Income Inequality Rightly Understood

Senators Elizabeth Warren (D-MA) and Bernie Sanders (I-VT) have long advocated wealth taxes on unrealized capital gains, in their view, to make the rich “pay their fair share.” President Biden included such a tax in his 2023 budget, though the House ultimately removed it. The idea of a wealth tax is perennially popular in some circles, despite its dubious constitutionality and the invasive powers it would give the IRS to collect and appraise inventories of everyone’s wealth and property. Some will remain discontented as long as wealth is not distributed perfectly equally, and taxing the haves will always be an attractive source of government revenue, while redistributing benefits helps politicians gain votes.

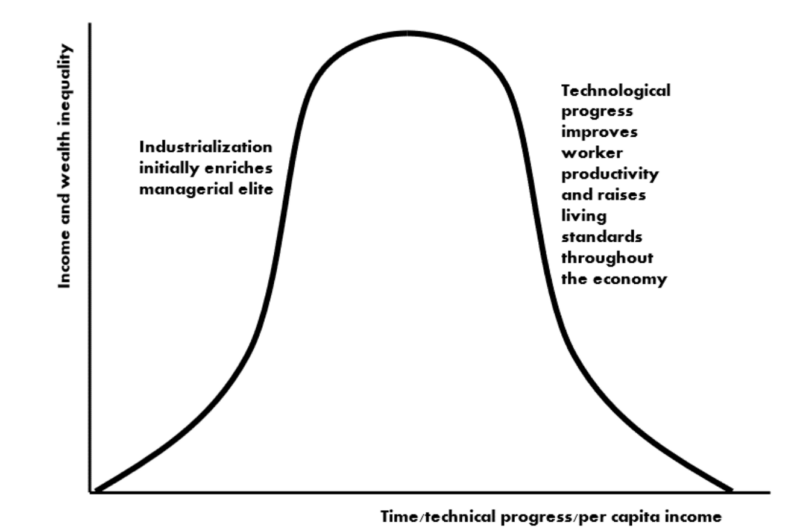

American economist Simon Kuznets (1901-1985) suggested income inequality should rise as an economy experiences initial industrialization. Until the industrial revolution, most of humanity was trapped in the crushing poverty of subsistence agriculture. Technological progress finally allowed increasing percentages of the population to enjoy higher standards of living. As most of the rewards of economic growth were initially captured by the wealthiest property owners, entrepreneurs, and capitalists who founded and managed the new industries, Kuznets noted that income and wealth would become more concentrated and income inequality would rise. However, this inequality eventually falls as technology becomes widely adopted throughout the economy. Scientific progress improves worker productivity, and workers benefit through higher wages and a rising standard of living. He illustrated this process of technological progress and growth with the Kuznets curve (Figure 1).

This increase and subsequent decrease in income inequality was observed generally from 1870-1970, but some measures suggest income inequality has risen since then. For example, rising compensation to CEOs and other executives increased as a multiple of full-time employees’ average wage, especially in the US, inviting increasing criticism and attention. Scrutiny of high and purportedly excessive executive compensation is invariably linked with concern regarding income inequality.

In his work on income inequality, Thomas Piketty attempted to reconstruct historical time series for shares of income among different population demographics, and his choices of data and data adjustments were not just arbitrary, but consistently biased in favor of his thesis of increasing inequality. Better data and less problematic adjustments suggest wealth concentration was either growing after 1980 far slower than Piketty concluded, or that it continued to fall. The questionable accuracy of Piketty’s data also calls into question his proposed policy solution, a tax on accumulated wealth.

Piketty’s data analysis is riddled with errors of historical fact, poor methodological choices, and opportunistic selectivity which aims to construct non-existent patterns from data which are at best ambiguous, and in some cases indicate precisely the opposite of what Piketty claimed to observe. When faced with a choice of primary series or algebraic transformations to use to join them, Piketty et al invariably choose whatever made it look like inequality was rising most rapidly.

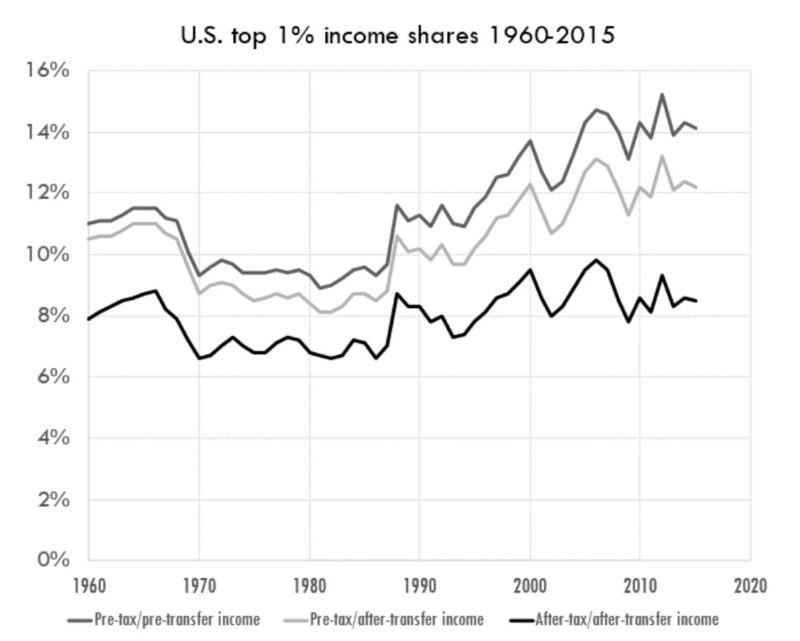

Income inequality has become increasingly controversial. However, once adjusted for taxes and government transfers, US income shares have been relatively stable from 1960-2015 (Figure 2). The progressive income tax and many government transfer payments are designed to redistribute income from the highest to lowest-earning individuals by lowering disposable income for the highest-earning and raising it for the lowest-earning. Before adjustment for taxes and transfers the income share for the highest one percent of the population appears to be rising from roughly 1985-2015, but when taxes and transfers are accounted for, the highest earners’ income share has not increased very much, if at all. Since the US relies more on a progressive income tax and less on regressive sales taxes than virtually every other country, it is especially important to make these adjustments to US data. Income shares have been relatively stable for most industrialized economies since approximately 1900.

Most arguments against income inequality fail to consider whether that gap was created by growth-enhancing productive activities which benefit the whole of society, or from unproductive rent-seeking which diminishes worker productivity and economic growth. Rent-seeking is the pursuit of income based on government favoritism to obtain contracts, revenue, and other favors that they don’t earn from voluntary market transactions. Rent-seeking occurs whenever an industry lobbies the government for subsidies, favorable tax treatment, restrictive licensing, or regulation which protects established firms from competition. These measures provide the lobbying organizations additional income without creating added value for society. Rent-seeking shields less-productive organizations from competition and enables them to extract higher prices from the public.

Some of the worst examples of rent extraction are zoning laws (which make housing artificially expensive by restricting the supply) and the Jones Act (which requires limits who can ship goods to US ports). Barring foreign competition has locked in reliable profits for US shippers, but shrank that domestic fleet from 250 ships in 1980 to just over 90 today – from a policy aimed at “protecting and preserving” domestic shipping. While failing to accomplish that goal, the Jones Act makes everything Americans buy more expensive, particularly gasoline and heating oil. Everyone loses except the rent seekers.

Rent-seeking organizations also use bribery and political contributions to obtain legislation or regulation that shields them from competition. Any discussion of income inequality that fails to address whether the source added value for others or simply extracted unearned rents, is not merely incomplete, but misleading.

Clearly there’s a big difference between wealth that derives from corporate welfare and rent-seeking, and wealth derived from entrepreneurial innovation that consumers willingly reward because it benefits them. A wealth tax narrowly focused on lessening inequality fails to distinguish one from the other. Taxing productive value will make all of us poorer.

Robert F. Mulligan

He is the author of Entrepreneurship and the Human Experience and Executive Compensation. Both books can be purchased through Amazon either in hard copy or as a Kindle eBook.