Trade Wars and Monetary Policy

President Trump’s trade war is in full tilt, much to the dismay of many economists and the detriment of producers and consumers across the globe. If the recent responses of nations like Canada and China are any indication, tensions will continue to escalate.

How should the Fed respond to the rising prices that will inevitably result from a trade war? And what can it do to ensure the real harm inflicted by the trade war doesn’t snowball into a general economic downturn?

Most economists in the monetary-disequilibrium tradition favor rules over discretion in monetary policy. When it comes to selecting the rule, they tend to argue that central banks should restrict their focus to targeting nominal rather than real variables. After all, central banks’ monopoly over the supply of bank reserves, a nominal variable, gives them much more direct influence over other nominal variables like inflation or nominal GDP in the long run than real variables like real GDP and unemployment. For this reason, many central banks over the past few decades have adopted some version of inflation targeting.

But not all versions of inflation targeting are equally equipped to deal with real shocks like trade wars. Economists who favor rules also tend to argue that the best type of monetary rule is one central banks can adhere to at all times, both good and bad. Which version of inflation targeting does the best job of maintaining monetary equilibrium and keeping output at its natural level through thick and thin?

Choosing the Right Target

Before we analyze what rule the Fed should use to guide monetary policy during a trade war, it’s worth recapping some of the debate over inflation targeting since it remains the most popular rule today.

Generally speaking, there are two approaches to inflation targeting. The first is to set a strict inflation target at some predetermined rate (say, 2 percent). This “strict” approach has the benefit of making the value of the monetary unit stable and predictable over time. But the benefit comes at a considerable cost. To wit, under a strict approach any deviation from the inflation target is ipso facto undesirable. This is true even when the deviation can be traced to changes on the real side of the economy, like when an oil shock causes the overall price level to rise or a technological advance leads to a dramatic reduction in prices of certain goods.

A strict inflation target would thus require central banks to respond to negative or positive supply shocks by either cutting the money supply (as in the case of a negative oil shock) or increasing it (as in the case of productivity-induced deflation) to achieve their rigid inflation target. Unfortunately, any attempt by central banks to offset these real-side-induced price changes would distort the money and loanable-funds markets and cause output to fluctuate more wildly. It would push the economy beyond its sustainable production possibility frontier in the case of a positive supply shock, or, in the case of a negative supply shock, exacerbate a real business cycle.

The limitations of strict inflation targeting have led many economists to instead support a “flexible” inflation target. As the name suggests, proponents of flexible targeting argue that central bankers needn’t panic if inflation rates vary so long as the swings stem from changes on the real side of the economy. Rather than increasing the money supply every time inflation falls, for instance, central banks should welcome below-target inflation, and even deflation in some cases, when it stems from positive supply shocks like firms’ discovering more efficient production methods or technological innovations like the 3D printer. They should likewise abstain from contracting the money supply to prevent any rise in inflation that results from negative supply shocks like, say, an oil shock or a natural disaster that destroys dozens of factories. In summary, in a world where productivity is constantly in flux, a flexible inflation target would do a better job of keeping output and employment at their natural levels than a strict inflation target.

All that said, is inflation the ideal nominal variable for central banks to target? One rule that readers of this blog are likely familiar with that is wholly consistent with both focusing the Fed on nominal variables and allowing for a flexible path for inflation is an NGDP-targeting rule. The reason an NGDP target is superior to an inflation target both in theory and practice is fairly straightforward. By maintaining a stable path for nominal spending in the economy (however measured), central banks stabilize the economy’s aggregate demand. And since a productivity norm is inherently baked into the cake of a nominal-spending target, fluctuations in real output would be limited to only those induced by changes in real, supply-side factors.

Many economists (myself included) have come out in recent years in favor of a nominal-spending target along the lines proposed by Scott Sumner and dozens of monetary economists throughout history precisely because it would minimize fluctuations in real output and maintain monetary equilibrium. It would therefore do a better job of preventing changes in the money supply from exerting any undue influence over prices or being an independent cause of mischief in the economy.

Trade Wars, Negative Shocks, and NGDP Targeting

What exactly does understanding the proper monetary response to productivity shocks have to do with why NGDP targeting is more desirable than inflation targeting in an era of trade wars?

For all practical purposes, the economic effects of expanding trade with foreigners are akin to discovering a more efficient technology or production method. Society becomes richer when individuals and firms specialize in what they can produce at the lowest opportunity cost, then trade with others who do the same. Trade also makes us richer by opening up foreign capital markets so that firms and workers can access financial and physical capital that will enable them to produce more output. Trade helps raise factor productivity and lower output prices. Recalling our earlier discussion, the increased productivity made possible by expanding our trading network can be thought of as a special case of a positive supply shock.

But a trade war that shrunk the volume of international trade would represent a negative shock. Factor productivity declines when firms’ ability to access foreign capital is restricted. Their costs of production also rise as they are forced to pay higher prices for foreign-made inputs. These higher per-unit costs are ultimately passed along to customers in the form of higher output prices. Producers are forced to scale back production and lay off workers in response to their higher costs of production and the fall in foreign demand. Workers see their real wages fall because restricting access to foreign capital and global supply chains reduces their productivity.

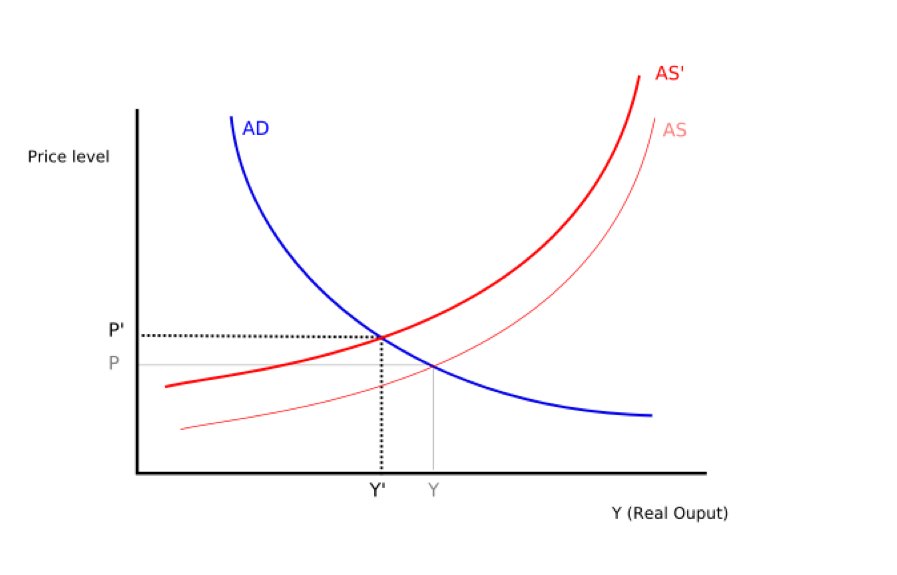

How would the Fed respond to such a negative shock under an NGDP-targeting regime? It would do whatever is necessary to stabilize the total flow of nominal spending in the economy, or aggregate demand. In the aggregate supply (AS) and aggregate demand (AD) framework, the Fed would simply keep the AD curve stable as the AS curve shifts inward following the outbreak of the trade war (figure 1). The economy would move up its unchanged AD curve to its new equilibrium, at which it intersects the new AS′curve. The overall price level (P) would rise; real output (Y) would fall. In effect, the Fed would respond to a trade war just as it would to a hurricane that destroys dozens of factories, an oil shock that affects firms’ costs of production, or any other negative productivity shock. This would enable it to minimize the negative effect of the trade war on real output without pushing the economy either inside or beyond its sustainable production possibilities frontier.

Figure 1. The Response of an NGDP Targeting Regime to a Negative Supply Shock

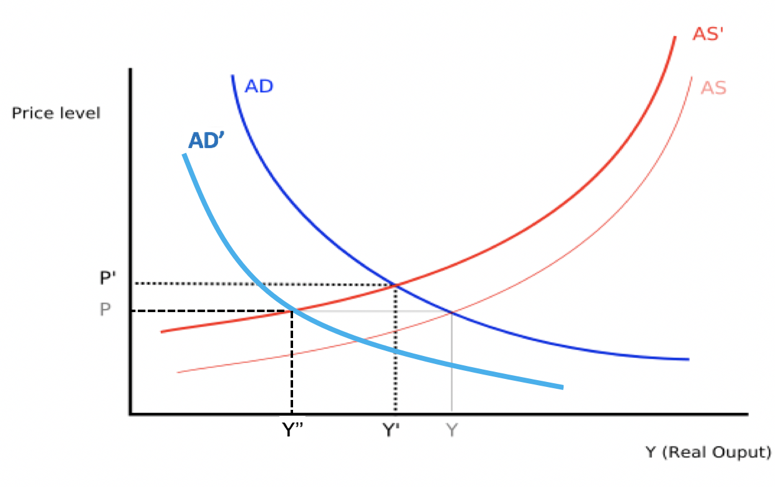

In contrast, how would an inflation-targeting Fed respond to a trade war? It would be forced to engage in contractionary policy to counteract the resulting rise in prices in order to keep inflation near its target. Unfortunately, as noted earlier, this policy response would intensify the already-detrimental impact of the trade restrictions on real output, raising unemployment and deepening the economic downturn. In the AS-AD framework, the Fed would have to actively contract the money supply to shift the AD curve in by enough to keep inflation at its desired rate (figure 2). The goal of keeping inflation stable therefore comes at the cost of greater output volatility, with the new equilibrium level of Y, Y′′, being even lower than Y′.

Figure 2. The Response of an Inflation Targeting Regime to a Negative Supply Shock

Just how much damage might a trade war inflict on our economy? Consider what happened in a previous trade war — namely, the one sparked by the passage of the notorious Smoot-Hawley tariffin 1930. Although Smoot-Hawley didn’t cause the Great Depression, it certainly contributed to it and the precipitous fall in international trade. Irwin (2006) estimates that “nearly a quarter of the observed 40% decline in imports” can be attributed to Smoot-Hawley. Bond et al. (2013) further estimate that “tariff protection reduced [total factor productivity] by 1.2%.” If Trump’s trade war were to escalate in similar fashion, it would translate into losses of tens of billions of dollars and thousands of jobs — not enough to amount to a replay of the Great Depression, but clearly significant harm.

Conclusion: Trade War, What Is It Good for?

The most important takeaway is that if we are stuck in a suboptimal world where tariffs and trade wars are here to stay, an NGDP-targeting regime would do a better job of minimizing fluctuations in real output than an inflation-targeting regime. In both cases, real output would fall as a result of the contraction in international trade. But in the case of NGDP targeting, that decline would be smaller, and monetary equilibrium would be maintained.

Thankfully, President Trump has assured us that “trade wars are good, and easy to win.” If depressed international activity is the president’s idea of winning, Americans might get sick of winning. But at least if the Fed adopts a nominal spending target, Americans might not get as sick.

Scott A. Burns

Scott A. Burns is an assistant professor of economics at Southeastern Louisiana University. His research focuses on financial innovation in the developing world, including the mobile money revolution that has taken place in Sub-Saharan Africa. He has published scholarly articles in Constitutional Political Economy, Independent Review, and the Journal of Private Enterprise.

Burns earned his M.A. and Ph.D. in Economics from George Mason University and his B.A. in Economics from Louisiana State University.