AIER Everyday Price Index Hits All-Time Record in March 2024

The AIER Everyday Price Index saw its third largest increase in over a year in March 2024, shooting up 0.82 percent. That rise brings our proprietary inflation index to a new record high of 289.2, surpassing the previous high of 288.60 reached in September 2023.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

The largest price increases among the constituents of the Everyday Price Index in March 2024 were seen in motor fuel, food away from home, and internet services/electronic information providers. The largest declines occurred in housekeeping supplies, residential telephone services, and food at home. Among the twenty-four index components, sixteen rose in price while eight declined.

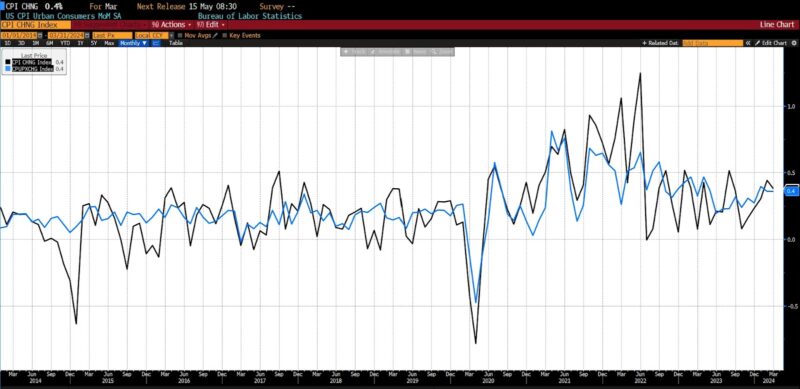

The US Bureau of Labor Statistics (BLS) released Consumer Price Index (CPI) data for March 2024 on April 10, 2024. All four of the primary release metrics, core and headline both month-over-month and year-over-year, were higher than forecast by 0.1 percent. Both the headline and core month-to-month CPI numbers rose 0.4 percent versus an expected 0.3 percent.

Among headline categories, in March 2024 the food index saw a slight increase of 0.1 percent, with food at home remaining unchanged, though three out of six major grocery store food group indexes decreased while the remaining three experienced price advances. Other food at home decreased by 0.5 percent, primarily due to a significant 5.0 percent decline in butter prices, while cereals and bakery products saw the largest one-month seasonally adjusted decrease ever reported. Meats, poultry, fish, and eggs rose by 0.9 percent, driven by a 4.6 percent increase in egg prices, while nonalcoholic beverages increased by 0.3 percent, and fruits and vegetables by 0.1 percent. The food away from home index rose by 0.3 percent in March, following a 0.1 percent increase in February, with limited service meals rising by 0.3 percent and full-service meals by 0.2 percent.

The energy index increased by 1.1 percent in March 2024, driven by a 1.7 percent rise in gasoline prices (which saw a 6.4 percent increase before seasonal adjustment), while electricity prices rose by 0.9 percent and natural gas remained unchanged. However, the fuel oil index experienced a decrease of 1.3 percent in March.

Amid core categories on a month-over-month basis, motor vehicle insurance saw a notable increase of 2.6 percent, continuing its upward trend from February. Apparel prices also rose by 0.7 percent, alongside personal care, education, and household furnishings and operations. However, the medical care index saw a modest rise of 0.5 percent, while used cars and trucks experienced a decline of 1.1 percent, and various other categories such as recreation, new vehicles, and airline fares also saw decreases.

March 2024 US CPI headline & core month-over-month (2014 – present)

From March 2023 to March 2024, headline CPI rose 3.5 percent, higher than the expected 3.4 percent. Year-over-year core CPI rose 3.8 percent, which was also higher than the survey prediction of 3.7 percent.

In food categories over the past 12 months, the food at home index rose by 1.2 percent, with other food at home increasing by 1.4 percent and fruits and vegetables up by 2.0 percent. Nonalcoholic beverages also saw a rise of 2.4 percent, while meats, poultry, fish, and eggs increased by 1.3 percent, and cereals and bakery products by percent. However, the dairy and related products index experienced a decline of 1.9 percent over the year. On the energy front, the index increased by 2.1 percent over the same period, driven by a 1.3 percent rise in gasoline prices and a notable 5.0 percent increase in electricity prices. Conversely, natural gas and fuel oil indexes decreased by 3.2 percent and 3.7 percent, respectively, over the past year.

Over the past year, the index for all items excluding food and energy increased by 3.8 percent, with shelter costs rising by 5.7 percent, contributing significantly to the overall increase. Other notable increases in indexes include motor vehicle insurance (22.2 percent), medical care (2.2 percent), recreation (1.8 percent), and personal care (4.2 percent).

March 2024 US CPI headline & core year-over-year (2014 – present)

Consumer inflation in the US continued its upward trajectory, as reflected in recent government data, dampening expectations for an early interest rate cut by the Federal Reserve, particularly in a politically charged election year.The inflationary pressures are evident across various essential goods and services, with alarming rates recorded in sectors like car insurance (22.2 percent), transportation (10.7 percent), and hospital services (7.5 percent), among others. Both core CPI and headline CPI figures have consistently surpassed forecasts for the past four months, further exacerbated by soaring oil prices nearing $90 per barrel, intensifying concerns about affordability and living costs. Moreover, the US has now endured over three years of inflation exceeding 3 percent, marking the longest period of sustained high inflation since the late 1980s and early 1990s.

AIER’s Everyday Price Index, focusing intently as it does on a narrow range of highly common products and services consumed by Americans, shows the underestimation of upward price pressures by the mainstream, government statistical agencies. In March 2024, our inflation metric increased by more than twice the amount that the BLS core CPI did.

Swap contracts predicting the Fed’s decisions adjusted to higher rate levels, indicating a reduced likelihood of rate cuts, with expectations for the first cut pushed back to July from June. Options traders also shifted their bets, now speculating on just one rate cut this year. Market reactions underscored the shifting expectations, with probabilities for a June rate cut dropping sharply and now favoring a rate adjustment by September. The CME Group FedWatch tool indicates a significant decrease in the likelihood of rate cuts, with fewer than two cuts expected by the year’s end.

It is increasingly clear that the choice to stop rate hikes at the 5.25 to 5.50 policy rate range was at best premature and may ultimately prove insufficient. Should another two or three months of inflation data continue on the current trajectory, the odds of a 0.25 rate hike is likely to materialize as a real, if marginal, possibility.

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Research Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.