Economics is Not Easy

I often have conversations with people who ask what I do. When I tell them, many say, “Oh, wow, I don’t know much about economics!”

Here is a blanket endorsement: Look, folks, when you tell me that, I believe you.

But for some reason almost everyone then continues on and proves their claim of ignorance. Folks want to say things about the economy, or policy, that sound plausible, but which are in fact deeply misleading. The problem is that economics is not easy, and a lot of things that “make sense” are just dead wrong.

I have been struck by this in the past couple of weeks as a weird debate plays out on Twitter and other social media. Some people are worried about inflation, some are worried about Fed policy to fight inflation, and others are using the discussion as a forum for proving they know nothing about economics.

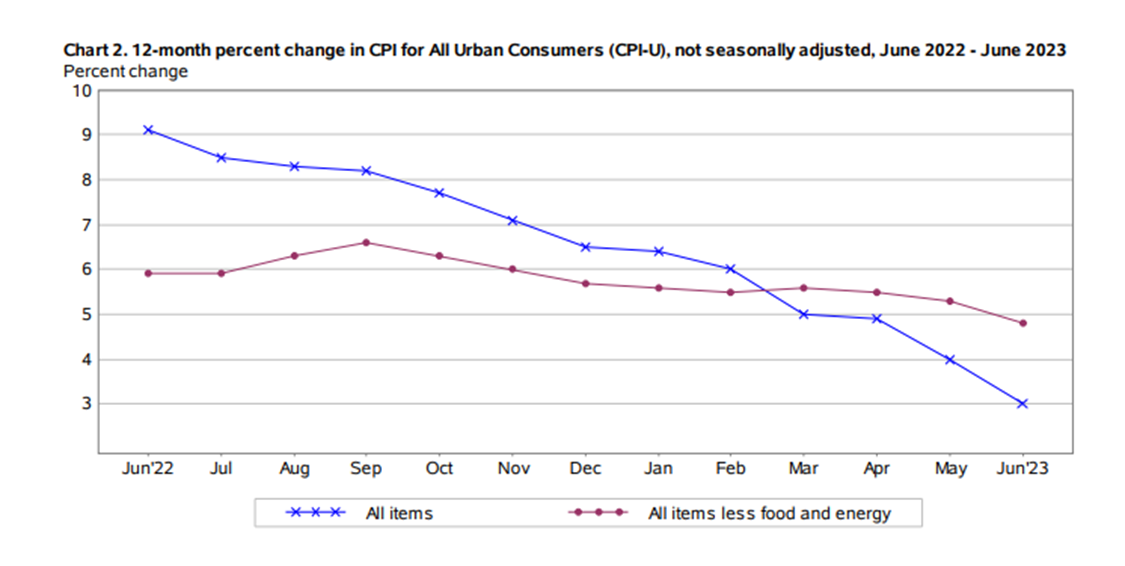

The chart below is from a Bureau of Labor Statistics report; there are several important things about the data it shows, but I am only going to hit the highlights.

Source: The Bureau of Labor Statistics (BLS)

When fuel prices were high last summer, it became a trope for many people that inflation was being caused by the greed of oil companies. Well, looking at the chart, it appears that the oil companies have become much, much less greedy. And inflation has persisted, even though this supposed causal chain (greed causes high prices causes inflation) has been broken.

Further, whatever the cause(s), inflation remains stubbornly high, not by world standards but by comparison to the government target of 2 percent, or at most 3 percent sustained price increases.

In fact, the oil and food price increases of last year were caused by the war in Europe, supply chain interruptions, and government shutdowns of attempts to restart the economy. Now that all that has abated somewhat, there is still an underlying problem: money.

There are two fundamental truths of macroeconomics, and while we can sometimes work around them, they are surprisingly resilient and robust. First, inflation, at least in the sense of a sustained increase in the overall price level over long time periods, is caused by artificial and unwise increases in the money supply. Second, increases in the overall price level are often misread by entrepreneurs and business people as increases in the actual demand for their specific products.

That’s not surprising when you think about it. The price for the widgets you make is going up fast, and you want to expand your factory and hire more workers. But you have trouble doing that, because the blodget makers, and the whatsit makers are all trying to do the same thing. Austrian economists call this the problem of “correlate errors,” where market participants are fooled by inflation into thinking that there is a “real” increase in the demand for their specific product.

To be fair, inflation of this sort can be self-correcting because the sharp increase in wages as all industries simultaneously compete for scarce workers prevents many firms from carrying out their misguided plans for expansion. But the upward pressure on wages, and prices, is an illusion. Since everyone looks to prices for accurate information about relative scarcity, having prices that are being inflated artificially is misleading, and results in multiple different economic actors all trying to expand at once.

Inflation is Not Really Wage Growth

Is it plausible to think that there has been such a large growth in the US money supply that the increase in prices is old-fashioned inflation, rather than a real expansion of economic activity? Consider the table below, from the St. Louis Fed “FRED” website:

The “monetary base” has increased before; it was increased by $1 trillion in 2009 in response to the “Great Recession.” But look at 2020: The monetary base increased by $3.5 trillion in two years. That is an unimaginable infusion of currency into the hands of banks, companies, and …well, almost everyone, when you consider the enormous transfers and “stimulus funds” shoveled out during the COVID shutdown. The government had a highly expansionary fiscal policy, accommodated by an even more highly expansionary monetary policy from the Federal Reserve.

The resulting inflation (and even Paul Krugman admits now he was wrong, and that there really has been substantial inflation) has sent out a misleading economic signal to owners of inputs, owners of factories, and owners of labor services (that is, workers): “EVERYBODY WANTS YOU!”

But it’s not real. The signal of increased price, which looks like an overall increase in demand, is just a lot more money chasing the same amount of goods, which bids up prices across the board.

An American Enterprise Institute Senior Fellow named Michael Strain commented this week on the situation. Strain recognized that inflation was no longer increasing, but pointed out—perfectly plausibly—that “the labor market and consumer demand remain too strong.”

That’s when the trouble started. The immediate response (for example, see this Tweet and comments) was to go all populist class war on the claim that the labor market was “too strong.” The problem is that no one is claiming that real (that is, adjusted for inflation) wages are too low. It would be great if workers had substantial pay increases, provided those increases were the result of increased productivity and real increases in demand for those widgets and blodgets. But the problem here is that the “increased demand” is imaginary, the result of inflation. Rather than an increase in the relative price of my product, in my industry, there is a general price increase. Strain’s claim that the labor market is “too strong” may have had unfortunate wording, but it’s basically correct.

Imagine that you were going to run a one-mile race. To prepare, you drink a bunch of coffee, and as soon as the starting gun goes off you sprint as fast as you can. For several hundred yards, buoyed by the artificial stimulant of the caffeine, you are way out in front. But you are running too fast, you can’t keep that up, and you start to wear out the artificial stimulant. In the third lap, everyone else catches you, and you come in last.

You talk to your coach later: “What went wrong?”

The coach says, scornfully, “You ran too fast.”

But you are incredulous: “Ran too fast? It’s a race! Don’t you understand that running fast is the point?”

The coach sighs, and tries to explain. Sure, you want to run fast. But the race has to be run at a sustainable pace, saving enough energy for a kick in the last lap. Going at a dead sprint is actually wasteful, and using coffee artificially speeds you up for a little while, but in the long run you produce less speed, and come in last.

Well, as I hope is obvious, in an inflationary period the labor market is “too strong” because the stimulus of increased demand for workers is artificial, like caffeine, and cannot be sustained. The “boom” caused by the misperception of increased demand for your product will quickly dissipate, and the industry will slow down, laying off even more workers than it hired, and come in last. Compared to a sustainable pace, a pace actually capable of producing real growth rather than inflation, the labor market is artificially stimulated. Economics is not easy. Understanding the problem of correlated errors, and the government-policy-induced cycle of boom and bust, requires something more than expressing a misplaced populist outrage on behalf of workers. Worst of all, unless inflation is controlled on a long-term basis, it is workers who will suffer most, as the consequences of the artificial stimulus hurt real economic growth.

Michael Munger

Michael Munger is a Professor of Political Science, Economics, and Public Policy at Duke University and Senior Fellow of the American Institute for Economic Research.

His degrees are from Davidson College, Washingon University in St. Louis, and Washington University.

Munger’s research interests include regulation, political institutions, and political economy.