Manufacturing Output Surged, Boosting Utilization to a 4-Year High

Industrial production rose 0.3 percent in December, following a 0.4 percent gain in November. Over the past year, industrial production is up 4.0 percent. Total capacity utilization increased 0.1 percentage points to 78.7 percent as capacity posted a 0.2 percent gain for the month.

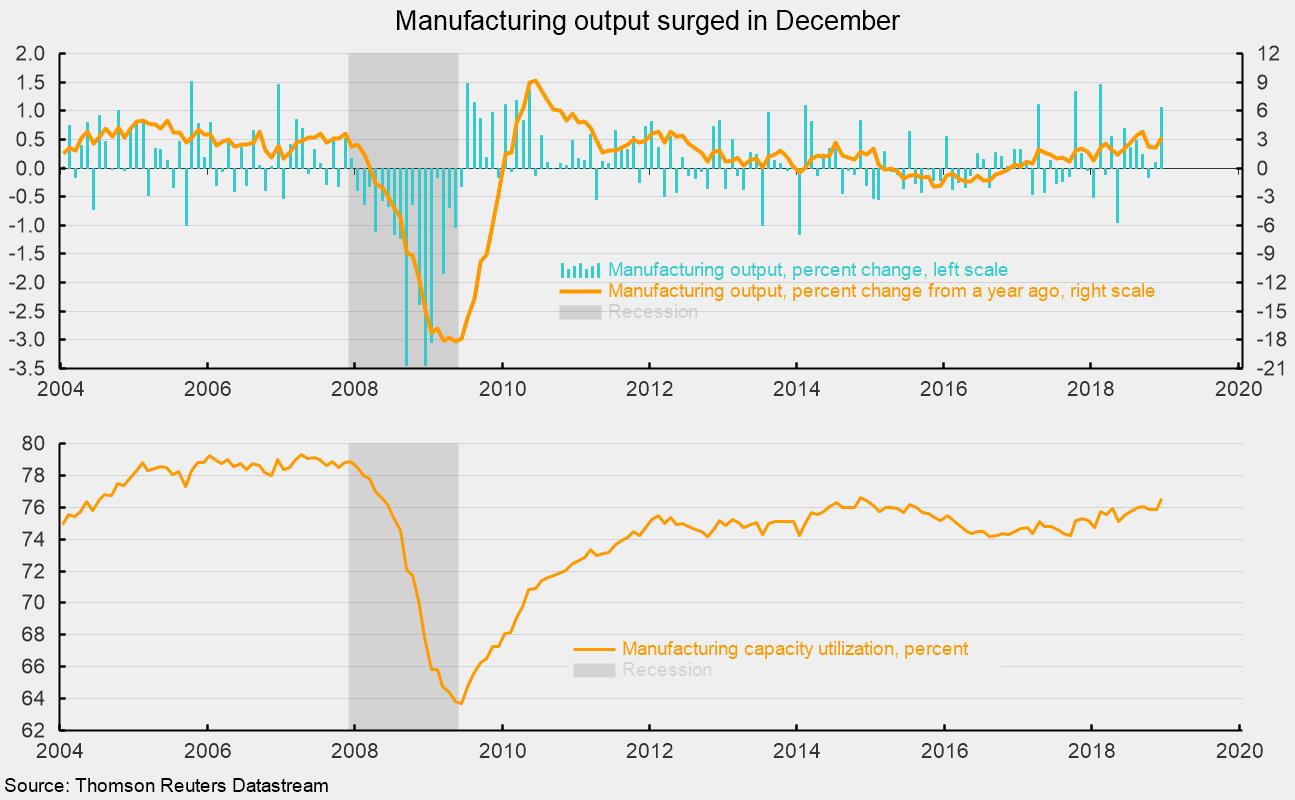

The gain in industrial production was driven by the manufacturing sector, which accounts for about 75 percent of total industrial production. Manufacturing output surged 1.1 percent for the latest month, the largest monthly gain since February 2018 (see chart). Over the past year, manufacturing output has risen 3.2 percent, the third-fastest pace since 2012, continuing a mild accelerating trend since 2016 (see chart). Mining output also posted a strong gain for the month, rising 1.5 percent, while utilities output plunged 6.3 percent in December. Over the past year, mining output is up 13.4 percent while utilities output is down 4.3 percent.

Within manufacturing, durable-goods production rose 1.3 percent while nondurable-goods production moved up by 0.9 percent. Leading the durable-goods production were motor vehicle production (up 4.7 percent), nonmetallic mineral products (up 2.8 percent), and aerospace products (up 1.7 percent). Among nondurable-goods producers, petroleum and coal products rose 3.5 percent while food-products production gained 0.9 percent.

Measured by market segment, consumer-goods production was unchanged in December, with consumer durables up 2.7 percent and consumer nondurables down 0.8 percent. Business equipment rose 0.5 percent in December and is up 5.0 percent from a year ago. The monthly gain was boosted by a 2.9 percent gain in transit equipment. Every category within business-equipment production shows a 12-month gain between 3.4 percent and 10.6 percent — a very solid performance. Construction supplies increased 1.6 percent for the month and is up 2.1 percent over the past year, suggesting a mildly positive outlook.

Materials production (about 46 percent of output) rose 0.5 percent for the month and is up 6.1 percent from a year ago. The energy component has been a major source of volatility in this category, particularly following the collapse of energy prices in mid-2014. The non-energy component rose 0.9 percent for the month and is up 3.7 percent from a year ago.

Manufacturing capacity utilization rose to 76.5 percent in December, up 0.7 percent from 75.8 percent in November. That is the highest reading since 2014 and the second-highest since 2008 (see chart).

Today’s report from the Federal Reserve provides evidence of the continuing gains in the manufacturing sector despite erratic results for some data series. A robust labor market, relatively high levels of consumer and business confidence, generally solid balance sheets for the private sector, and modestly favorable readings from the AIER Leading Indicators index suggest the outlook for continued economic expansion remains cautiously optimistic. The major risks are primarily associated with economic policy (monetary, fiscal, and trade) and global economic uncertainty.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.