January 2020 Business Conditions Monthly

Modest readings continue for the AIER Leading Indicators index, suggesting slow growth with downside risks.

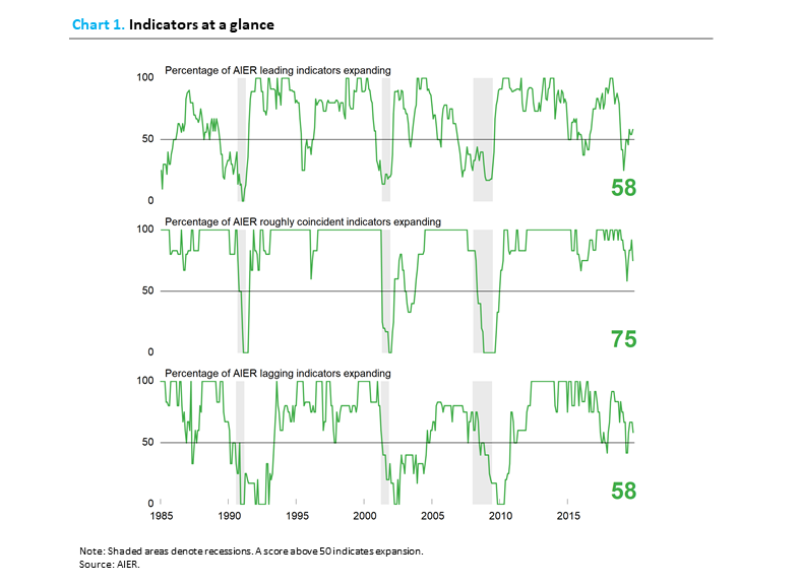

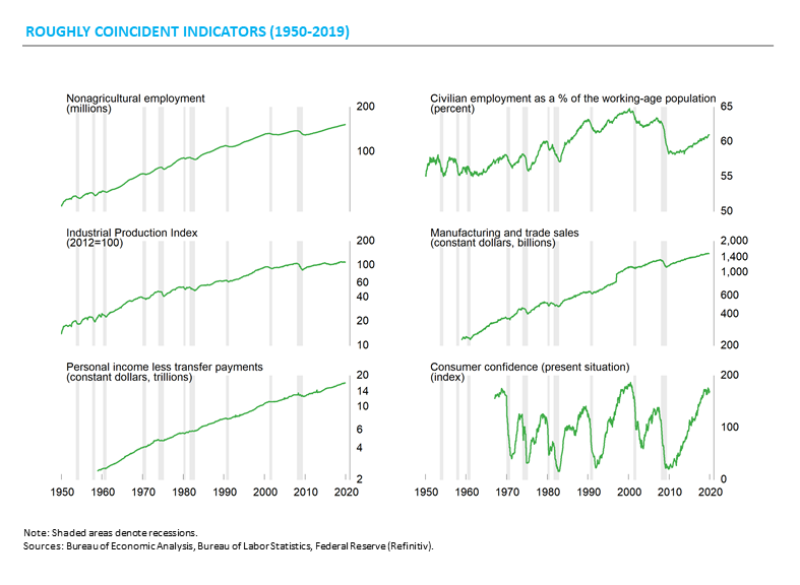

AIER’s Business Cycle Conditions Leading Indicators index fell 4 points to 54 in December. The latest result was the eighth month in a row with the index coming in between 45 and 58. The Roughly Coincident Indicators index held at 75 while the Lagging Indicators index was unchanged at 58 (see chart).

The run of moderate results for the Leading Indicators Index reflects the overall mixed picture for the economy. Economic data show varied strength among the major sectors. Furthermore, with the current expansion well into record length, there is little pent-up demand. However, the combination of a strong labor market, slow price increases, low interest rates, and generally healthy balance sheets for consumers provide a solid foundation for continued growth.

Politics and policy uncertainty have the potential to undermine consumer and business confidence, and given the modest pace of growth, it would not take much to reduce growth to zero. Overall, the economy continues to expand but remains vulnerable to continued erratic policies and political partisanship.

The AIER Leading Indicators index gave back the small gain from November, leaving the index just slightly above neutral for the fifth consecutive month.

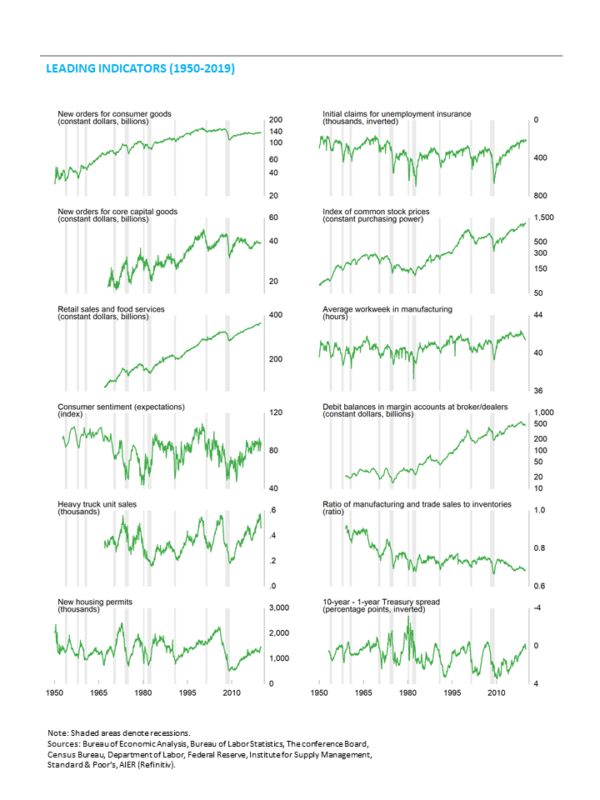

The AIER Leading Indicators index fell 4 points to 54 in December. The index has been range bound between 45 and 58 for 8 consecutive months and hasn’t been above 60 since November 2018. The extended period of close-to-neutral results are consistent with the overall mixed performance of the various sectors of the economy. The results suggest continued economic expansion albeit at a moderate pace and with a heightened degree of uncertainty. Overall, just 5 of the 12 leading indicators maintained a positive trend in December, with 4 trending lower while 3 indicators were neutral.

Positive trends were maintained by initial claims for unemployment insurance, real retail sales and food services, real new orders for consumer goods, housing permits, and real stock prices. Neutral results came from real new orders for core capital goods, the University of Michigan index of consumer expectations, and the 10-year–1-year Treasury yield spread. All three neutrals for December were improvements from unfavorable trends in the prior month.

Total heavy-truck unit sales, the ratio of manufacturing and trade sales to inventory, the average workweek in manufacturing, and debit balances in customers’ margin accounts had unfavorable trends in December. Total heavy-truck unit sales weakened from a positive trend in the prior month while the remaining three continued their downtrends from the prior month.

Overall, the Leading Indicators index remains above 50, indicating continued expansion is likely. However, the extended run of close-to-neutral results combined with other mixed data and policy uncertainty suggest a high degree of caution is warranted.

The Roughly Coincident Indicators index was unchanged in December, maintaining a 75 after hitting 92 in October. This index frequently posts readings of 100 late in economic expansions but hasn’t seen a perfect score since December 2018. The less-than robust results confirm the mixed performance of the economy.

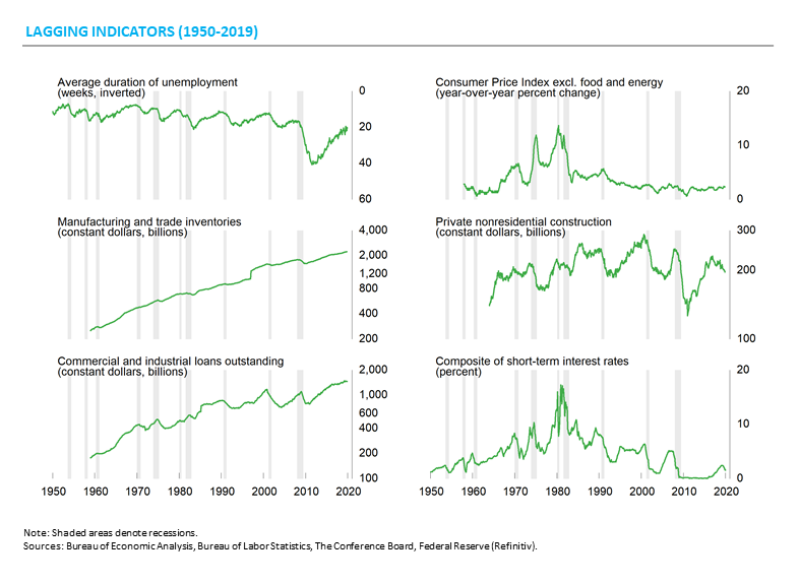

AIER’s Lagging Indicators index held at 58 in December following three months at 67 from August through October. There were no changes among the six indicators, with three indicators trending higher, two trending lower, and one holding in a neutral trend.

Overall, the three AIER business cycle–indicator indexes are still in favorable territory, suggesting a continued positive economic outlook. However, all three are weak compared to history, suggesting slow growth with heightened uncertainty. Caution is warranted.

Consumer balance sheets look healthy with record-high net worth and low liabilities-to-asset ratio.

Household net worth reached $113.8 trillion at the end of the third quarter. Total assets were $130.2 trillion, with financial assets at $91.0 trillion, or 69.9 percent of the total, while nonfinancial assets were $39.2 trillion, or 30.1 percent. Total assets increased 0.6 percent for the quarter and were up 3.3 percent from a year ago.

Household liabilities were $16.4 trillion at the end of the third quarter. Mortgage debt was $10.5 trillion, or about 64.2 percent of the total. Total household liabilities increased 0.8 percent for the quarter and were up 3.3 percent from a year ago. Mortgage debt rose 0.9 percent for the quarter while the value of household real estate rose 0.3 percent. Total owners’ equity in real estate rose to 64.0 percent of the value of the real estate. Consumer credit totaled $4.1 trillion, or about 25.2 percent of total household liabilities after a 1.9 percent increase for the quarter. From a year ago, consumer credit is up 4.8 percent. Total household liabilities were 12.6 percent of total household assets, the second-lowest ratio since 1985.

The combination of low debt levels, low interest rates and rising incomes is keeping debt service burdens low.

Debt service for households was 15.0 percent of disposable personal income in the third quarter, equaling the 39-year low. Debt service peaked at 13.2 percent of disposable income in the fourth quarter of 2007 but fell sharply over the 2008 through 2012 period. The average over the past 39 years is 11.2 percent.

Servicing total recurring financial obligations, a broader measure than debt service that includes rent, auto leases, homeowners’ insurance, and property taxes, totaled 15.0 percent of disposable personal income in the third quarter. That is just slightly above the 39-year low of 14.9 percent from the fourth quarter of 2012. The average over the last 39 years is 16.4 percent.

Overall, while debt levels are rising moderately, increases in assets are keeping balance sheets strong while the low level of interest rates and rising incomes are keeping debt service low.

The personal savings rate was 10.3 percent in the third quarter, up from the second quarter and extending a mild uptrend

The personal savings rate, savings as a percentage of disposable personal income, came in at 10.3 percent in the third quarter as measured by the flow-of-funds report. In the second quarter, the savings rate was 10.0 percent. This measure is broader than the monthly measure from the Bureau of Economic Analysis that is often quoted.

On a three-year moving-average basis (to dampen quarterly volatility), the personal savings rate was 10.2 percent, up from 9.8 percent in the second quarter. The rate has been trending moderately higher since hitting a relative low of 9.0 percent in the fourth quarter of 2017. In a longer-term perspective, the three-year average has been bouncing around in the 9 to 12 percent range since the end of the last recession. That is a solid improvement over the 6 to 9 percent range for the 1999 to 2008 period but well below the 15 to 18 percent range that prevailed for most of the period from 1965 through 1990.

The measure of personal savings from the Bureau of Economic Analysis shows a rate of 7.9 percent for the month of November 2019, the latest data available. On a three-year average basis, the rate was 7.5 percent, well below the rate measured in the flow-of-funds report. The difference is due to definition and methodology differences, but the movements in the rates are generally similar. Personal savings rates are trending higher recently and are higher than in the early 2000s but well below the rates of the mid-1960s through 1990.

Nonfinancial corporate stock buybacks continued in the third quarter

U.S. nonfinancial corporations continued a brisk pace of stock buybacks in the third quarter. Net equity issuance, gross issuance minus buybacks, totaled $572.3 billion at an annual rate in the latest period. That brings the four-quarter total to $2.2 trillion.

Measured as a percentage of total market capitalization of equities, the third-quarter came in at a -1.9 percent pace. That extends a run of 40 consecutive quarters, and 67 of the last 69 quarters, of negative net issuance. However, over that period, the average decline was -2.0 percent and covers a range of -5.8 percent to 1.4 percent, making the third quarter about average for the last 15 years.

Historically, net equity issuance was positive from 1952 through 1976. From 1977 through 1983, net equity issuance had mixed periods of positive and negative results. From 1984 through 1990, nonfinancial corporate equity net issuance was sharply negative as a percentage of market capitalization, running 28 consecutive quarters, and posting results in the -1.6 percent to -7.9 percent range and averaging -1.2 percent.

Total nonfinancial corporate liabilities-to-assets ratio near all-time high.

Total liabilities for the nonfinancial corporate sector rose 1.3 percent in the third quarter, less than the 1.8 percent gain in total assets. That result pushed the ratio of liabilities to assets down to 62.3 percent from 62.6 percent at the end of the second quarter. However, at 62.3 percent, the ratio is just 0.7 percentage points below the all-time high of 63.0 percent from the third quarter of 2018, and well above the 25 to 28 percent range during the late 1950s.

The liabilities-to-assets ratio rose sharply from the upper 20s in 1960 to 60 percent in 2000. The ratio fell sharply in the early 2000s, hitting 49.4 percent in 2006. The ratio has moved sharply higher since 2006, hitting a high in 2018.

Some of the increase is likely a reaction to the very low interest rates on corporate debt. The risk is that should interest rates rise significantly, issuing new debt to replace maturing debt could dramatically increase interest expense (much like the Federal government). Some corporations may be able to issue equity instead of rolling over maturing debt, but that would dilute shareholder value and could hurt share prices.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.