Retail Spending Was Strong in October

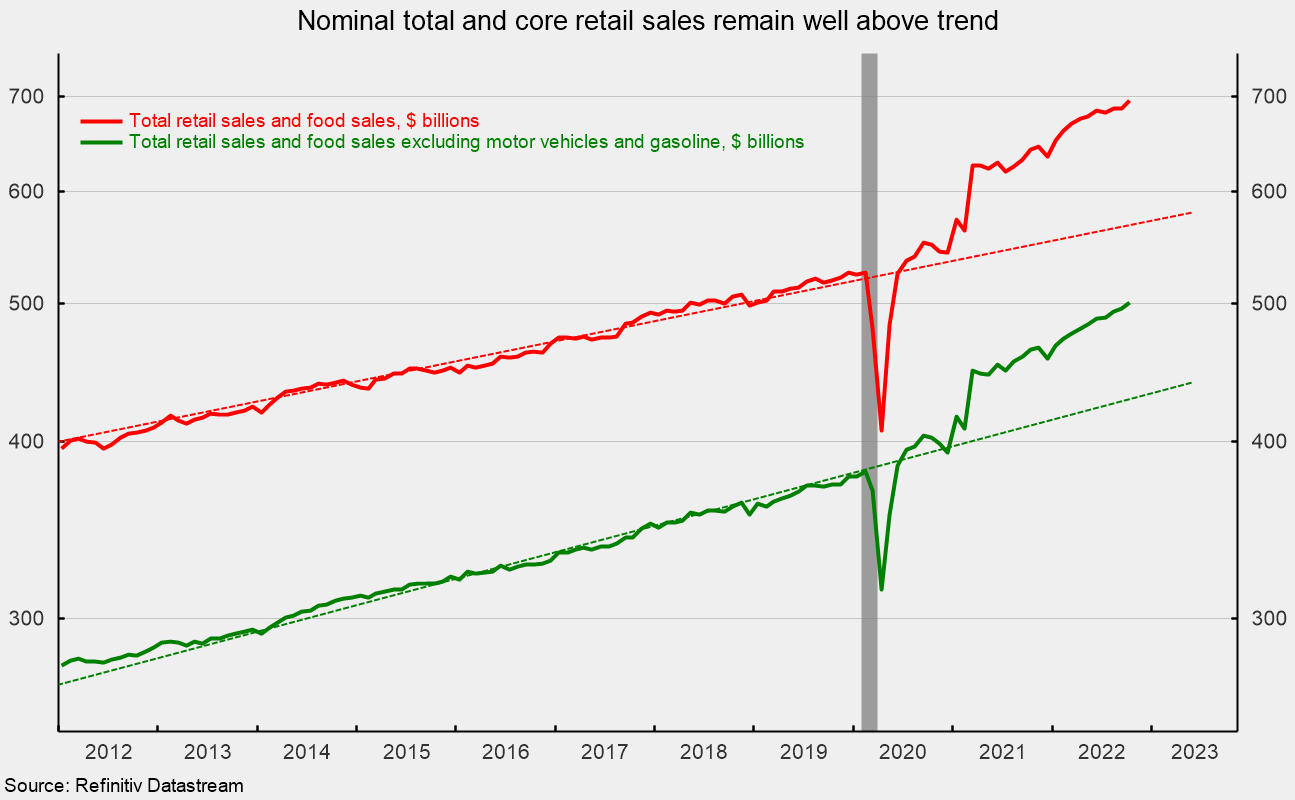

Total nominal retail sales and food-services spending rose 1.3 percent in October after being unchanged in September. From a year ago, retail sales are up 8.3 percent and remain well above the pre-pandemic trend (see first chart).

Nominal retail sales excluding motor vehicle and parts dealers and gasoline stations – or core retail sales – rose 0.9 percent in October following a 0.6 percent gain in September. From October 2021 to October 2022, core retail sales are up 8.0 percent. As with total retail sales, core retail sales remain well above the pre-pandemic trend (see first chart).

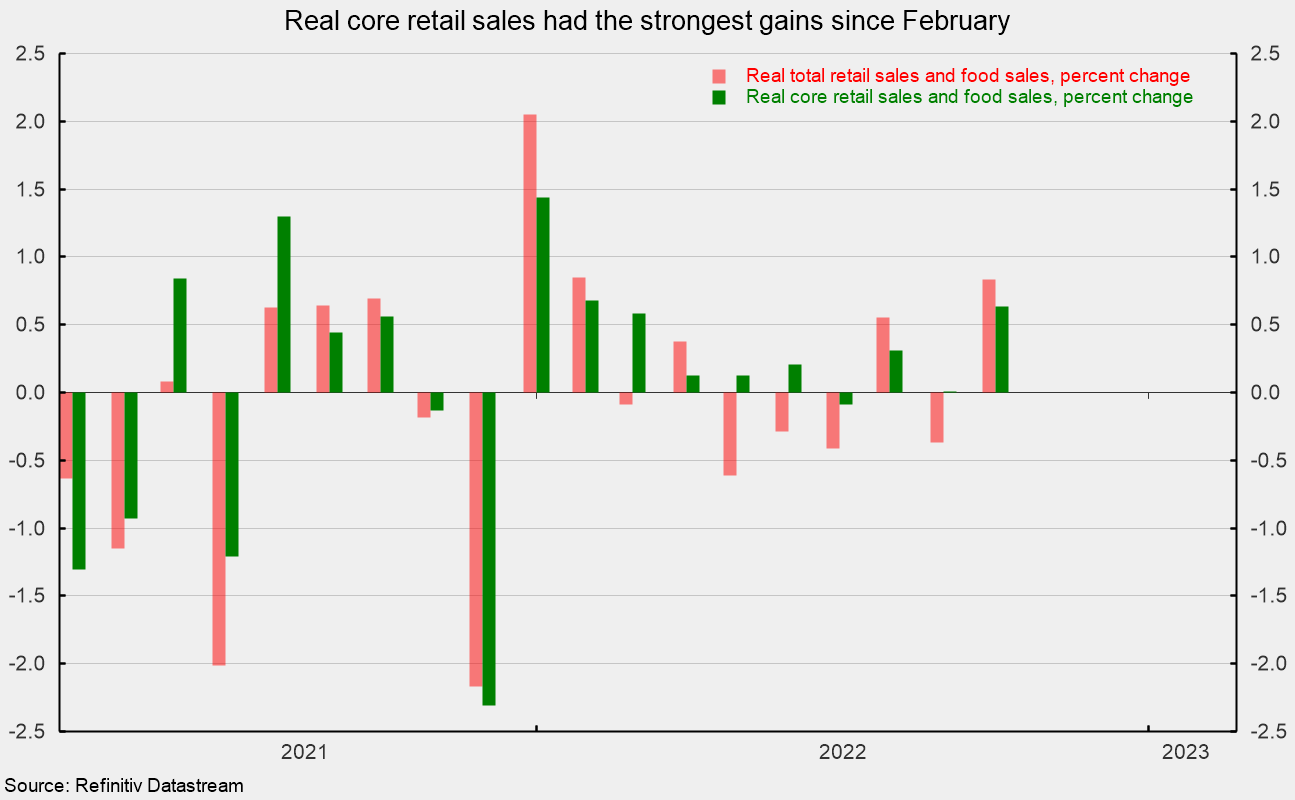

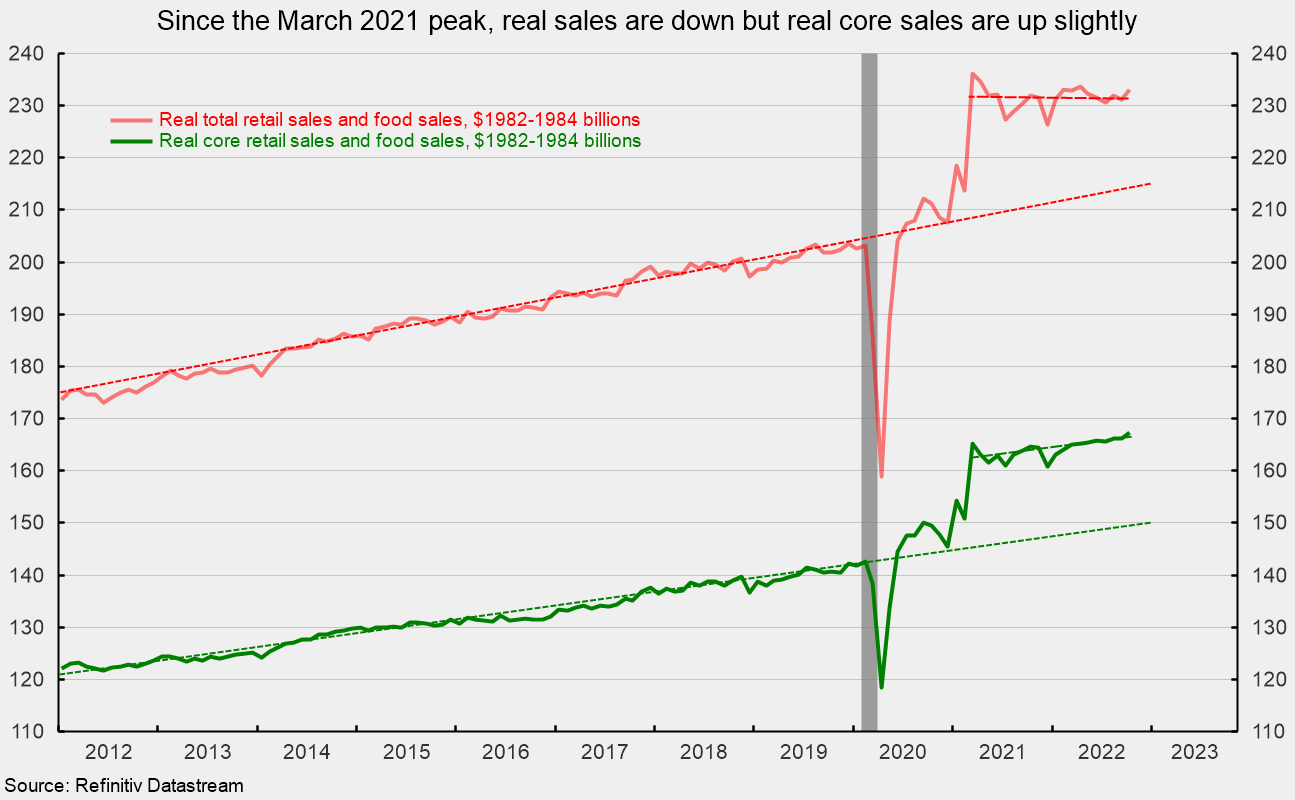

However, these data are not adjusted for price changes. In real terms (adjusted using the CPI), real total retail sales were up 0.8 percent in October following a 0.4 percent decrease in September and declines in five of the last eight months (see second chart). From a year ago, real total retail sales are up 0.5 percent versus a ten-year annualized growth rate of 2.5 percent from 2010 through 2019. As with nominal retail sales, real retail sales remain well above their pre-pandemic trend, but since March 2021, they have been trending flat (see third chart).

Real core retail sales posted a 0.6 percent rise in October after being unchanged in September (see second chart). Over the last twelve months, real core retail sales are up 1.6 percent versus a ten-year annualized growth rate of 2.2 percent from 2010 through 2019. While real total retail sales are still below the March 2021 peak, real core retail sales have been trending higher at a rate of 1.6 percent per year (see third chart).

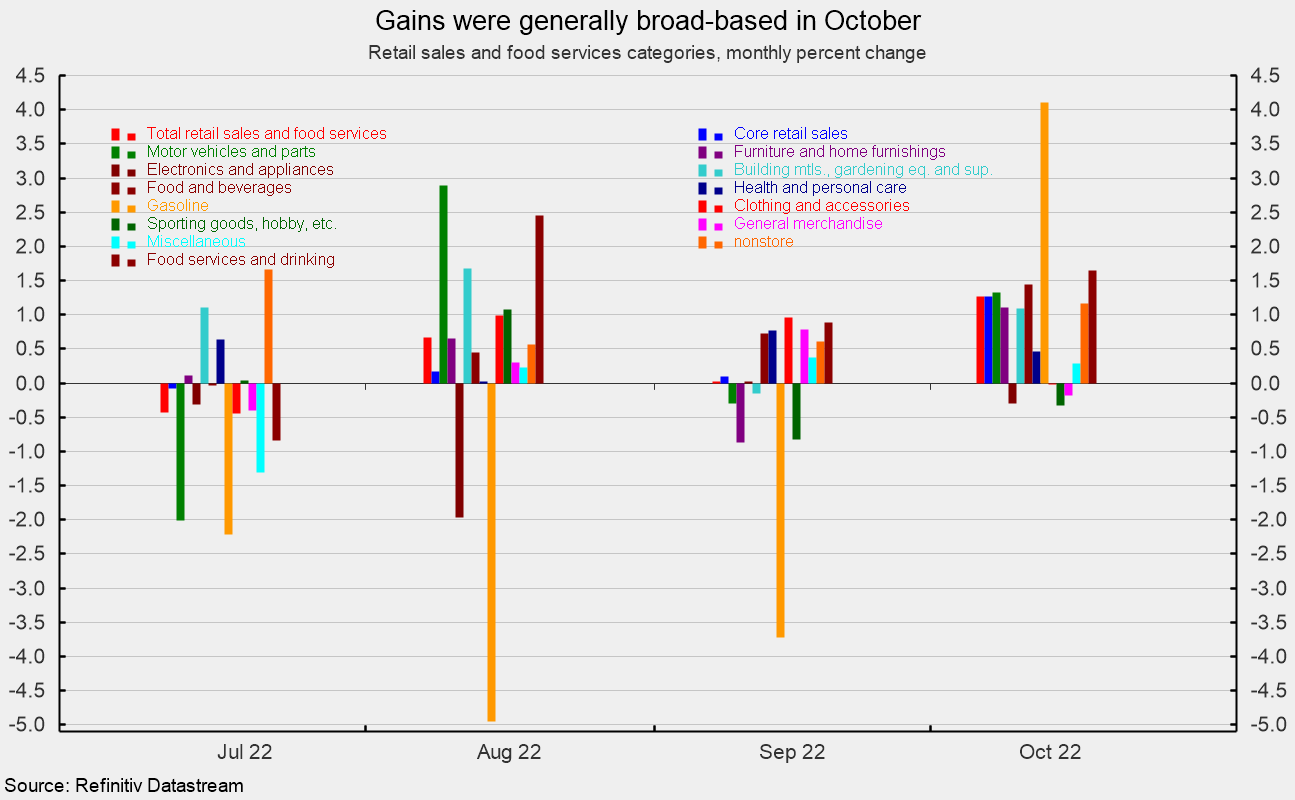

Categories were generally higher in nominal terms for the month, with nine up and four down in October (see fourth chart). The gains were led by gasoline spending with a 4.1 percent jump following a 3.7 percent drop in September. The average price for a gallon of gasoline was $4.13, up 3.5 percent from $3.99 in September, suggesting price changes more than accounted for most of the rise. Food services and drinking places (restaurants) rose 1.6 percent followed by food and beverage store sales (groceries) up 1.4 percent, motor vehicles and parts retailers, (1.3 percent), nonstore retailers (1.2 percent), furniture and home furnishings (1.1 percent), and building materials, gardening equipment and supplies (1.1 percent). Declines came in electronics and appliance stores (-0.3 percent), sporting goods, hobby, musical instruments, and book stores (-0.3 percent) and general merchandise stores (-0.2 percent).

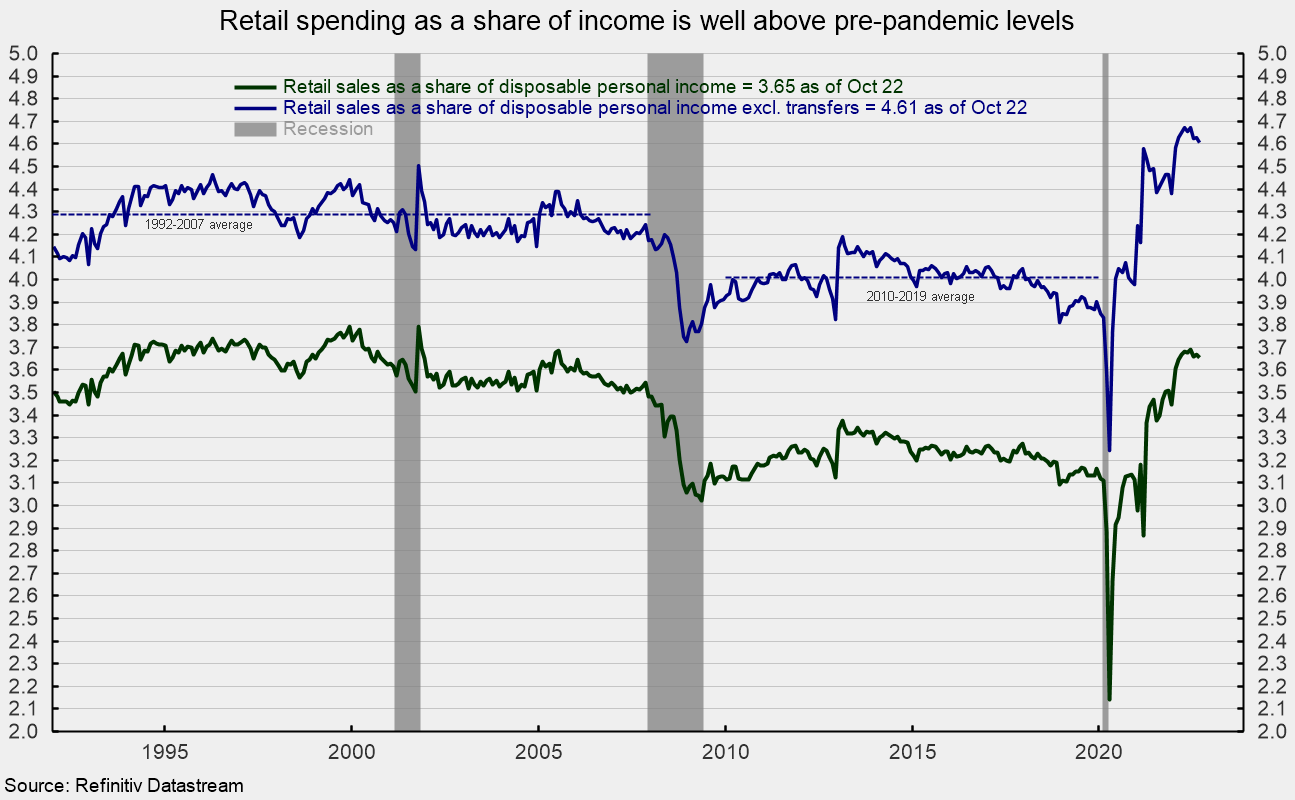

Overall, nominal total and core retail sales remain well above trend. However, rising prices are still providing a significant boost to the numbers. In real terms, total and core retail sales posted solid gains in October, but the trends are much weaker. Retail spending measured as a share of personal income remains well above the average shares seen in the 2010 through 2019 period and the 1992 through 2007 period (see fifth chart).

Sustained upward pressure on prices is likely affecting consumer attitudes and spending patterns. As more and more consumers feel the impact of inflation, real consumer spending may be under pressure. Furthermore, an aggressive Fed tightening cycle may lead to significant demand destruction. Both phenomena raise risks for the economic outlook. In addition, the fallout from the Russian invasion of Ukraine and waves of lockdowns in China remain threats to economic expansion. The outlook is highly uncertain. Caution is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.