April Business Conditions Monthly

The AIER Business-Cycle Conditions Leaders index rose to 83 in March, the highest level in two and a half years (Chart 1). The Coinciders index rose to a perfect 100, the highest level since September 2015, while the Laggers index pulled back to 83 from 92 in the prior month.

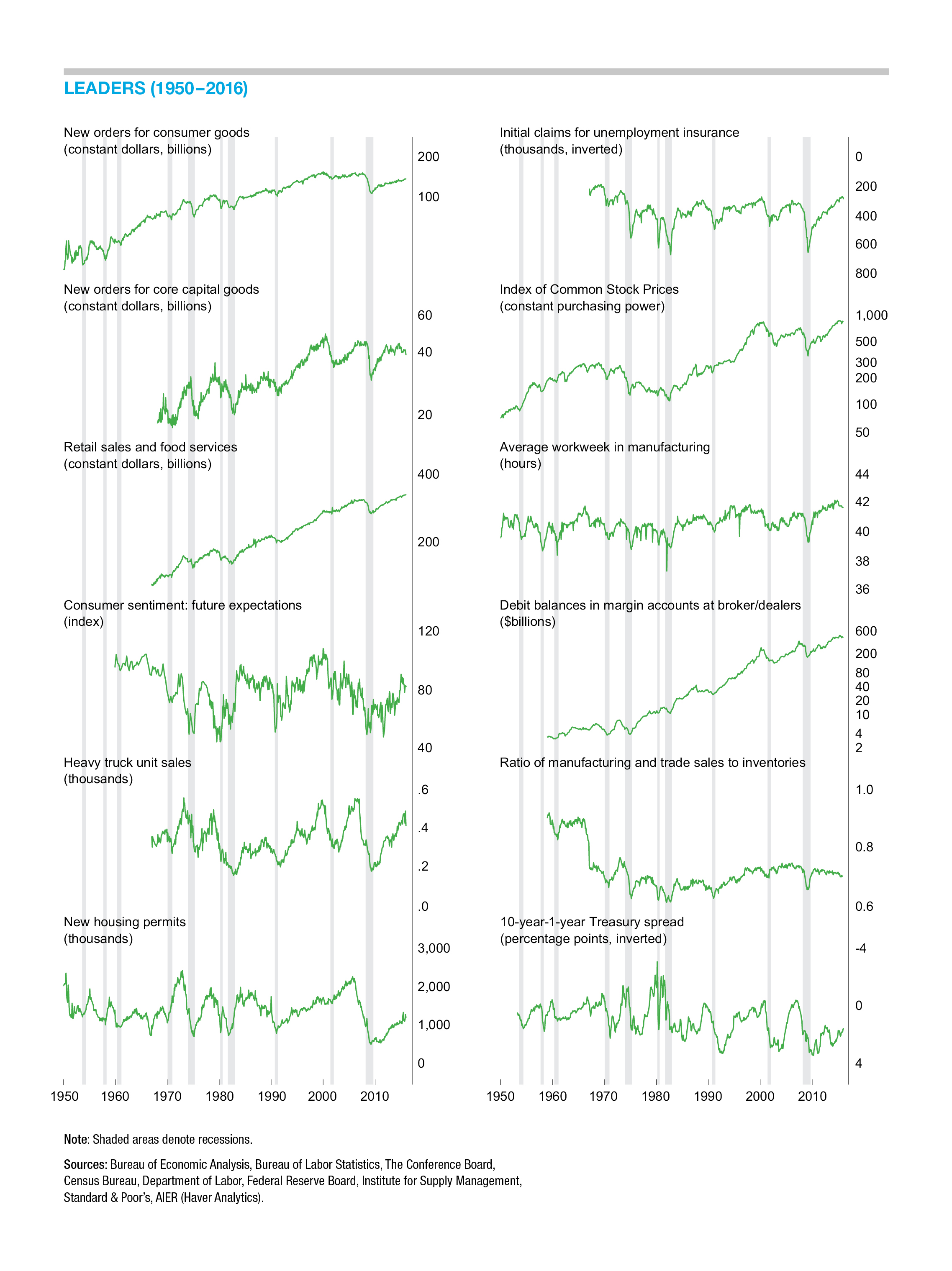

Nine of the twelve Leaders are now expanding compared to eight in the previous month. The indicator for average workweek in manufacturing turned from a flat trend to an increasing trend in the latest month, reflecting better conditions in the sector. Initial claims for unemployment insurance, the other labor market indicator among the Leaders, remains in a favorable trend. Initial claims is one of our Leaders with an inverse relationship with the business cycle. Lower initial claims for unemployment insurance is headed in a favorable direction. The current trends for these two Leaders are consistent with the strong labor market conditions that have been slowly developing over the past few years. Both indicators do have natural limits on their performance. The average workweek in manufacturing can only increase so far before plateauing. Likewise, initial claims can only drop so far before bottoming. At some point, these Leaders may move to a flat trend, but serious concern should only arise as these two Leaders change to unfavorable trends.

Two Leaders are currently flat: real new orders for consumer goods, and unit sales of heavy trucks. Real new orders for consumer goods turned from an upward trend to a flat trend in July 2016, turned negative the following month, and stayed in a downward trend until December 2016. The current four-month run in a flat trend seems likely to break to the positive side in coming months given the strong labor market conditions. An improvement to a positive trend would confirm the favorable results for the other two consumer-related Leaders, real retail sales and food service spending and the University of Michigan Index of Consumer Expectations.

Unit sales of heavy trucks just improved to a flat trend in March after several months in a downward trend. The other capital-spending-related Leader, real new orders for core capital goods, had shown weakness for most of the 2012 through 2015 period but turned to a positive trend in January 2017. Capital spending in the United States has been weak over the past several quarters, partially due to the collapse in energy prices in mid-2014. As energy prices rebound, investment in energy-related industries has bottomed and looks to be turning higher. Stronger economic data and anticipation of infrastructure spending in the future have added to business confidence and may support faster growth in business investment.

Overall, the recent performance of our Leaders is reassuring, pointing to continuing economic expansion in the months ahead, with a low risk of recession. Positive signs for the current expansion are reinforced by favorable results from our Coinciders.

Our Coinciders index registered a perfect 100 as all six of the indicators are now expanding. March is the first reading of 100 since September 2015. The employment-to-population ratio and industrial production had been trending flat in February, but both returned to positive trends in March. Despite the recent improvement, the ratio stands at 60.0 percent as of February 2017, well below the peak of 64.7 percent in 2000.

Industrial production posted its third month of an increasing trend in March following 23 months of weakness. Most of that weakness was a result of a collapse in mining output related to the drop in crude oil prices. Manufacturing output, the majority of total industrial production, has had slow but steady gains since the end of the recession. The perfect 100 reading from the Coinciders index gives definitive proof of the improving economic conditions.

Our Laggers posted a slight decline in March, falling to 83 from 92 in February. Four indicators are currently trending higher while two are flat, including real commercial and industrial loans, which had been trending higher in February. None of the Laggers indicators are moving lower.

Green shoots for housing

The housing market continues to recover from the boom-and-bust cycle of the late 2000s. Residential investment—new single-family and multifamily home construction plus existing home renovations—has been a net contributor to real gross domestic product for most of the past three years, though the second and third quarters of 2016 were exceptions.

After the Great Recession, multifamily construction led the recovery as starts and permits reached their prerecession range by the end of 2012. More recently, multifamily starts and permits have flattened out at about a 400,000-unit pace, above the average during the 1990s and 2000s but still below peak rates from the 1960s through 1980s. Despite the relatively high level of new construction, the vacancy rate for multifamily housing units has declined to the 4.5 to 5.5 percent range over the past few years. The inventory of existing multifamily units for sale also remains low by historical measures, with just 4.2 months of supply in February.

The market for single-family housing has been a bit slower to recover. Single-family starts and permits have been trending higher since the end of the Great Recession, but the level of activity remains below the long-term average. Single-family starts registered an 872,000 annual pace in February, up from a low of 353,000 in 2009 but well below the 1.1 million average from 1959 through 2006. Still, the continued slow gains have been a net positive for the economy.

One benefit of the slow pace of recovery is that the single-family market has remained tight, and that has helped support home prices. There was 5.4 months’ supply of new single-family homes for sale in February. That is below the long-term average but still above the 3.8 months’ supply of existing single-family homes. The Case Shiller home price index rose 5.7 percent from a year ago in January, ahead of the 5.0 percent average since 1976.

With the unemployment rate low, continuing jobs creation, a large number of open jobs, rising incomes, and high consumer confidence, housing activity is likely to be healthy during the 2017 selling season. The two potential headwinds are the possibility of higher rates (though the Fed isn’t likely to raise rates again until later this year) and the availability of mortgage credit. Based on surveys of commercial-bank-loan officers, mortgage lending standards are neither excessively tight nor dangerously loose. Reasonable credit availability will be critical to sustaining housing activity, but poor lending can lead to bigger troubles down the road. Conditions are favorable for housing activity—sales and construction—especially for the single-family segment, to perform well over the next several months.

Energy and housing driving consumer prices higher

The Federal Reserve raised the target for the federal funds rate by 25 basis points on March 15. That was just the third rate increase since December 2015. Fed members were in favor of a rate increase because they believe that the economy has moved closer to the dual-mandate targets of full employment and price stability. Fed members view full employment as an unemployment rate between 4.5 percent and 5.0 percent. The current unemployment rate is 4.7 percent. Other labor indicators reflect a generally healthy jobs market as well. Job creation continues at a healthy pace, with payrolls adding 235,000 new employees in February and an average of 209,000 over the past three months. The number of job openings remains near multidecade highs, more employees are quitting for better jobs, the participation rate has increased, and hourly earnings growth is accelerating.

The second part of the dual mandate, stable prices, is defined as an average growth rate of 2.0 percent in the Personal Consumption Expenditures (PCE) price index over the medium term. The PCE price index has increased 1.9 percent over the twelve months through January 2017, up from a pace of 0.9 percent in July 2016. However, much of the increase has come from a rebound in energy prices. The PCE index excluding energy is up 1.5 percent over the past 12 months, about where it has been for the past five years.

Among the other components of the PCE price index, housing services, particularly imputed rent of owner-occupied housing, has been a major component of PCE index increases. Imputed rent has been increasing above the Fed’s 2.0 percent overall target for the past five years and is up 3.6 percent over the past year through January 2017. This category accounts for about 10 percent of real consumer spending. Unlike most of the information in the PCE spending and PCE price indexes, there is no actual underlying transaction behind this category. It is an accounting entry best understood as what a homeowner would pay themselves to rent their home.

In general, price pressures continue to come from services, while goods prices are about flat. Services prices are up 2.4 percent over the past year, while goods prices are up just 0.8 percent. Within goods, durable-goods prices are down 2.4 percent, while nondurable goods prices are up 2.5 percent, driven by a 19.2 percent jump in energy goods.

Over the past 20 years, M2 money supply has grown at an annual average pace of 6.4 percent per year. During that time, the PCE price index has increased at a 2.0 percent annual rate. As of February 2017, M2 money increased 6.4 percent over the prior year and the PCE price index has risen 1.9 percent. Though price increases have been low, concern over the future path of prices is warranted. The Fed is removing monetary accommodation, but at a slow pace so as not to put the current economic expansion at risk. However, the Fed’s balance sheet remains bloated, bank reserves exceed $2.3 trillion, and the monetary base tops $3.7 trillion. On a positive note, bank reserves are down about 8 percent from a year ago, and the monetary base has shrunk by 3.3 percent. While waiting for a surge in prices due to Fed policies has been like waiting for Godot, vigilance is required, especially with stronger economic growth.

Inflation protection

Prices increases remain tame, for now. The potential for accelerating price increases exists. Historically, certain assets have been more successful at protecting wealth from inflation. Treasury Inflation Protected Securities (TIPS) are government-issued debt securities that offer protection against inflation. These securities adjust coupon and principal payments for changes in the Consumer Price Index. However, these securities can also be impacted if prices fall.

Hard assets such as commodities and real estate help protect against inflation. The prices of these assets tend to rise along with the general price level, offsetting the declining value of the dollar. Gold is often the preferred hard asset as it is a very liquid global commodity that is easily purchased and held by investors. It has the added benefit of being a safe haven in times of political and financial distress. Over the past 20 years, the price of gold increased dramatically. From a low of around $250 per ounce in 2001, gold prices soared, along with most other commodities, hitting a peak of about $1,900 per ounce in 2011. However, since 2011, gold has fallen to about $1,250 an ounce currently, a decline of about 34 percent. But even at $1,250 an ounce today, gold is up fivefold from the low in 2001.

Equities also offer some hedge against inflation as prices tend to rise with the general price level. However, the value of equities can be held back by rising interest rates typically associated with accelerating inflation. Equities can also be hurt by weakening demand as investors reallocate to equities in other countries.

Traditional fixed income securities typically offer the least protection against inflation. Since both the principal and coupon payments are fixed, these instruments are most impacted by accelerating price increases.

[pdf-embedder url=”https://www.aier.org/wp-content/uploads/2017/04/BCM_April2017.pdf“]Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.