New Unemployment Claims Slowed Again as Total Unemployed Hits a Record High

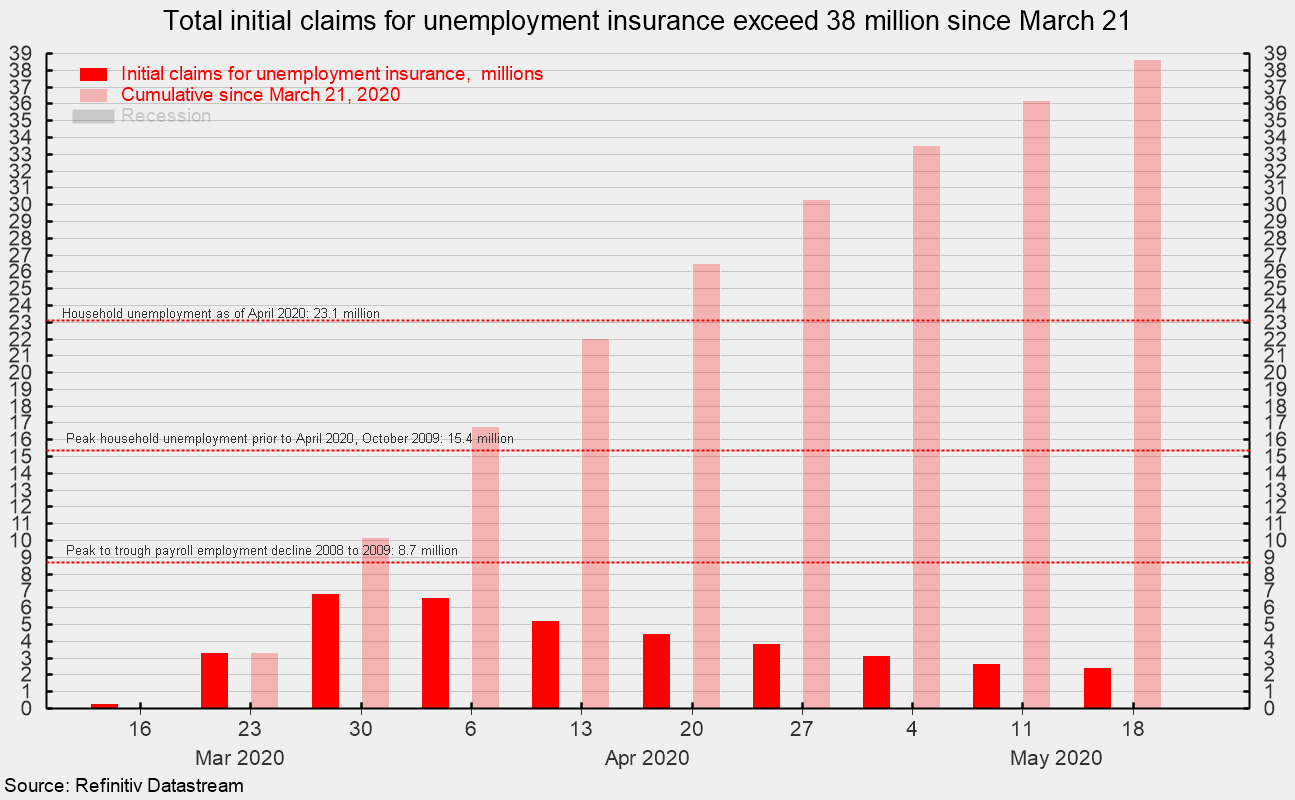

Initial claims for unemployment insurance totaled 2.44 million for the week ending May 16, marking the ninth consecutive week of massive numbers of layoffs (see chart). However, claims have slowed for the seventh straight week after registering 6.87 million for the week ending March 28.

The current 9-week total of 38.6 million initial claims is more than four times the total of 8.7 million job losses that occurred over 25 months versus during the Great Recession (see chart). The current total is also more than double the 15.4 million peak number of unemployed people for the Great Recession and is above the record-high 23.1 million unemployed shown in the April 2020 jobs report, suggesting the May jobs report could be another disaster.

The April jobs report also showed a drop of 20.5 million in nonfarm jobs while the unemployment rate surged to 14.7 percent. Furthermore, the Bureau of Labor Statistics said that incorrect responses on the survey suppressed the calculated unemployment rate and that if properly coded, the unemployment rate would be about 5 points higher, closer to 20 percent. The previous cycle peak in the unemployment rate was 10 percent in October 2009 while the highest unemployment rate since 1950 came in November 1982 at 10.7 percent. Though data collection was much less reliable, the unemployment rate following the Great Depression was estimated to have peaked at about 25 percent in 1933.

Massive layoffs over the last nine weeks have crushed the labor market, consumer confidence and retail spending. The unprecedented flood in claims is part of a tsunami of negative economic statistics that reflects the impact of the COVID-19 outbreak and the drastic policy reactions implemented to contain the spread. Despite massive government spending and extraordinary monetary policy efforts, the economy likely entered a recession in March, ending the longest economic expansion in U.S. history.

All 50 states have begun easing restrictions though plenty of restrictions remain. The easing should start to reverse some of the distortions to overall economic activity, but it will likely take a significant period of time to fully recover. Expect extraordinarily weak economic reports over the next few months.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.