How Much Independence Has Fed Lost?

The NBER released a bombshell working paper Monday morning that most (but not all) of the media missed. Its authors claim that the Federal Reserve is not very independent of executive control anymore, and they can prove it.

That might sound like some pretty arcane stuff, but it is of crucial importance to our nation’s future, at least if a popular theory about constraints on inflation is correct.

That theory, which appears in most undergraduate Money and Banking textbooks, including my own, posits that central banks sufficiently insulated from political pressures have the ability and desire to keep inflation in check. More independent central banks indeed tend to have a better record on inflation.

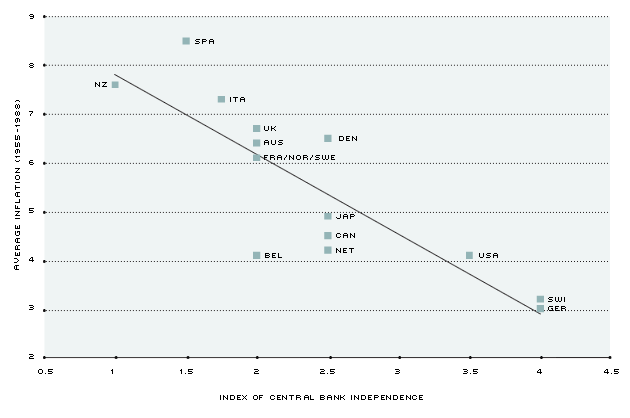

This is how the St. Louis Fed depicts the relationship using data from 1955-1988 (referencing the classic 1993 paper on the subject by Alesina and Summers):

One problem, though, is that researchers often kind of eye-ball the independent variable (central bank independence), the variable on the horizontal axis. The Federal Reserve is not as independent as The European Central Bank, the story commonly runs, because the latter is mandated by treaty while the former exists only by virtue of statute. Look at the U.S. Constitution and you will see nothing about having a central bank, much less details about its structure. In fact, the U.S. went some 8 decades without a central bank. That said, the Fed seems more independent than some other nation’s central banks because it has control over its own budget, its governors serve a single, long term, and so forth.

The genius of the recent NBER paper, by Duke’s Francesco Bianchi and London Business School’s Howard Kung and Thilo Kind, is that it directly measures the effect of President Donald J. Trump’s tweets critical of the Federal Reserve on the Federal Funds Rate, a key overnight interbank interest rate.

They find that his Twitterstorms have lowered Federal Funds futures contracts by about 10 basis points (.1 percent), an economically significant amount given that the Fed typically adjusts its target in 25 basis points (.25 percent) increments. They conclude that market participants believe that erosion of the central bank’s independence is “significant and persistent.”

This paper presents novel market-based evidence that President Trump impacts expected monetary policy with a strong expansionary bias typical of politically motivated agendas. Our high-frequency identification approach relies on a large collection of unique tweets from the President criticizing the conduct of monetary policy in conjunction with tick-by-tick fed funds futures prices over the past two years. The collected tweets ardently pressure the fed to lower interest rates. High-frequency changes in expectations of the fed funds target across horizons are extracted from the futures prices of different maturities. An event study is conducted by constructing a small time window around the precise at the second timestamps of each tweet to assess the reaction of the expected fed funds target before and after each tweet. The cumulative effect of the collected tweets implied our estimation is around negative 10 bps over the past year, with the effect growing over time and horizon. Our findings suggest that market participants believe that the erosion to central bank independence is significant and persistent.

In other words, market participants behave as if they expect that the Federal Reserve eventually will succumb to pressure from POTUS and loosen monetary policy. That does not bode well for the Fed’s independence and hence its ability to fight inflation, which has been a key factor in the dollar’s international dominance since the abandonment of the gold exchange standard in the early 1970s.

A weak, unwanted dollar would be especially troubling now, given America’s chronic budget deficits, ballooning debt, and looming entitlement funding crises. Of course if the President stopped hurting the real economy with his trade war, he might not need to tweet so hard to gin up production artificially with easy money policies.

Robert E. Wright

Robert E. Wright is the (co)author or (co)editor of over two dozen major books, book series, and edited collections, including AIER’s The Best of Thomas Paine (2021) and Financial Exclusion (2019). He has also (co)authored numerous articles for important journals, including the American Economic Review, Business History Review, Independent Review, Journal of Private Enterprise, Review of Finance, and Southern Economic Review. Robert has taught business, economics, and policy courses at Augustana University, NYU’s Stern School of Business, Temple University, the University of Virginia, and elsewhere since taking his Ph.D. in History from SUNY Buffalo in 1997. Robert E. Wright was formerly a Senior Research Faculty at the American Institute for Economic Research.

Find Robert

- SSRN: https://papers.ssrn.com/sol3/cf_dev/AbsByAuth.cfm?per_id=362640

- ORCID: https://orcid.org/0000-0003-3792-3506

- Academia: https://robertwright.academia.edu/

- Google: https://scholar.google.com/citations?user=D9Qsx6QAAAAJ&hl=en&oi=sra

- Twitter, Gettr, and Parler: @robertewright