Business Conditions Monthly June 2023

June 2023 saw expansion in both AIER’s Leading and Roughly Coincident Indicators, with the Lagging Indicator falling to a slightly contractionary bias.

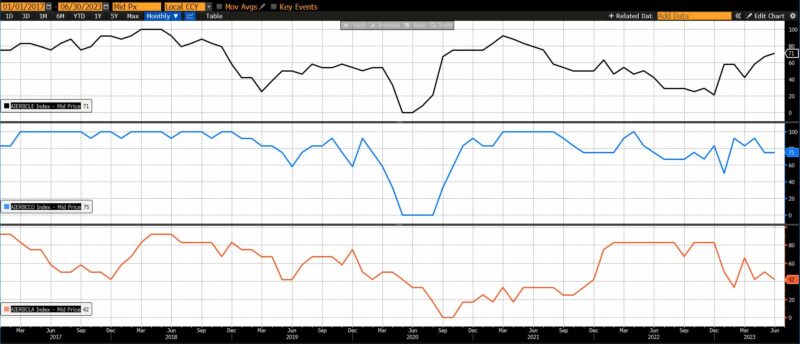

AIER’s Leading Indicator rose to 67 in May to 71 in June, its highest value since July 2021. After languishing at contractionary levels for the second half of 2022 with levels below 30, with the exception of March 2023 the index has expanded in most categories. Our Roughly Coincident Indicator has, since October of 2020, remained above 50 but bounced between 58 and several readings of 100. More recently, since mid-2022, the index has averaged in the mid-60s, with February and April 2023 generating readings over 90. It maintained a level of 75 from May to June 2023.

The AIER Lagging Indicator rose from 42 in April to 50 in May, shifting from mildly contracting to a neutral bias. In June 2023 it returned to 42.

AIER Business Conditions Monthly (5 years)

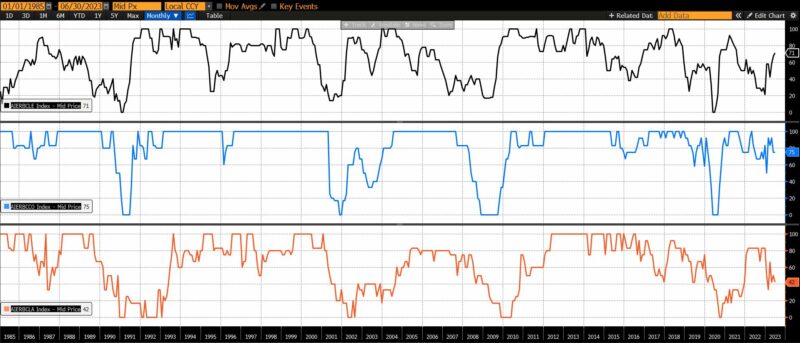

AIER Business Conditions Monthly (1985 – present)

Leading Indicators (71)

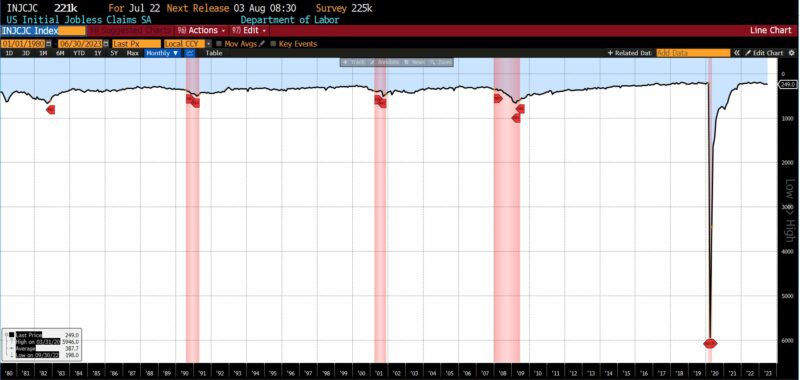

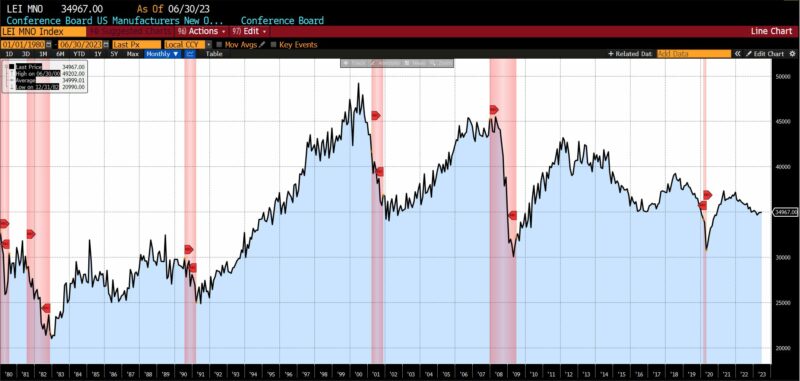

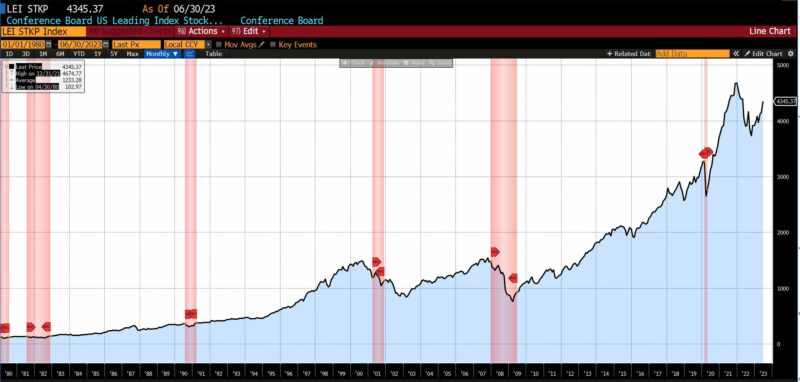

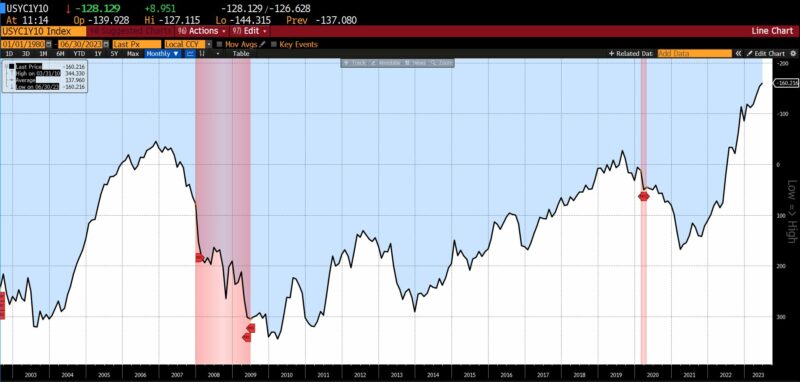

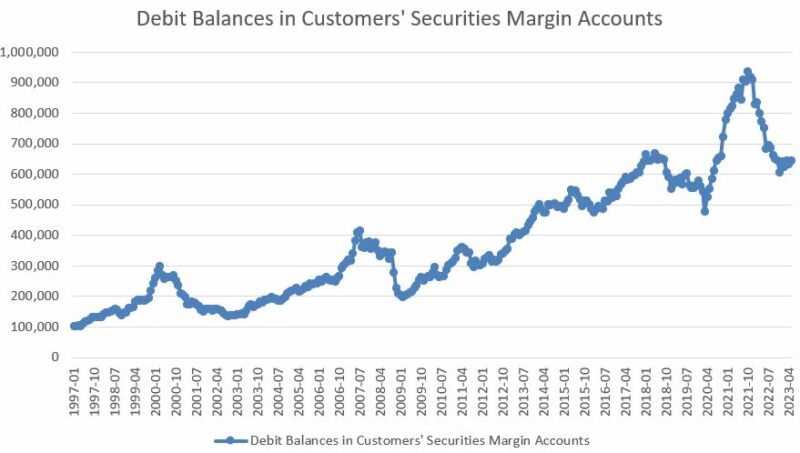

Among the twelve Leading Indicators seven increased, two decreased, and three were essentially unchanged. Among rising components were the University of Michigan Consumer Expectations Index (11 percent), US Initial Jobless Claims (7.8 percent), the Conference Board US Leading Index of Manufacturing New Orders for Consumer Goods and Materials (0.1 percent), the Conference Board US Leading Index of Stock Prices of 500 Common Stocks (4.8 percent), the US Census Bureau’s Adjusted Retail and Food Services (0.2 percent), the 1-to-10 year US Treasury spread (4.2 percent), and debit balances in brokerage margin accounts (5.8 percent).

The Bureau of Labor Statistics US Average Weekly Hours (All Employees, Manufacturing), the Conference Board Leading Index of Manufacturers New Orders for Nondefense Capital Goods ex Aircraft, and the Census Inventory to Sales Ratio (total business) were unchanged from May to June 2023.

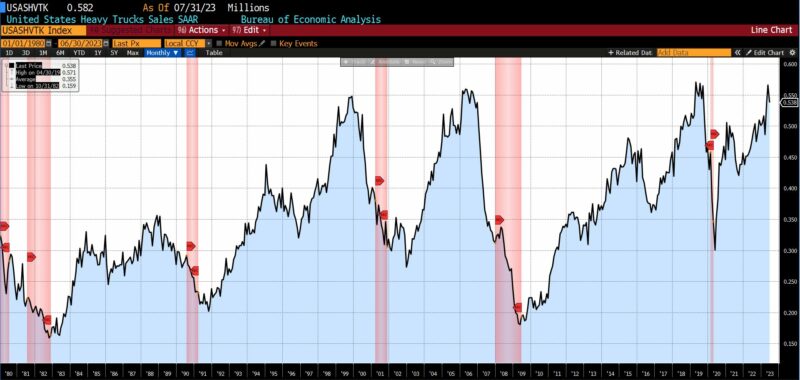

The declining components of the Leading Indicators were the US New Privately Owned Housing Units Started by Structure (-8.0 percent) and the Bureau of Economic Analysis’ US Heavy Truck Sales (-4.9 percent).

Roughly Coincident (75) and Lagging Indicators (42)

From May to June 2023 four of the six components of the Roughly Coincident indicators rose, one was unchanged, and one declined.

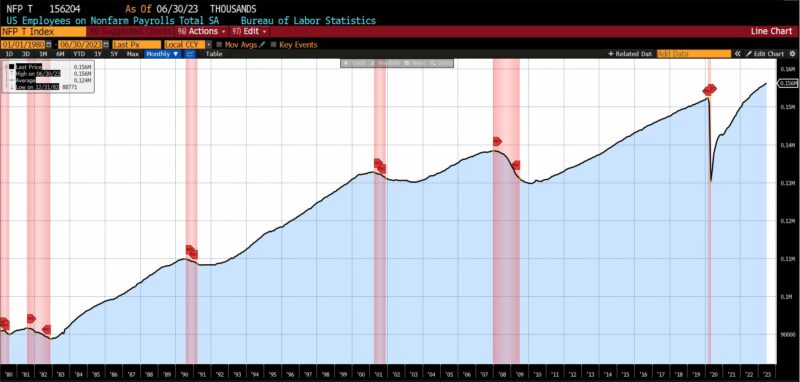

The three Conference Board components of this index increased: Coincident Manufacturing and Trade Sales up 0.26 percent, Coincident Personal Income Less Transfer Payments up 0.25 percent, and the Consumer Confidence Present Situation up 4.3 percent. Total US Employees on Nonfarm Payrolls, published monthly by the Bureau of Labor Statistics, also rose by 0.13 percent.

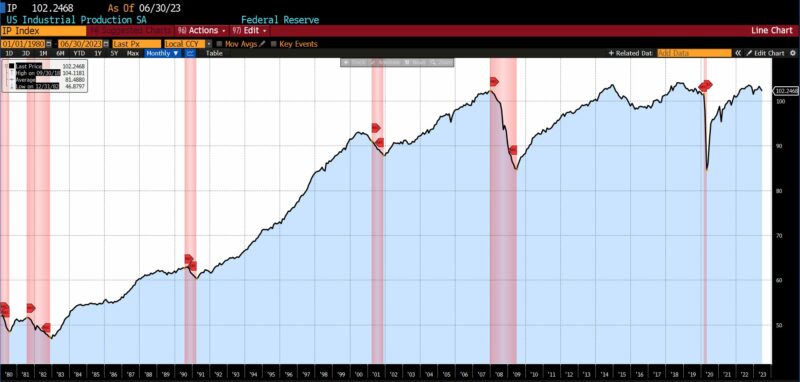

The Federal Reserve’s Industrial Production Index declined by 0.54 percent, and the US Labor Force Participation Rate was unchanged in June.

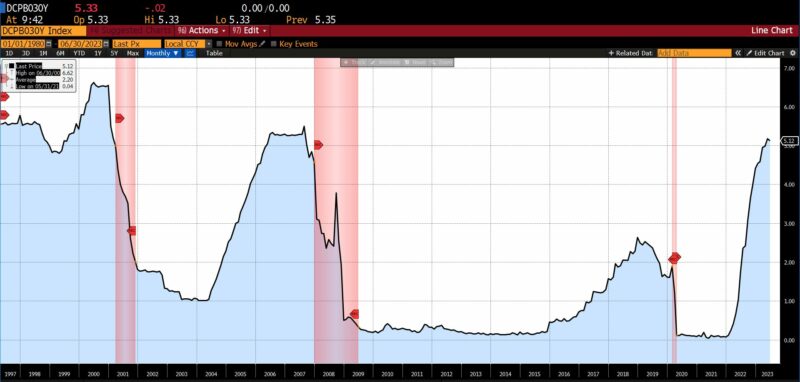

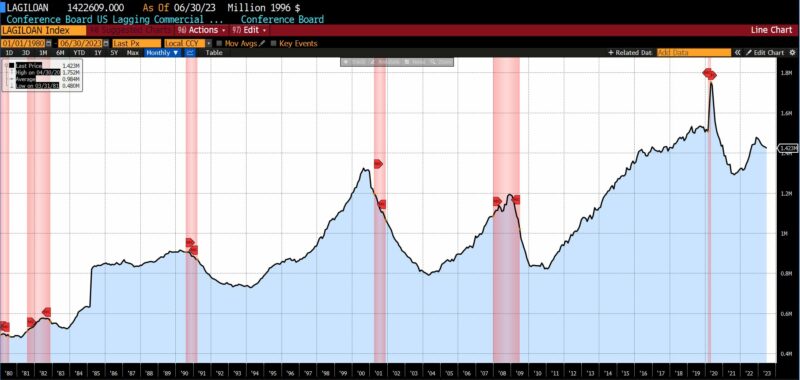

Among the six Lagging Indicators, core CPI, 30-day average yields, and the Conference Board’s US Lagging Commercial and Industrial Loans declined by 9.4 percent, 1.0 percent, and .42 percent respectively. The Conference Board’s US Lagging Average Duration of Unemployment rose by 2.3 percent while the US Census Bureau’s US Manufacturing and Trade Inventories increased by 0.2 percent. And the Census Bureau’s US Private Construction Spending (Nonresidential) for June fell 0.03 percent.

June 2023 saw expansion in both AIER’s Leading and Roughly Coincident Indicators. The Leading Indicator has been in a general uptrend since December 2022 after a long, sloping downtrend which began in March 2021. The Roughly Coincident Indicator, meanwhile, has been in positive territory since the start of 2023, while the Lagging Indicator has generated monthly values alternating between neutrality and contraction in its constituents with the exception of March 2023 (66).

Discussion

In light of strong consumer spending, historically low unemployment, a construction boom, and a steady disinflationary trend, a growing number of economic forecasters have dialed back their predictions of a late 2023 recession in favor of soft landing scenarios. Another, smaller camp has shifted sharply and is now forecasting a reacceleration of the US economy. Last week’s unexpectedly strong 2.4 percent 2nd quarter 2023 US GDP has added to hopes that the Fed’s contractionary policy regime, now entering its sixteenth month, will soon have the general price level back to its target range without a substantial (or to some, any) economic slowdown.

In the March 2023 Business Conditions Monthly (Volume LXXXIV), we expressed the following view, citing trends in our three indicators as well as employment diffusion, the growing gap between consumers’ present confidence and expectations, the rate of economic growth versus short-term interest rates, the decline in the quality of corporate earnings, and a handful of other economic metrics:

US economic fundamentals are now clearly deteriorating, with risks compounding to the downside. The current baseline estimate is for an economic recession within the next twelve to eighteen months [September 2024].

Despite the rapid embrace of these altered projections, we maintain the above position for the reasons which follow.

-

- 2nd Quarter GDP

The first estimate of the 2nd quarter US GDP number (2.4 percent) mandates a look under the hood. Consumer spending contributed 1.1 percent to the reading, despite falling from 4.2 percent in the 1st quarter of 2023 to 1.6 percent in the second. Durable goods spending, however, fell from 16.4 percent in the 1st quarter of 2023 to 0.4 percent in the 2nd quarter. With pandemic savings dwindling, the student loan payment moratorium ending in September/October 2023, and delinquencies on car loans rising, American consumers are likely to be hard pressed to continue their acquisitive ways in the remainder of 2023 and into 2024.

Nonresidential fixed investment added 1 percent to 2nd quarter GDP. But a substantial amount of the 7.7 percent increase in new private structures and equipment spending is tied to three legislative measures passed under the Biden administration. The Bipartisan Infrastructure Act (signed in November 2021), which provides up to $550 billion over the next five years on transportation, broadband, and public works; the Inflation Reduction Act (signed in August 2022), which provides up to $500 billion in Federal spending and tax breaks for green/sustainable projects; and the CHIPS and Science Act (also August 2022) which will provide up to $280 billion in spending on semiconductor foundries over the next decade.

The Biden administration’s industrial policy foray, ostensibly to reverse the decline of American industrial heft in the global marketplace, is a superficiality. The rapid slide in the percentage of the US workforce employed in manufacturing over the past five decades has vastly more complex origins than the number of physical structures that exist.

Investment in physical plant and equipment paid for/spurred on by industrial policy and dwindling consumer firepower thus account for roughly 2.1 percent of the 2.4 percent 2nd quarter GDP number. Whether viewed as a representation of current output or a foundation for future growth, the disproportionate contribution of two questionable sources of growth to that measure do not paint a particularly encouraging picture.

-

- The Senior Loan Officers Opinion Survey (SLOOS)

According to the Federal Reserve’s 2nd quarter SLOOS results, banks are tightening credit standards. The percentage of banks reporting tightening standards for commercial and industrial loans increased from 46 percent in the 1st quarter of 2023 to just under 51 percent in the current quarter. The top reasons for tightening among respondents were: 1) Less favorable/more uncertain economic outlook; 2) Reduced risk tolerance; and 3) Deterioration in current or expected liquidity position. The number of respondents citing “concerns about legislative changes” jumped from 38.3 percent in the first quarter to 54 percent in the second quarter. Just over 40 percent of respondents expressed their intention to tighten lending standards sometime during the second half of 2023. The ability to tap credit in support of continued consumption is likely to deteriorate in the coming two to four quarters.

-

- Manufacturing weakness

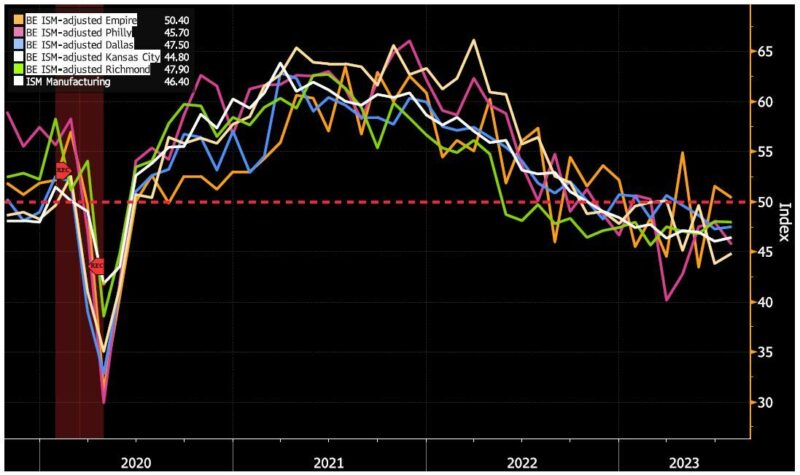

The Institute for Supply Management’s (ISM) Purchasing Managers’ Index fell for a ninth straight month in July to 46.4. While new orders and production improved slightly in July, the indices remain in contractionary territory. Also in July 2023 the ISM Index of Factory Employment fell to its lowest reading (44.4) since July 2020. Industrial production fell from September 2022 to December 2022, recovered a bit through April 2023, and has fallen since. As demand for durable goods has declined, factory output has slowed with wholesalers and retailers accumulating less inventory.

The recent trend in the overall ISM Purchasing Managers’ Index as well as five regional totals (Empire/New York, Philadelphia, Dallas, Kansas City, and Richmond) are displayed below. Weakness in manufacturing is seen across all areas and spreading.

The recession forecast made in March 2023 was cast with a longer time horizon than most others at the time (18 months versus six to 12 months). This was a purposeful choice made on account of our expectation that in the post-pandemic era the combined effects of pent-up demand, extended policy lags, and other factors might take longer to manifest. At present we continue to believe that the US will enter a recession by September 2024, but will adjust our perspectives if and when necessary as new data and facts become available.

LEADING INDICATORS

ROUGHLY COINCIDENT INDICATORS

LAGGING INDICATORS

CAPITAL MARKET PERFORMANCE

AIER-BCM-June-2023Download

(All charts and data sourced via Bloomberg Finance, LP)

Research-Reports_2023_07Download

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Research Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.