Labor Market Shows Broad Strength Prior to COVID-19 Outbreak

Hiring surged in February as U.S. nonfarm payrolls added 273,000 jobs after a similar increase of 273,000 new jobs in January. February’s gain was the third increase of more than 250,000 in the last four months. Over the last six months total payrolls have risen by more than 1.38 million or an average of 230,000 per month. For the past year, the total gain was over 2.4 million or about 200,000 per month. While the results are very favorable, they do not reflect the initial effects of the outbreak of COVID-19. Strong momentum in the labor market should help the economy resist some of the temporary disruptions to economic activity. However, the longer and more widespread the disruptions, the more likely the economy falls into recession. Extreme caution is warranted.

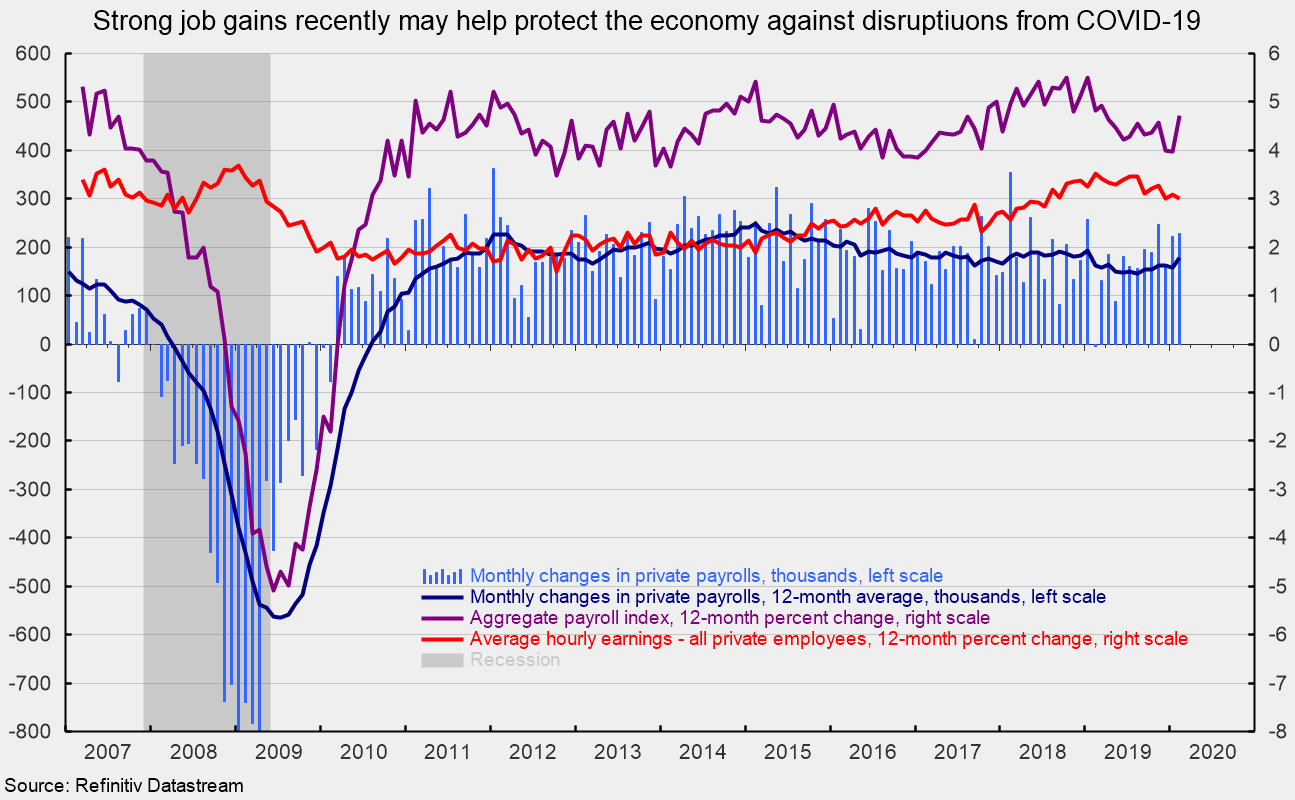

For the private sector, nonfarm payrolls added 228,000 in February following a gain of 222,000 in January (see chart). Private payroll gains have exceeded 220,000 in three of the last four months. Over the last six months private payrolls have risen by more than 1.25 million or an average of 207,000 per month. For the past year, the total gain was over 2.15 million or 179,000 (see chart).

Goods-producing industries added 61,000 jobs in February, ahead of the monthly average gain of 19,000 over the past year. Construction and durable-goods manufacturing led with additions of 42,000 and 11,000 jobs, respectively, while nondurable-goods industries and natural resources and mining industries both added 4,000 workers for the month.

Within private service-producing industries, which typically account for the lion’s share of job creation, payrolls added 167,000 workers, a little ahead of the 12-month average increase of 160,000. The February rise was led by a 56,500 gain in health care and social assistance and a 51,000 jump in the leisure and hospitality industries. Professional and business services posted a gain of 41,000 jobs for the latest month. All those areas exceeded their prior 12-month average gain. Financial industries posted a surprisingly strong 26,000 job increase, about double the average for the latest 12 months. Retail industries lost 7,000 jobs in February.

The unemployment rate fell to 3.5 percent from 3.6 percent in January, matching the 50-year low. The labor force participation rate held at 63.4 percent in February, the highest since June 2013, as 60,000 people left the labor force.

Average hourly earnings rose 0.3 percent in February, pushing the 12-month change to 3.0 percent. Average hourly earnings growth has been very slow compared to previous cycles, especially given the low unemployment rate. After hitting a 12-month pace of 3.5 percent several times in 2019, the pace of growth has decelerated a bit recently (see chart).

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls rose 0.8 percent in February. That gain helped push the 12-month increase to 4.7 percent, the fastest since March 2019 (see chart). This index is a good proxy for take-home pay and has posted relatively steady year-over-year gains in the 3.5 to 5.5 percent range since 2010. Continued gains in the aggregate-payrolls index is a positive sign for consumer income and spending, supporting continued economic expansion.

The latest employment report suggests that the labor market was generally strong before the outbreak of COVID-19. The effects of the outbreak on economic activity are still unknown but are likely to be significant in the short term. The economy is likely able to withstand a short-term disruption. However, the longer and more widespread the disruptions to activity, the more likely a recession becomes.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.