Is this the End of Globalization?

In a speech, entitled What is behind the recent slowdown?, given in Berlin on 14th May 2019, Hyun Song Shin, Economic Adviser and Head of Research at the Bank for International Settlements (BIS) discussed the weakening of global value chains (GVC’s) in manufactured goods. The manufacturing sector is critical; it still accounts for 70% of global merchandise trade:

During the heyday of globalisation in the late 1980s and 1990s, trade grew at twice the pace of GDP. In turn, trade growth in manufactured goods was driven by the growing importance of multinational firms and the development of GVCs that knit together the production activity of firms around the world.

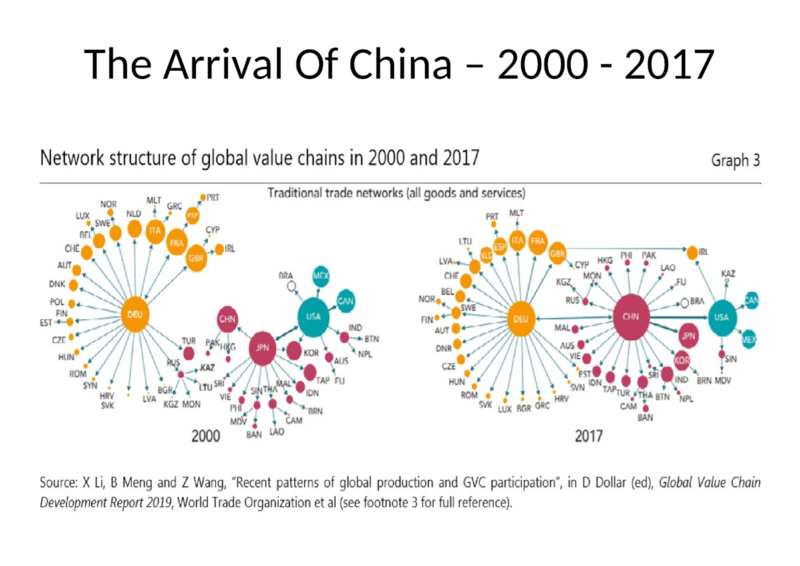

The infographic below shows how the rise of China has transformed the structure of the global supply chain during the last two decades:

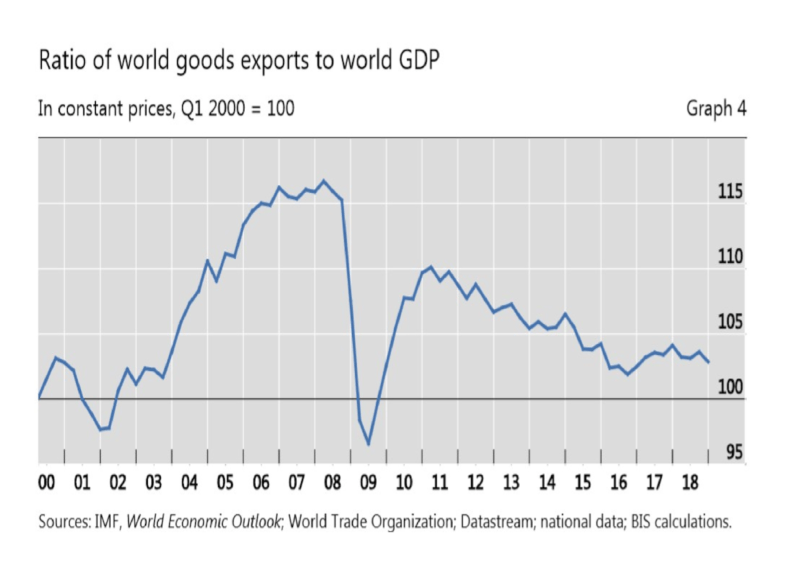

When seen through the lens of a developed country manufacturing worker, whose very livelihood has been hollowed out by the comparative advantage of imported goods, the recent trade war between the US and China is long overdue. However, the reversal in the globalisation of trade has been in train since long before the arrival of the current US President. The chart below shows the decline in world goods exports relative to world GDP since the great financial crisis of 2008:

Hyun goes on to describe the inherent fragility of GVC’s (the emphasis is mine):

Long and intricate GVCs have many balls in the air, necessitating greater financial resources to knit the production process together. More accommodative financial conditions then act like weaker gravity for the juggler, who can throw many more balls into the air, including large balls that represent intermediate goods with large embedded value. However, when the shadow price of credit rises, the juggler has a more difficult time keeping all the balls in the air at once.

When financial conditions tighten (as they did in the wake of the great financial crisis) GVC’s shorten. Production is on-shored or re-shored. During the past three months, as China has grappled with the COVID-19 pandemic, the truncation of GVC’s has accelerated. Resiliency has eclipsed efficiency as the need for certainty of supply has shattered many of the Ricardian assumptions of the past century.

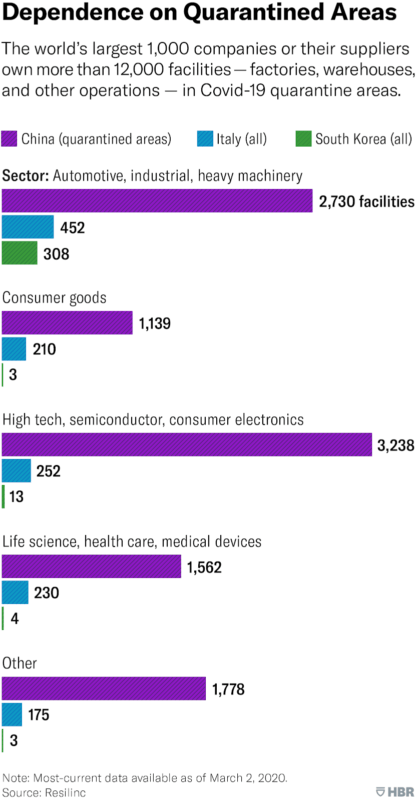

Many commentators have argued that globalisation allowed the world economy to become overly optimised. Looking ahead to the end of the current crisis, the pandemic may achieve what US tariffs have not, a complete re-evaluation of the logistics of global trade. The HBR infographic below highlights the magnitude of the disruption as early as 2nd March. At that stage only China, South Korea and Lombardy had entered lockdown: –

In the Harvard Business Review article which accompanied this infographic, Coronavirus Is Proving We Need More Resilient Supply Chains, the authors, Tom Linton and Bindiya Vakil, recommend that companies invest in mapping and monitoring their global suppliers. They advocate the adoption of Artificial Intelligence and Natural Language Processing techniques to help identify weaknesses and bottlenecks. The cost of mapping and monitoring is substantial but the benefits of flexibility can be justified by the savings which can be gleaned from reduction in inventory and improvements in the agility of response to abrupt changes in customer demand.

In the first few weeks of January 2020, companies that had mapped their supply chain already knew which parts and raw materials were originating in the Wuhan and Hubei areas and, as a result, could bypass the frantic hunt for information and fast-track their responses.

The coronavirus epidemic teaches us — once again — that a robust supplier-monitoring system that maps sub-tier dependencies is a basic requirement for today’s supply chain and sourcing professionals.

On February 29th The Economist, Covid-19 is teaching hard lessons about China-only supply chains, highlighted weaknesses in the global pharmaceuticals supply chain. The authors note that a large share of global antibiotic supply is produced by a cluster of Chinese firms based in Inner Mongolia. China is also the world’s dominant producer of active pharmaceutical ingredients.

Robustness and adaptability will not be achieved without cost but in the brave new antifragile world, protection against the next global continuity shock will be a central tenet of prudential risk management. We are about to enter a new age of dual supply-chain redundancy.

Another trend which has been evident for several years will also gain additional impetus; technology has been displacing workers throughout history but this process is likely to accelerate in the wake of the corona crisis. For developed countries, the labour-cost savings of manufacturing overseas has been diminishing as emerging market wages rise. Developed nation robotics, machine learning and artificial intelligence will continue to displace low-cost workers in developing and frontier countries.

In his July 2019 essay for Project Syndicate, In Praise of Demographic Decline, Adair Turner observes:

Our expanding ability to automate human work across all sectors – agriculture, industry, and services – makes an ever-growing workforce increasingly irrelevant to improvements in human welfare. That’s good news for most of the world, but not for Africa.

The author goes on to suggest that for countries in demographic decline, automation of manufacturing processes is an economic boon, whereas for countries with rising fertility it is an impediment to improvements in their per capita standard of living.

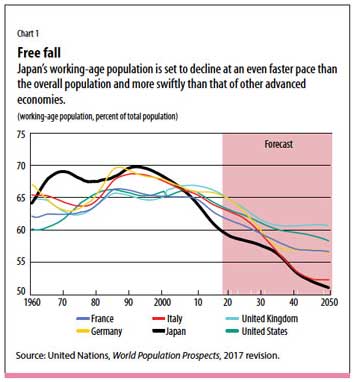

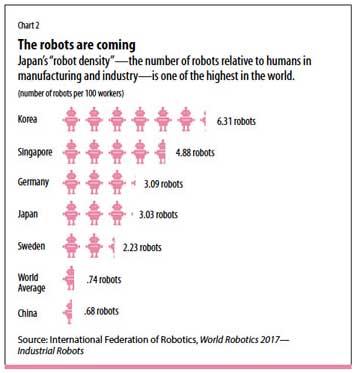

As with many trends among developed countries, Japan, where deaths outnumber births by an average of 1,000 people per day, is in the vanguard in embracing technology to counter the demographic deficit. The shortening of GVC’s will simply hasten their innovation in automation. Where Japan leads other developed countries will follow. The chart below shows the decline in working age population for the six largest developed nations:

If the table below is any guide, robots are destined to absorb a significant proportion of the slack:

In their June 2018 article on Japan, published by the IMF, Land of the Rising Robots, Todd Schneider, Gee Hee Hong, and Anh Van Le conclude:

…the wave of change is clearly coming and will affect virtually all professions in one way or another. Japan is a relatively unique case. Given the population and labor force dynamics, the net benefits from increased automation have been high and could be even higher, and such technology may offer a partial solution to the challenge of supporting long-term productivity and economic growth.

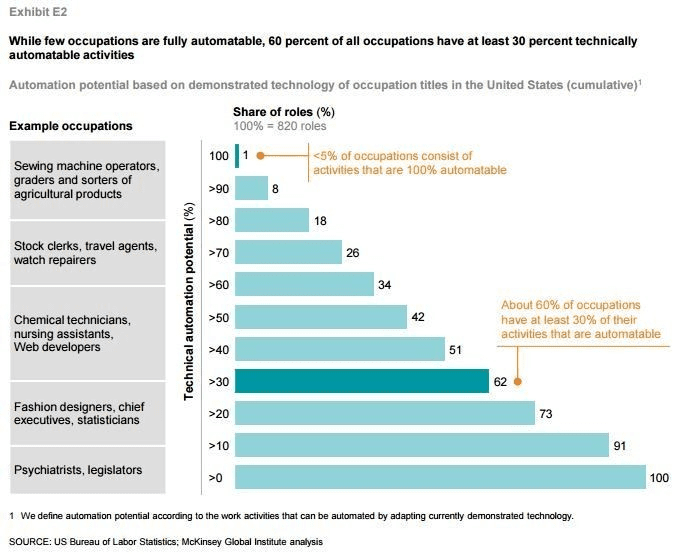

The changes in the nature of employment, resulting from what some are describing as the Fourth Industrial Revolution, will be profound. This infographic from McKinsey attempts to assign a probability of automation to roles which are currently performed by US workers:

As GVC’s shrink and dual supply-chain redundancy raises costs, the cost-benefit of automation will decline; ‘home-grown’ automated manufacturing will augment and, in certain circumstances, replace the existing long and fragile GVC’s.

This transition from global back to more local supply chains will take time. In the COVID-induced interim a recession is almost inevitable. At the household level inventory has been accumulated – just visit a supermarket near you; shelves bereft of produce like some scene from a documentary of market failure in the USSR. For businesses, inventories are diminishing as they draw down on essential parts and components. Several production lines are at a standstill, and stresses are evident globally. This disruption has ceased to be merely an economic issue, as it begins to impact our national security. In Washington and Brussels questions are being asked about the risk of outsourcing too much, too far and to too few manufacturers.

In an article, published earlier this month for Foreign Affairs, Henry Farrell and Abraham Newman suggest, The Pandemic Is Exposing Market Vulnerabilities No One Knew Existed, pointing out that for globalization to be successful it must necessarily also be fragile. The geopolitics of globalisation has suffered a sea-change, as yet it is unclear what form the new rules of engagement will take. What seems clear is that the nation state is far from dead; it is alive and strident and remains fundamentally self-interested. What had appeared to be concrete economic and political alliances were quickly swept aside.

For investors the challenge of the last month has been extreme. Government bonds rallied and then retraced as the magnitude of the fiscal cost of the pandemic materialised. Stocks imploded, ignoring central bank attempts to stabilise prices. Even safe haven assets such as gold failed to provide much safety as liquidity drove everything, which had previously rallied, to fall.

In order to preserve value, there have been predictable bans on short selling in some markets and calls to close stock exchanges in others. In an article for the AIER, Richard Ebeling makes a plea that, To Kill Markets Is the Worst Possible Plan, I fear several of his predictions and few of his recommendations will come to pass.

For the moment, a massive wave of fiscal stimulus and the prospect of more to follow seems to have caused stock markets to pause. There are pockets of phenomenal value to be found, both in terms of dividend yields and low price-to-earnings ratios among well-managed, solvent corporations. Value investors, who have waited patiently for almost a decade, will find a wealth of opportunity.

Many less well-managed firms will finally diminish despite zero interest rates. Already those companies which have been buying back their own stocks are faring less well than those who choose to pay dividends to their loyal investors. The age of financial alchemy may not yet be over, nor is the process of globalisation at an irretrievable end, but the rules of engagement are changing rapidly.

Colin Lloyd

Colin is a macroeconomic commentator, writer and presenter, based in London, England. He has worked for asset managers in commodities, money markets, capital markets, equities and foreign exchange since the early 1980’s and writes In the Long Run. He is a contributor to several free-market publications including The Cobden Centre and was a 2017 runner-up for the 2017 Richard Koch Breakthrough Prize awarded by The Institute of Economic Affairs.