Holiday Spending Outlook Upbeat

November is the second consecutive month of across-the-board 100 percent readings for our primary leading, primary roughly coincident, and primary lagging indicators. Our cyclical score of leading indicators, derived from a separate mathematical analysis, also increased from 88 in October to 91 in November. (See The Indicators at a Glance on page 2.)

Among the leading indicators, M1 money supply and our yield curve index hit new highs in November, suggesting financial conditions remain supportive of future economic growth.

Initial claims for state unemployment insurance were judged to have a favorable trend, meaning claims are continuing their slow downward trend and remain within the 300,000 to 350,000 range that is consistent with a healthy labor market.

The average workweek in manufacturing indicator was also judged to have a favorable trend, reflecting the lengthening workweek for manufacturing workers and suggests that factories are getting busier. Our index of common stock prices, which is adjusted for inflation, hit a new high for November, consistent with the performance of most of the non-inflation adjusted indexes followed in the press.

We appraised the trend in the change in consumer debt as neutral in the latest month as consumers continue to refrain from adding significant new debt. Following several years of debt reduction, consumer balance sheets are looking healthier. An end to debt reduction should free up income for consumption and would allow consumers to begin adding debt at some point in the future, potentially boosting spending down the road. For now, consumer debt growth remains broadly flat.

Among our primary roughly coincident indicators, nonagricultural employment registered a new high in November, confirming the positive readings from our labor-market-related leading indicators. Personal income less transfer payments was judged to have a positive trend supported by increasing jobs, wages, and a lengthening workweek. Gains in personal income should help support consumer spending and overall economic growth.

Consumers Poised to Buy

The holiday shopping season (November and December) accounts for about 20 percent of annual core retail sales (retail sales and restaurants excluding autos and gas). With Black Friday behind us, attention will surely be focused on the remaining shopping days and whether U.S. consumer spending will contribute to a strong fourth-quarter GDP gain.

Early estimates are providing conflicting indications. The National Retail Federation is projecting a 2.7 percent decline compared to last year, based on a survey of 4,464 consumers, while ShopperTrak estimated a 2.3 percent rise based on foot traffic measured by cameras in 60,000 stores nationwide combined with government and retailer data.

Our analysis suggests that growth in core retail sales is likely to be equal to or better than the 5.4 percent gain in 2011 and the 4.7 percent gain in 2012.

The key drivers of consumer spending include jobs, wages, income, debt and debt service, wealth, and confidence. A number of measures for these drivers are components of our statistical indicators of business-cycle changes. As mentioned above, among our leading indicators this month, AIER’s experts appraised initial claims for state unemployment insurance and the average workweek in manufacturing (both indicators of the job market), and the index of common stock prices (an important part of consumer wealth) as having favorable trends. We appraised the trend in consumer debt as neutral.

Nonagricultural employment and personal income less transfer payments, both parts of our roughly coincident indicators, were also judged to have favorable trends. Among our lagging indicators, we appraised the ratio of consumer debt to income as also having a favorable trend. Overall, our proprietary indicators would suggest a generally positive holiday shopping season.

In addition to relevant AIER indicators, we look at several other important measures that may give some guidance on the current shopping season. For each, we compare the latest data available prior to the start of the shopping season (usually October data) to the same point in 2011 and 2012.

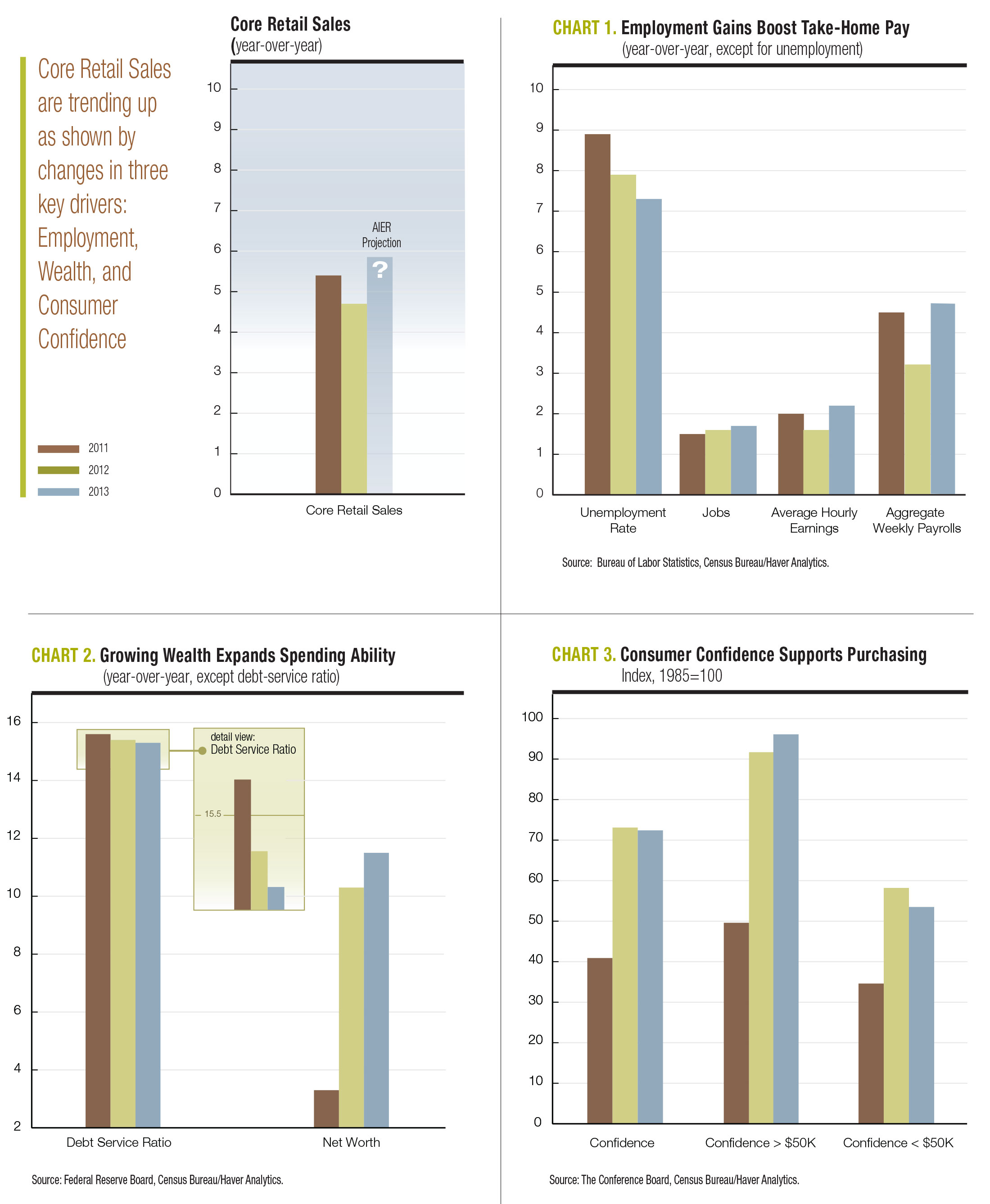

The unemployment rate has declined from a recession peak of 10 percent in 2009 to 7.3 percent in October 2013. While this level of unemployment is still too high, the important point for this year’s core retail sales growth is that the unemployment rate has declined over the past two years: from 8.9 percent in October 2011 to 7.9 percent in October 2012 to the 7.3 percent in October 2013.

The flipside to the declining unemployment rate is the gain in the job market. Since the end of the recession in 2009, payrolls have added back about 7.2 million of the 8.7 million jobs lost during the recession at a slow but steadily increasing rate. Over the last three years, payrolls added 1.9 million jobs in the 12 months through October 2011, a 1.5 percent rise compared to 2.1 million jobs for the year ending October 2012, or a 1.6 percent gain. For 2013, payrolls have added 2.3 million new jobs, a rise of 1.7 percent.

Wages, as measured by average hourly earnings, were up 2.2 percent for 2013, compared to 2 percent for the 12 months through October 2011 and 1.6 percent in for the comparable period in 2012. While these gains are slow by historical measures, when combined with growth in employment and a rise in hours worked, take-home pay has posted reasonable advances.

As measured by the aggregate weekly payrolls index, take-home pay rose 4.5 percent in 2011, 3.2 percent in 2012, and is up 4.7 percent through October 2013. Again, all these increases are mild by historical standards, but inflation is also quite low by historical standards implying that overall purchasing power has been increasing.

Taken together, these job and income indicators suggest core retail sales growth is likely to match or exceed the gains in 2011 and 2012. For each, the 2013 level has improved compared to the levels seen at the beginning of the prior two holiday shopping seasons (See Chart 1 on page 4).

There are a few other key metrics that are relevant to consumer shopping trends. First is debt service.

Consumers have made significant progress reducing debt service burdens over the past several years. Consumer debt service, as measured by the Federal Reserve’s Financial Obligations Ratio has declined sharply from its peak of 18.4 percent in 2007 to the current level of 15.3 percent as of the second quarter of 2013—and now is close to a 30-year low.

The financial obligations ratio is an estimate of the relationship of minimum required payments to disposable personal income. The required payments include mortgages and consumer debts plus automobile lease payments, rental payments on tenant-occupied property, homeowners’ insurance, and property tax payments. A lower debt service burden allows a greater share of disposable income to be used for spending.

Restructuring the liability side of the balance sheet is healthy for the economy in the long run and contributes to gains in overall household net worth—also an important driver of consumer spending. As consumers become wealthier, they tend to allocate a larger share of their income to spending.

For consumers, net worth has hit a new all-time high of $74.8 trillion as of the second quarter of 2013, having posted year-to-year gains. While reducing debt has contributed to increases in net worth, rising asset prices has also been a major factor. In general, stock price indexes in the U.S. (as well as AIER’s stock price index) are hitting record highs, helping push the value of consumer financial assets up. At the same time, housing prices continue to regain ground, helping the value of consumer’s real assets.

Like the indicators for jobs and income, the measures of debt service and household net worth are showing improvements compared to their levels at the start of the prior two holiday shopping seasons. This supports the expectation of comparable or slightly better gains this year in core retail spending (See Chart 2 on page 4).

With the labor market making slow but steady progress, housing prices recovering, and stock prices moving to new highs, consumer confidence in the U.S. has been on an uptrend over the past few years. Despite declines in September and October, overall consumer confidence as measured by The Conference Board stood at 72.4 in October 2013, down slightly from 73.1 in October 2012, but up sharply from 40.9 in October 2011.

The overall consumer confidence numbers tell a generally supportive story. If we look at confidence by income group, the data become even more interesting. Confidence among consumers earning less than $50,000 has trended higher since the end of the recession, but it has been far less robust than for consumers earning more than $50,000. Part of the reason for the divergence is the greater exposure to rising asset prices, particularly equities, for the higher income group as well as a somewhat more favorable recovery in higher-paying jobs.

For the two cohorts, consumer confidence as of October 2013 is higher than the levels seen in October 2011, a positive for the spending outlook. Interestingly, when compared to 2012, confidence for the lower-income group has declined slightly while confidence for the upper-income group still shows an increase (See Chart 3 on page 4). Given that the upper income group accounts for about 69 percent of total consumer spending, the relatively stronger reading for confidence among the upper earners is also a positive for the spending outlook.

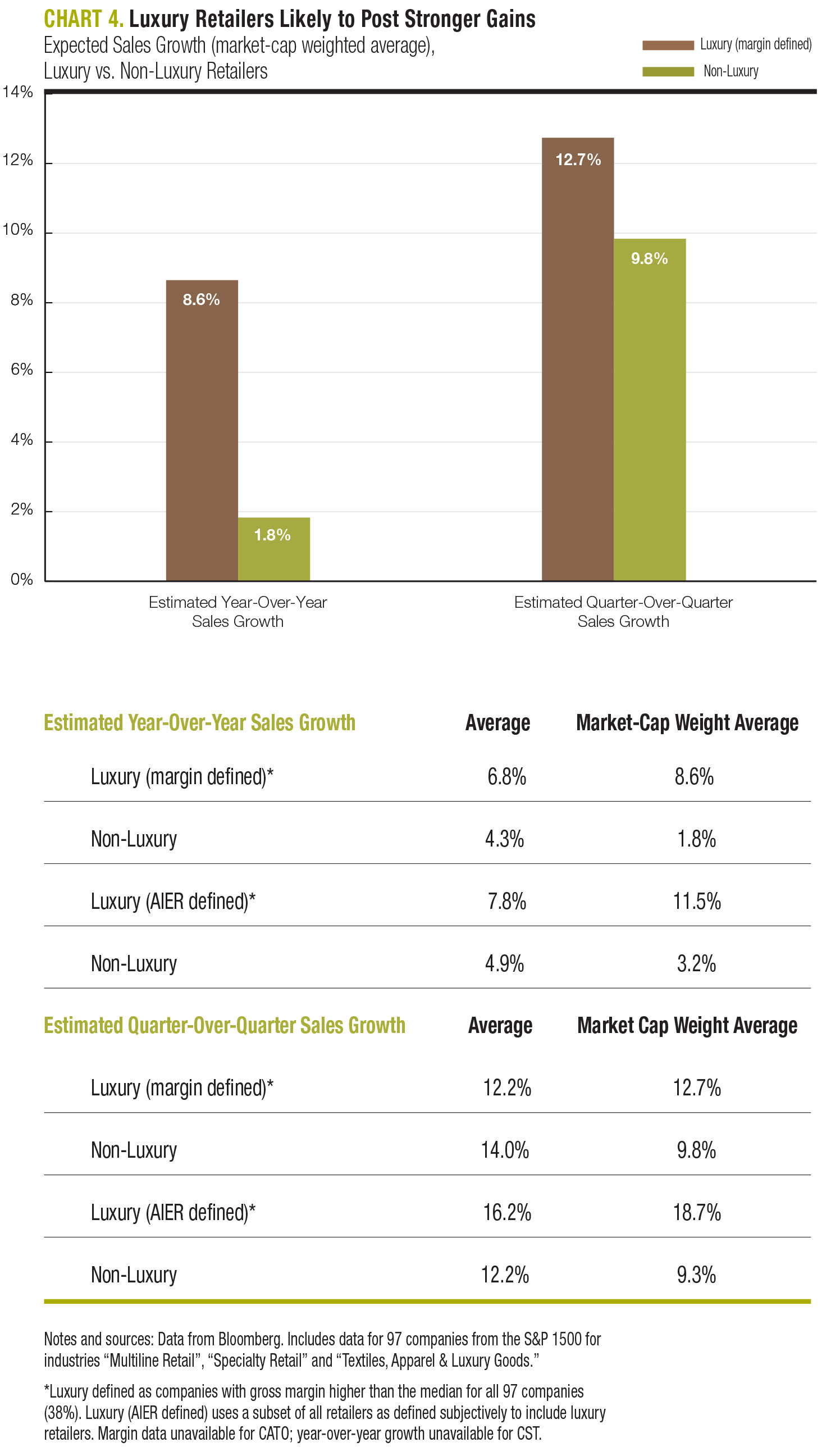

It’s not surprising to see the gap in confidence between the upper-and lower-income groups reflected in the outlook for retailers. We use gross profit margins as a proxy for identifying retailers of luxury goods who typically sell higher-margin goods to higher-income groups compared to lower-margin retailers who tend to sell to lower-income groups.

According to data from Bloomberg, expectations for sales growth for the fourth quarter are higher for higher-margin retailers than for lower-margin retailers. Consensus estimates by equity analysts imply an expectation of 8.6 percent year-over-year growth for luxury retailers versus just a 1.8 percent gain for non-luxury retailers (See Chart 4 and the table on page 5).

Given the steady improvement in key drivers of consumer spending, we expect the 2013 holiday spending season to post gains about equal to or slightly better than those posted in the past two years. This is consistent with the outlook suggested by our leading and coincident indicators for continued moderate economic growth overall.

Moreover, our analysis suggests that spending is likely to be supported by both upper-income and lower-income groups, though the upper-income groups are likely to provide a larger share of the overall growth.

[pdf-embedder url=”https://www.aier.org/wp-content/uploads/2014/01/BCC20131210.pdf“]Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.