Auto Sales Fell Slightly in November but Remain at a High Level

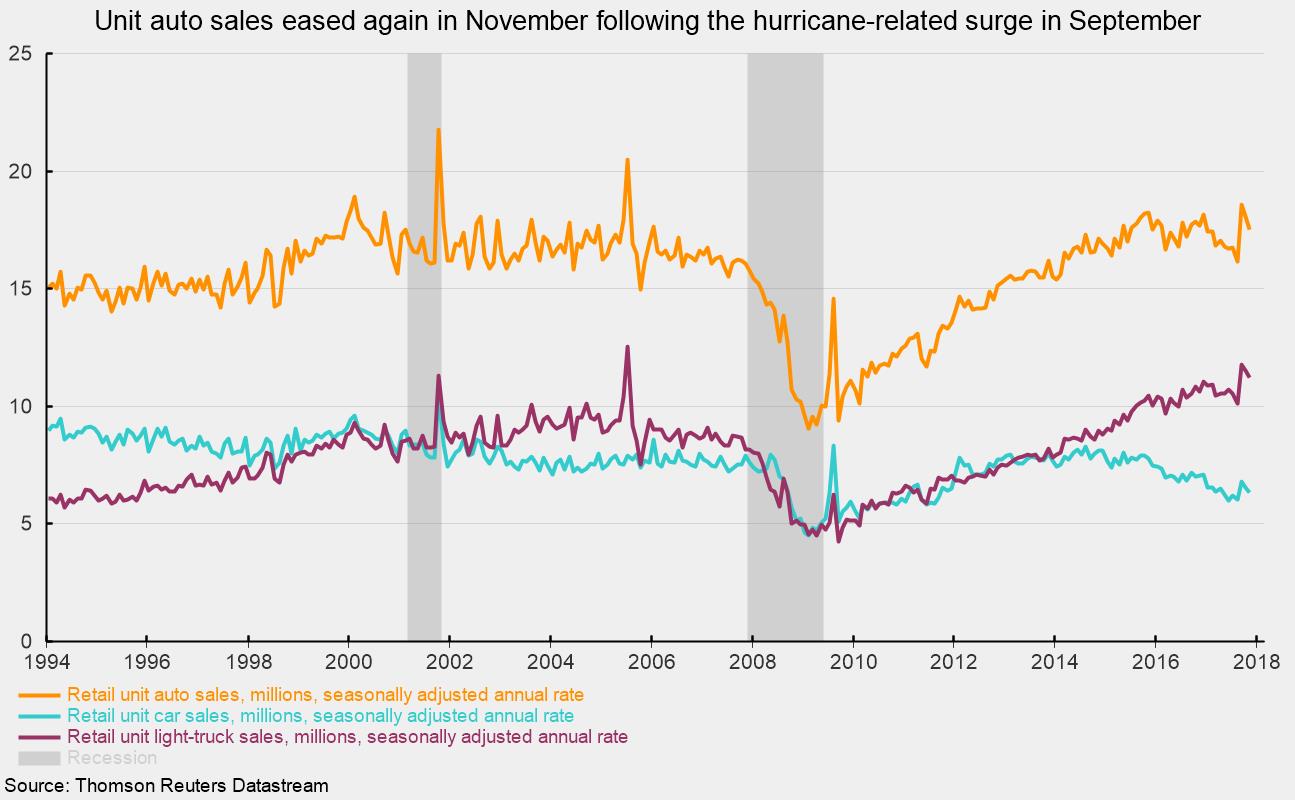

U.S. retail unit auto sales fell slightly for the second month in a row in November after jumping to a 12-year high in September. The September surge was largely due to the replacement of vehicles damaged during and after Hurricanes Harvey and Irma. Despite the slowing over the latest two months, auto sales remain at a high level by historical comparison.

For the first 11 months of 2017, unit auto sales have averaged 17.2 million annualized following record results of 17.4 million and 17.5 million in 2015 and 2016, respectively. Sales suffered through an eight-month downtrend, slowing from an 18.2 million rate in December 2016 to 16.1 million in August 2017 — a drop of 11 percent. September 2017 sales surged to 18.6 million, the highest monthly result since July 2005. The last two months have seen sales ease back to 18.1 million in October and 17.5 million in November.

The November decline came from sales of cars and light trucks, both domestically produced and imported. Light trucks continue to be the dominant segment, accounting for 63.9 percent of auto sales. They posted an annualized selling rate of 11.2 million units in November, with domestic light trucks accounting for 9.2 million, or 81.8 percent, of retail light-truck sales. Imported light trucks posted a 2.0 million rate for the month.

Passenger-car sales fell to a 6.3 million-unit annualized pace versus a 6.6 million rate in October. Among passenger cars, domestic cars came in at 4.6 million while imports sold at a 1.7 million pace. Domestic passenger cars account for 73.0 percent of total passenger-car sales.

Overall, despite the decline in unit auto sales, the relatively high level is a positive sign for consumer spending and the economy in general heading into the first quarter of 2018.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.