This Is Not QE4, Yet

When the plumbing clogs up, no matter how impressive the building, it’s worth keeping an eye on.

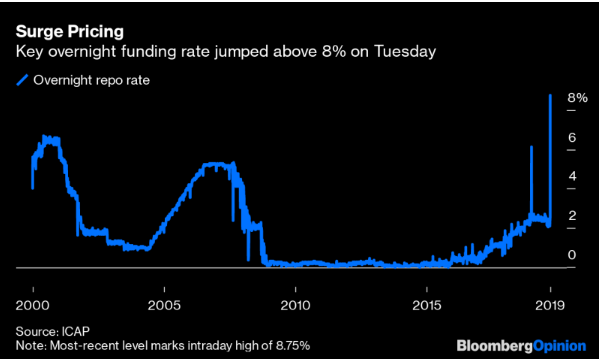

The overnight repurchase (repo) market serves as the plumbing to keep liquidity flowing through the financial system. So when the news broke that the overnight borrowing rate surged to nearly 10%, causing the Fed to conduct back-to-back injections of liquidity for the first time in over a decade, it created a whirlwind of analysis and commentary among TV pundits.

With all of this chatter, one might think there is cause for panic. Actually, there is not.

Why is this repo market so important, if the Fed had not stepped into it for over a decade? What were the real drivers of the tightening of the market and spike in overnight rates?

What is the repo market, and why not to panic

Repo operations (overnight repurchase agreements) began with the establishment of the Federal Reserve in 1917, but it was in the immediate wake of the Vietnam War that the modern repo market was born. When bouts of high inflation struck the United States during the early 1970s and again in the late 1970s and early 1980s, many banks, large corporations, and even municipal governments chose to place their idle cash – until then held within the banking system, in amounts often exceeding standard depository insurance – into short-term government securities (U.S. Treasury bills and notes) to take advantage of rising short-term rates alongside default guarantees. During the same time period (post-1974) the U.S. became a debtor nation and a previously illiquid marketplace for U.S. government debt expanded considerably.

Funding in short-term/overnight markets via repo transactions was and remains a market response to the simultaneously unmet requirements of both large institutional cash pools and broker-dealers/hedge funds possessing large inventories of securities. Moving the trillions of dollars outside of the banking system into the conventional banking system is simply not an option given the associated costs, administrative requirements, and loss of flexibility that such a move would entail.

What were some of the real drivers?

The sky isn’t falling on the U.S. economy, despite some of the comments among the talking heads; the tighter overnight market this week can be explained by factors that anyone who watches the markets for a living should have seen coming.

A large number of U.S. corporations submitted quarterly tax payments this week, due on September 16th, which by no coincidence was the first date the overnight repo market tightened. Corporations needed liquidity (cash) to make these estimated payments, drawing liquidity out of the market in the form of withdrawals from money market funds that might have otherwise provided the cash side of repo exchanges.

Increases in Treasury issuance, due to the increasing budget deficit, has soaked up cash and left less to lubricate the overnight repo market. Additionally, with the Fed monetizing some of these Treasury issuances, and directly owning trillions in these securities, the amount of available cash was decreased further.

Adding a bit of geopolitical speculation to the mix, it is also possible that the Saudis — normally playing a large role in the cash side of the repo exchange — have been distracted due to the drone attacks on Aramco facilities over this past weekend. The attack took offline nearly 5.7 million barrels per day of production, or over 50% of the kingdom’s daily output. The rapid restoration of production and refining is indicative of how high a priority this has been, and reinforces the idea that other items may have been put on the back burner this week.

Markets were working. Whether in the realm of gasoline after a hurricane or in a market for borrowed money, scarcity pushed prices (in this case, short term interest rates) up, which is in turn what attracted additional supply. It is true that some firms may have been inconvenienced (or, indeed, handicapped) if insufficient liquidity had not responded to the briefly 8 – 10% repo rates, but the Fed’s action underscores the interventionist core of the money market.

This is not a panic

The standard barometer of banking distress, the TED spread (calculated by taking the difference between the 3-month US Treasury Rate and the LIBOR rate), has essentially not budged during the last week, sitting as it is near five-year lows. It measures the willingness of banks to lend to one another in the overnight market: a spike in that rate, therefore, indicates a growing reluctance (a need for greater compensation to offset real or perceived risk) among banks to lend to other banks. At 22 basis points (bps) today, it sits at less than half the long-term average (57 bps); by comparison, during the depths of the financial crisis in the fall of 2008, the TED spread spiked by a factor of 20 times to nearly 500 bps.

The events of the last few days are noteworthy but at this point are more of a warning about the financing implications of rapidly ballooning deficits and bad timing rather than of an imminent financial crisis. In short, the Fed’s repo operations are worth watching, but are not currently pointing toward wide economic panic.

Peter C. Earle

Peter C. Earle, Ph.D, is a Senior Research Fellow who joined AIER in 2018. He holds a Ph.D in Economics from l’Universite d’Angers, an MA in Applied Economics from American University, an MBA (Finance), and a BS in Engineering from the United States Military Academy at West Point.

Prior to joining AIER, Dr. Earle spent over 20 years as a trader and analyst at a number of securities firms and hedge funds in the New York metropolitan area as well as engaging in extensive consulting within the cryptocurrency and gaming sectors. His research focuses on financial markets, monetary policy, macroeconomic forecasting, and problems in economic measurement. He has been quoted by the Wall Street Journal, the Financial Times, Barron’s, Bloomberg, Reuters, CNBC, Grant’s Interest Rate Observer, NPR, and in numerous other media outlets and publications.

Sean Stein Smith

Sean Stein Smith was a Visiting Research Fellow at the American Institute for Economic Research, focusing on blockchain, cryptoassets, and the economic impact of these technologies. He is an Assistant Professor at the City University of New York (Lehman College), serves on the Advisory Board of Wall Street Blockchain Alliance, where he also chairs the Accounting Working Group, and chairs the Emerging Technology Interest Group of the New Jersey Society of CPAs. His research has been quoted in dozens of scholarly and practitioner publications, and he is a regular speaker at accounting and technology conferences. Follow him on Twitter.