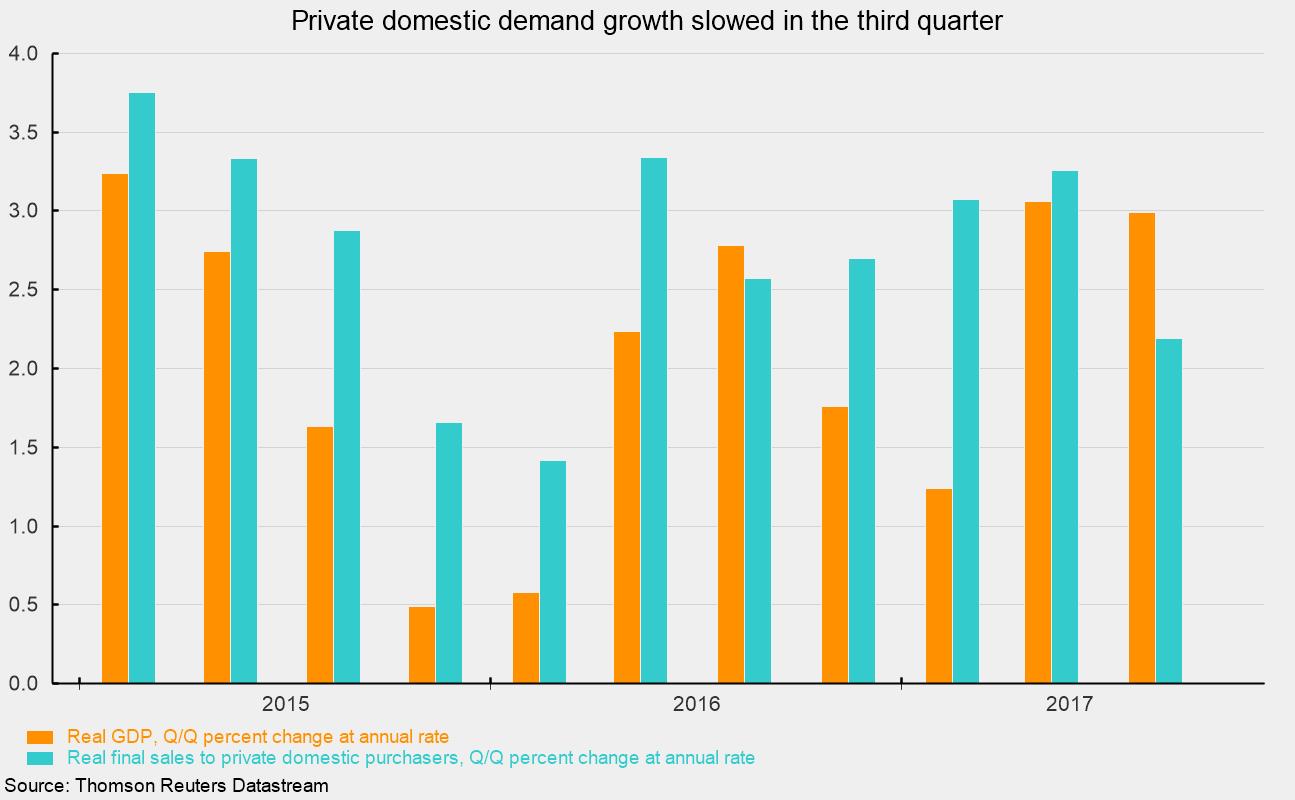

The advance estimate for third-quarter real gross domestic product shows a 3.0 percent annual rate of growth, nearly matching the 3.1 percent rise in the second quarter. But that headline number masks a notable slowdown in private domestic demand. Private domestic demand, also known as real final sales to private domestic purchasers, is the sum of personal consumption expenditures, business fixed investment, and residential investment (housing). The difference between the two growth rates in the third quarter was primarily due to inventory accumulation, which added 0.73 percentage points to third-quarter real GDP growth.

Private domestic demand has been the primary driver of real GDP growth for most of the current economic expansion. PDD posted a more modest 2.2 percent growth rate in the third quarter than the 3.3 percent in the second quarter. Since 2015, PDD growth has beaten GDP growth in 9 of 11 quarters, registering an annualized growth rate of 2.7 percent versus 2.1 percent for GDP. Over the last four quarters, PDD is up 2.8 percent versus 2.3 percent for GDP.

Within PDD, at 2.4 percent, personal consumption expenditures grew at a slower annual rate in the third quarter than the 3.3 percent in the second quarter. That slowdown was a result of slower growth in consumer spending on nondurable goods (2.1 percent versus 4.2 percent in the second quarter) and on consumer services (1.5 percent versus 2.3 percent). Spending on consumer durable goods accelerated in the third quarter — primarily due to motor vehicles sales, which surged in September as hurricane-damaged vehicles were replaced — posting a rise of 8.3 percent compared to 7.6 percent in the second quarter.

Business fixed investment spending decelerated to a 3.9 percent pace compared to 6.7 percent growth in the second quarter. Within business fixed investment, spending on nonresidential structures declined — at a 5.2 percent annual rate — versus a 7.0 percent gain in the second quarter. Spending on equipment held relatively steady, posting 8.6 percent growth versus 8.8 percent in the second quarter, and investment in intellectual property products accelerated to a 4.3 percent pace compared to 3.7 percent growth in the second quarter.

Outside of PDD, inventory accumulation added 0.7 percentage points to overall GDP growth while net exports added 0.41 percentage points and government spending deducted 0.02 percentage points. The contribution by net exports reflects a 2.3 percent rise in exports and a 0.8 percent drop in imports. Within the government sector, federal nondefense spending and state and local spending fell by 0.5 percent and 0.9 percent respectively while federal defense spending rose 2.3 percent in the third quarter.

Price measures in the GDP report were mixed in the third quarter. The overall GDP price index rose 2.2 percent in the third quarter, driven by increases in prices for nonresidential and residential structures, up 4.6 percent and 5.1 percent respectively, as well as the federal nondefense and state-and-local sectors, gaining 2.4 percent and 3.2 percent.

The PCE price index, preferred by the Fed, rose 1.5 percent in the third quarter and 1.5 percent from the third quarter of 2016 to the third quarter of 2017. Excluding the volatile food and energy categories, the core PCE price index is up just 1.3 percent from a year ago, the slowest pace since 2015.

Overall, the headline GDP number masks a deceleration in domestic demand. However, a healthy labor market, decent wage and income growth, and record net worth suggest support for better consumer spending and continued GDP growth in coming quarters.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.