Jobs Report Sends Mixed Signals

United States nonfarm payrolls added 130,000 jobs in August, below the consensus expectation of 158,000. The prior two months were revised down, showing gains of 159,000 and 178,000 for July and June, respectively. The three-month average from June to August was 156,000, well below the 199,000 average since 2011, but still a decent performance. Despite the slowdown in jobs growth, hourly earnings rose, the length of the workweek increased, the unemployment rate held steady and the participation rate rose. Overall, the report provides mixed signals.

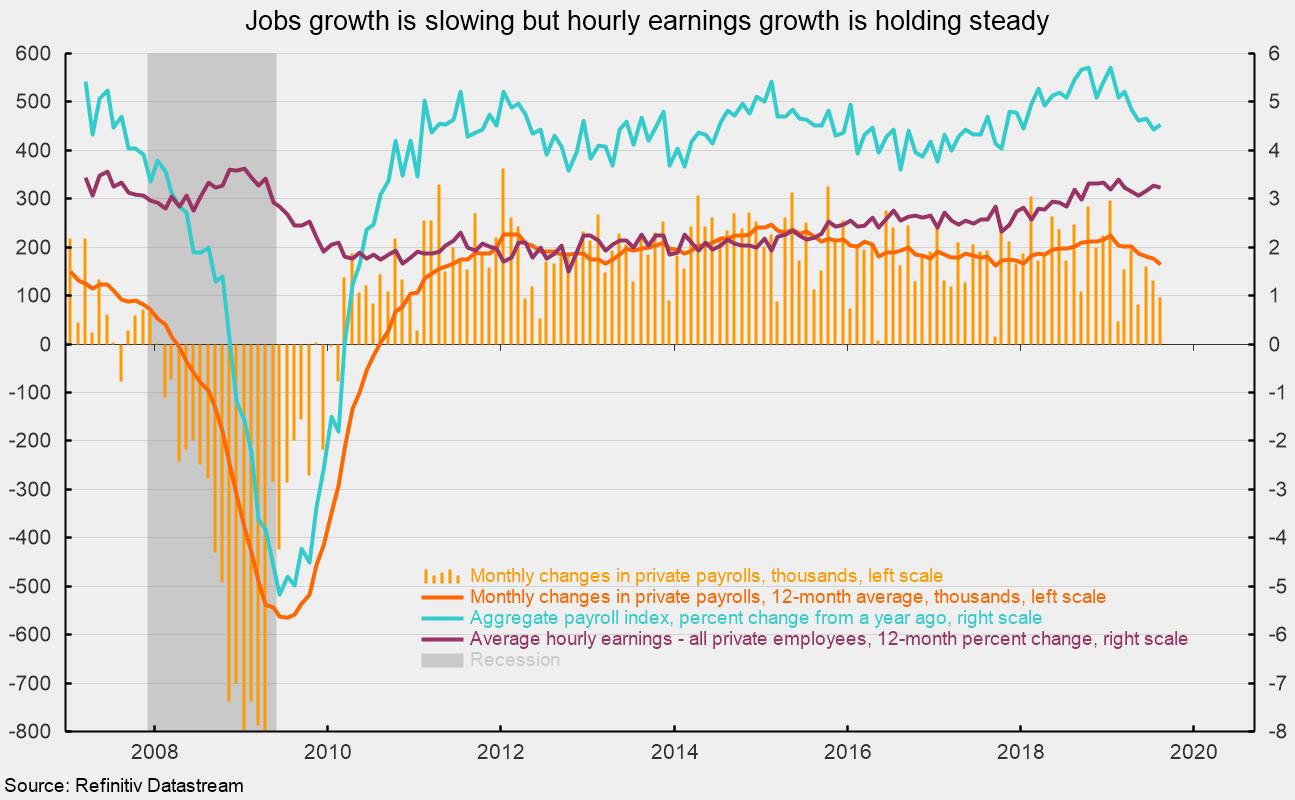

Private payrolls added 96,000 in August following revised gains of 131,000 in July and 161,000 in August (see bars in chart). Those result in a three-month average of 129,000. Over the past year, the monthly gain for private payrolls was 165,000 (see chart). Since 2011, the 12-month average gain has ranged between roughly 150,000 and 250,000, putting the last 12 months in the lower part of the range. Job creation has clearly slowed over the past 7 months. A critical question: is hiring slowing because of difficulty finding qualified employees or because employers are becoming more cautious in an environment of erratic and unpredictable trade and monetary policy and escalating trade wars?

Within the 96,000 gain in jobs, goods-producing industries added 12,000 employees in August, below the average gain of 27,000 over the past year. Construction led the way on the upside, adding 14,000 jobs following a loss of 2,000 jobs last month. The 12-month average for construction industries is 15,000. Nondurable-goods manufacturing added 3,000 jobs (versus a 12-month average of 4,000) while durable-goods manufacturing was unchanged for the month (versus a 12-month average of 8,000). Mining and logging industries lost 5,000 jobs.

For private service-producing industries, which typically account for the lion’s share of job creation, payrolls added 84,000 workers, led by increases of 37,000 in professional and business services and in health care and social-assistance industries. Financial industries added 15,000 jobs while leisure and hospitality payrolls expanded by 12,000 in August, averaging 26,000 a month over the past year. Retailers cut 11,000 workers continuing a prolonged trend of decline.

The public sector added 34,000 employees. The federal government added 28,000 including 25,000 workers for the 2020 census. State government payrolls expanded by 6,000 while local government payrolls were unchanged.

The unemployment rate held steady at 3.7 percent for the third month in a row and the participation rate rose in August to 63.2 percent. The unemployment rate is just 0.1 percentage points above the 3.6 percent cycle low from April and May 2019 and the second-lowest since 1969. The participation rate remains well below the 66.0 to 67.0 percent rate that prevailed from 1988 through mid-2008.

Average hourly earnings rose 0.4 percent in August, resulting in a 12-month gain of 3.2 percent (see chart). Gains in average hourly earnings have been below gains in previous cycles, but the growth rate has been slowly drifting higher since 2015. The 12-month gain has been above 3 percent for 11 consecutive months. The average length of the workweek increased by 0.1 hours to 34.4 hours in August. Average weekly hours have been bouncing around between 34.3 and 34.6 hours since 2012.

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls rose 0.7 percent in August and is up 4.5 percent from a year ago (see chart). This aggregate measure has posted relatively steady year-over-year gains in the 3.5 to 5.5 percent range since 2011.

The weak jobs report for August raises concerns over the strength of the labor market. There’s enough evidence to suggest that the labor market remains solid but the recent slowing in job creation is worrisome. In an environment where erratic and unpredictable policy, apparently driven purely by the potential for political gain, has sharply increased uncertainty, caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.