Trouble Ahead: Unfunded Liabilities in State Pension Funds

Since the Great Recession, large federal budget deficits and a record level of government debt have dominated the headlines. But municipal and state finances have also come under stress in recent years. On the municipal side, Detroit declared bankruptcy and restructured public pensions. In Dallas, the police and firefighters’ pension fund is broke. Stockton and San Bernardino rank as two of the largest municipal bankruptcies in U.S. history.

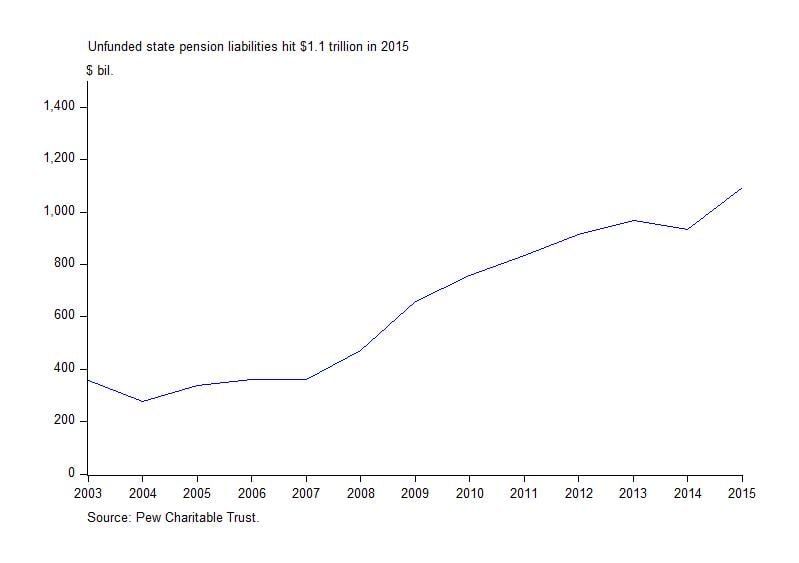

At the state level, public pension funds bear significant stress. The gap between the benefits promised to workers and state pension fund assets was $1.1 trillion in 2015: a 17 percent increase from 2014. The gap is known as the net state pension fund liability. State pension funds were well-funded until the early 2000s, but in 2001, the net state pension fund liability began to increase.

The net liability grew between 2014 and 2015 because of low investment returns: the median return on state pension fund investments was 3.6 percent in 2015. The predicted long-run return was nearly double the actual return. On average, state pension funds had assumed a long-run investment return of 7.6 percent. Assumed long-run returns have been difficult to calculate because actual returns have been volatile.

They have been volatile because funds have moved into riskier assets. Since the early 1990s, state pension funds have moved from low-risk investments, like AAA bonds, to riskier investments such as equities. Since 1990, the share of state pension fund assets invested in equities has increased from 40 to 70 percent. The result has been volatile returns for state pension funds, ranging from low single digits to as high as 21 percent in 2011.

According to a report by the Pew Research Center, Alaska, Illinois, and Mississippi have the most unfunded pension liabilities as a share of personal income. Unfunded pension liabilities in Alaska were 23.7 percent of income, while liabilities in Illinois were 16.8 percent of income. Nevada has also seen a large increase in unfunded pension liabilities, mostly because of optimistic assumptions about investment returns. In comparison, the national average was close to 7 percent and states such as North Carolina, Wisconsin, and South Dakota have pension liabilities covered.

A widening gap between state pension fund liabilities and assets poses serious risks. Unfunded pension liabilities likely mean higher contributions from state governments and lower benefits. Prospects for larger contributions from state governments are not auspicious. Last year, state governments’ contributions fell short by $8 billion. Higher taxes are politically difficult.

Are there any solutions? Some municipalities, like Philadelphia, have offered retirees a buyout. New York State has reduced pensions for new employees. Without reforms, the pension crisis will not just be felt by the public sector. Unfunded liabilities will have an impact across the economy. Reduced benefits will curb consumption, while higher taxes will push consumers and businesses out of the state.