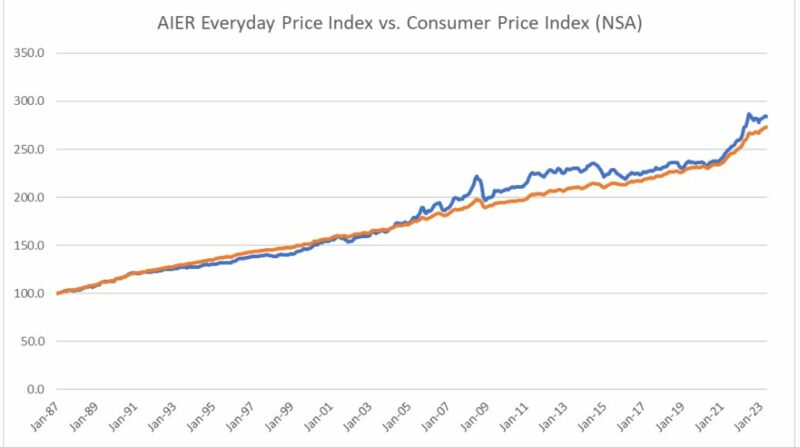

AIER’s Everyday Price Index Declines Slightly in May 2023

AIER’s Everyday Price Index (EPI) fell 0.09 percent in May 2023 after rising for three of the first four months of this year. At its current level, 284.1, the EPI is up 1.4 percent on a year-over-year (May 2022 to May 2023) basis.

Within our proprietary index, the constituents seeing the largest price gains from April 2023 to May 2023 were nonprescription drugs/vitamins, recreational reading materials, and video discs/other media. The largest price declines over the past month occurred in domestic services, motor fuel, and household fuels/utilities.

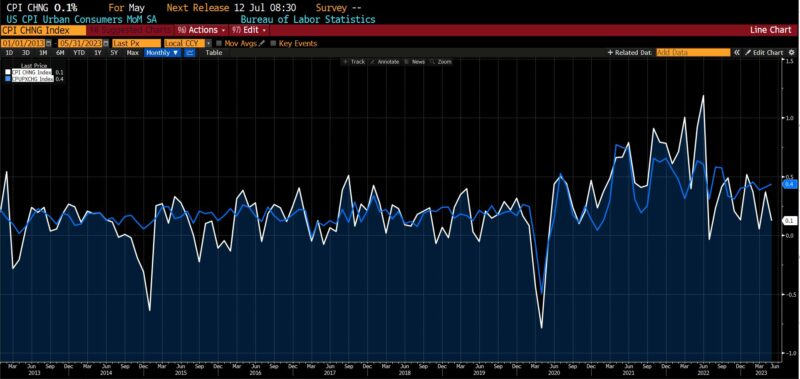

One June 13th, the US Bureau of Labor Statistics (BLS) released the May 2023 Consumer Price Index (CPI). The month-over-month headline CPI showed an increase of 0.1 percent, which met expectations. The core CPI (ex food and energy) increased by 0.4 percent, which also met expectations. The biggest increases in headline CPI prices between April and May 2023 took place in shelter and used car/truck prices, with a slight uptick in food prices. Prices of headline CPI constituents declining to the greatest extent over that same time period were energy prices broadly, most notably in gasoline.

Core CPI saw its largest price increases in shelter, used cars and trucks, motor vehicle insurance, apparel, and personal care items. The most pronounced decreases in prices took place in household furnishings and airfare.

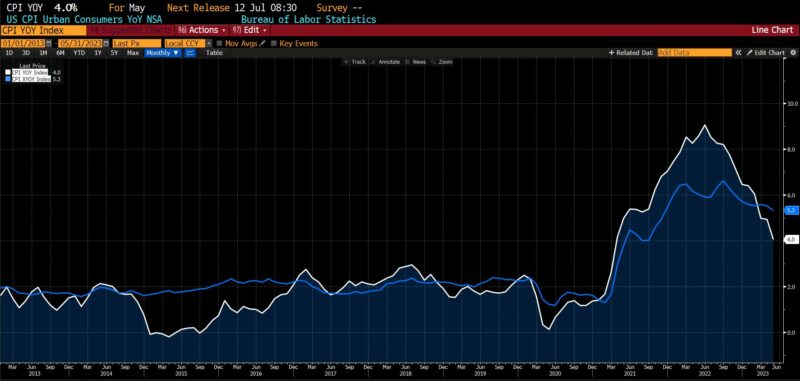

On a year-over-year basis, between May 2022 and May 2023 headline CPI increased by 4.0 percent, slightly lower than expectations of a 4.1 percent increase. The core CPI, however, was slightly higher than expectations, increasing by 5.3 percent versus an expected 5.2 percent increase. Of note, the May 2023 headline CPI increase was the smallest such increase since March 2021. May 2023 is additionally the third month in a row in which the year-over-year core CPI exceeded the year-over-year headline CPI.

The Federal Reserve’s rate hiking operation is now in its sixteenth month. With the policy rate target between 5.0 and 5.25 percent, its highest in sixteen years, borrowing costs have steepened as money supply measures are contracting at their fastest rates in decades. As of April 2023, M1 has contracted by 9.8 percent on a year-over-year basis while M2 has contracted at a 4.6 percent rate year-over-year.

A slew of contradictory data muddying the assessment of the monetary tightening measures has recently been released. While US GDP has averaged just over 1 percent growth for the last five quarters, the May 2023 nonfarm payrolls came in at 339,000, beating estimates of 195,000 new jobs by one of the largest margins on record. Similarly, consumers have proven resilient even despite increases in both credit card delinquencies and bankruptcies. Wages rose at an annualized rate of almost 5 percent in the first quarter of 2023, while the pandemic era burst of productivity (working from home, increased automation) has dissipated. Yet despite upward pressure on wages and declining productivity, corporate profits (even measured by the earnings-per-share of S&P 500 firms) have remained largely stable.

It is widely expected that at the June 2023 Federal Open Market Committee (FOMC) meeting a decision will be made not to “pause” but rather to “skip” an additional 25 basis point rate hike, revisiting the possibility in July 2023. At that time there may be more macroeconomic clarity, and at any rate more data on both the pace and uniformity of disinflation across goods and services will be available.

Note: As of the 13 June 2023 release of the CPI data, the EPI constituent drawn from the US CPI Gardening and Lawncare Services NSA was unavailable. Both Bloomberg and the US Department of Labor Statistics were alerted to this omission. In the May 2023 calculation of the EPI, the US CPI Gardening and Lawncare Services NSA (Wage Earners) was used in its place. Once an affirmative determination has been made as to whether the previous measure will return or be replaced by this index, the appropriate update will be made to the EPI calculation and announced.

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Research Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.