Evidence that Trade Wars Are Dragging the Economy Down

I had been listening to Donald Trump pledge a return to protectionism for many years, long before his implausible presidential victory. Most Republican lawmakers and voters either didn’t understand what that would mean or figured he couldn’t possibly be serious about this. After all, who doesn’t understand at this late date in human experience that national autarky is a sure loser for any country? If Trump doesn’t get this, then markets will take care of the problem. He loves a rising stock market, so surely economic reality will cause him to change course.

This last point was my one sliver of hope. Markets would fall and Trump would reverse course. Surely. It’s obvious that financial markets have been punishing this course since it all began in early 2018. My anecdotal observation saw it happening in real time. Trump would tweet and the markets would head south. A deal would seem to be in the offing and markets would grind their way back.

It’s been this way for a year and a half. The end result is that the rising markets that Trump used to trumpet are no more. Both the Dow Jones Industrial Average and the S&P 500 are at the same level they were 18 months ago, thus reversing the course of a decade of increases. How long must this experiment go on before Trump eats humble pie?

Financials are a sign but a superficial one compared with other trends of underlying weakness: consumer spending, business investment, foreign investment, and private-sector job creation. They are all weakening in unison. This is where matters get serious.

After daily warnings in the Wall Street Journal, and unrelenting commentary from the American Institute for Economic Research, one would think that the Trump administration would get the message. Still, the administration barrels ahead, raising tariff after tariff, even as the economy weakens further.

One theory is that the trade war is nothing but a pretext for Trump to do what he wanted to do from the beginning, which is to isolate the American economy from the rest of the world so that he can run the country like his own big firm. Even then, one would suppose that flat financials plus recessionary pressure would amount to a wakeup call – unless he is so confident that his political rivals are so lame that his reelection is guaranteed.

But notice that the administration always has another scapegoat besides the trade war. It’s the Fed. It’s tight money. It’s too-high interest rates. It’s the too-strong dollar. At one point, Trump even tweeted that the real problem is American businesses themselves, which, he said, are “badly run” and “weak.” Too weak to withstand the piece-meal pillaging of the Trump administration’s own protectionism!

What’s really in contention here – though it should not be – is whether and to what extent the trade war and the uncertainty it has created bears primary responsibility for the weakening economy. Are there any empirical tests one could run that would establish this? Well, that question alone presents one of those black-hole methodological problems. No matter how much data one assembles and how many ways the data is manipulated, the problem of cause and effect in human affairs will always remain elusive. Still, it can be highly instructive to try.

The following economists have undertaken the mighty effort: Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. All five work for the Federal Reserve board. Their paper is extremely revealing on the relationship between erratic trade policy, tariffs, and economic trends.

They seek to measure the uncertainty of the trade regimes and its financial and macroeconomic effects. They deploy two data sets to codify uncertainty. First, they use a previously constructed metric based on automated text searches of the quarterly earnings call transcripts of U.S.-listed corporations. Second, the Fed constructed its own measure. They ran automated text searches of 7 major newspapers in its coverage of trade. The algorithms looked for words related to uncertainty such as risk, threat, and uncertainty. They measured the monthly share of articles that mentioned these and rescaled the mentions into an index.

These use econometric strategies to correlate changes in uncertainty with changes in financials and major economic data. What they end up with is a pattern that is suggestive as any pictures could be of the relationship between the two. That is to say, they conclude that trade uncertainty and policy are a key factor in the changed economic environment.

Let’s look at some of these.

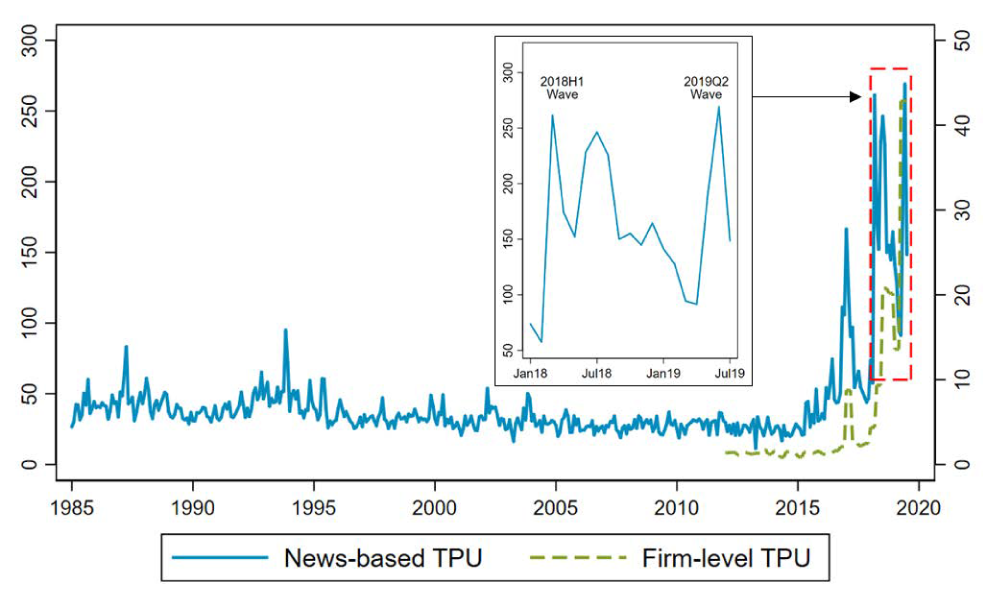

The first chart shows the results of the uncertainty index.

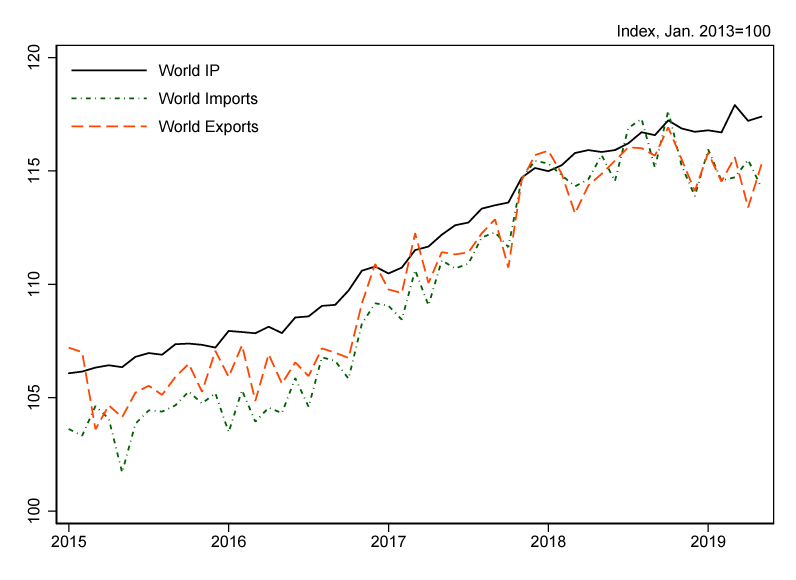

The second shows the trend in imports, exports, and industrial production.

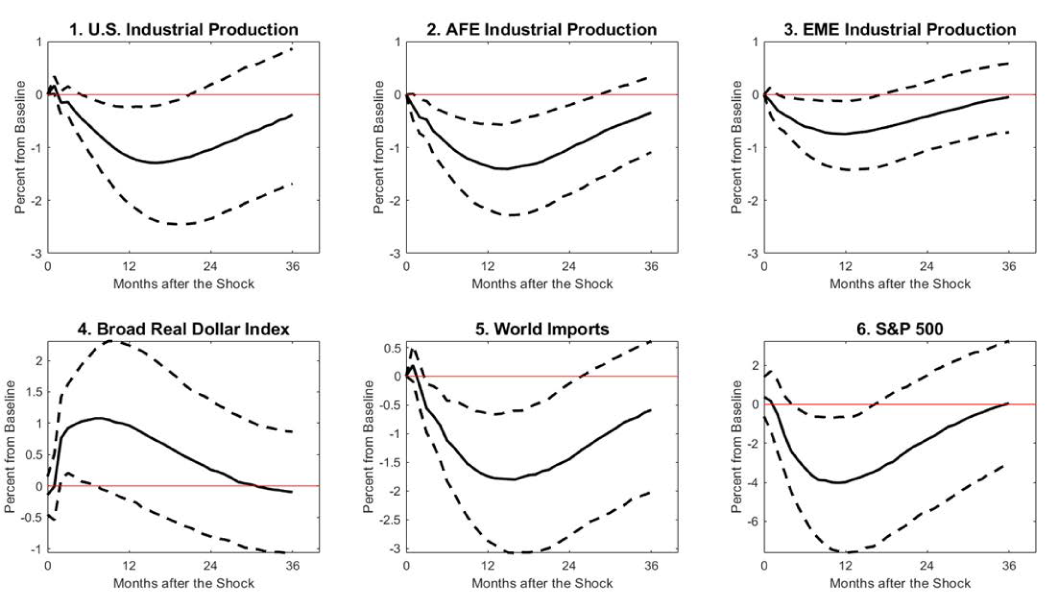

The third set shows the relationship between the two using vector autoregressive modeling techniques.

Sample from 1985M1 through 2019M5. The size of the shock matches the increase in TPU in March 2018.

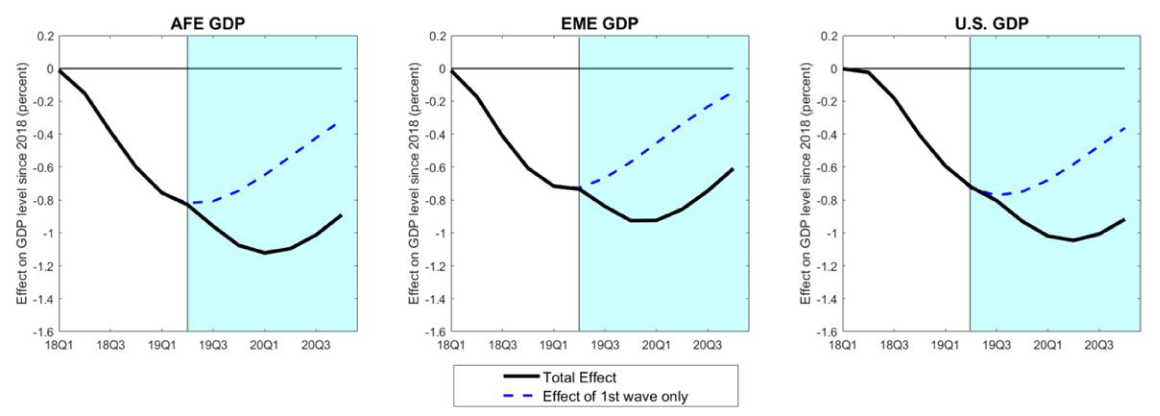

The fourth shows the relationship between uncertainty and GDP, and it includes counterfactual paths that might had been taken had the administration not pursued its policies.

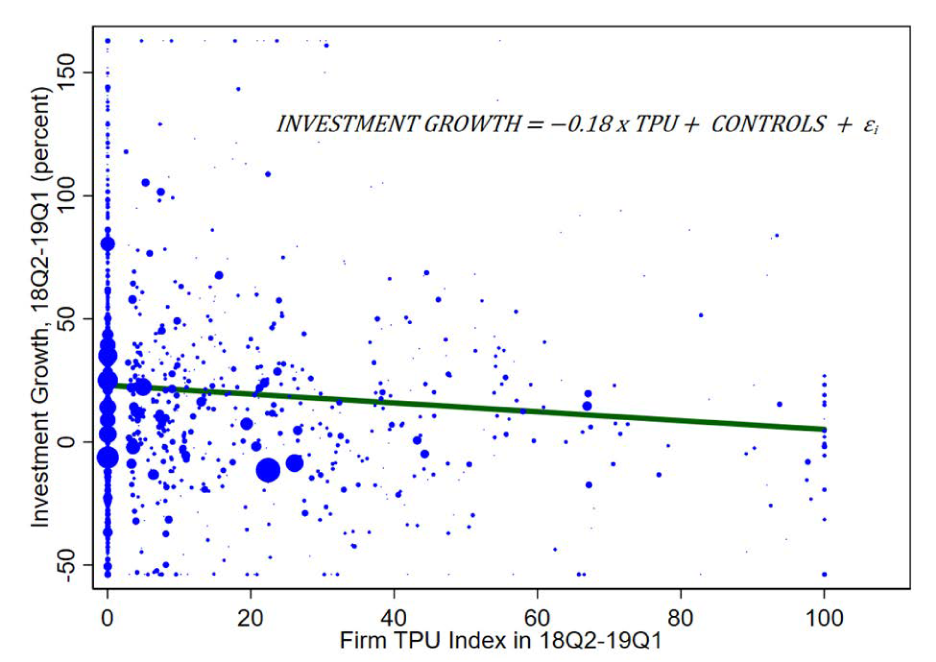

The final chart maps the relationship between trade-policy uncertainty and business investment.

The standard error of the regression coefficient is 0.076 with a p-value of 0.02.

Firm TPU is the average value of trade policy uncertainty over the four quarters, and is normalized so that it ranges from zero to 100.

Investment growth is the sum of capital expenditures for the four quarters ending in 2019Q1 relative to capital expenditures for the four quarters ending in 2018Q1.

The size of each dot is proportional to firm investment in 2017. Investment growth and trade uncertainty have been winsorized at the 5th and 95th, 1st and 99th, percentiles, respectively.

Source: Proquest, Compustat, and authors’ calculations.

Finally, they conclude:

Both the aggregate time-series analysis and the cross-sectional evidence suggest that higher trade policy uncertainty has adverse effects on GDP and investment, with these effects estimated to be protracted through time. This evidence is consistent with a large body of recent academic literature that documents the negative effects of other kinds of economic and policy uncertainty on economic activity. That said, the unprecedented size of the recent increases in trade policy uncertainty points to some degree of “uncertainty” around these estimates.

Just how much has trade policy harmed economic growth? No one knows but the models show the following:

We find that the rise in TPU in the first half of 2018 accounts for a decline in the level of global GDP of about 0.8 percent by the first half of 2019. Had trade tensions not escalated again in May and June 2019, the drag on GDP would have subsequently started to ease. However, renewed uncertainty since May of 2019 points to additional knock-on effects that may push down GDP further in the second half of 2019 and in 2020.

The last data point here is ominous. And true. No one expects things to get better before they get worse. This is the core of the concern. If the US and the world slide into recession, let no one claim that trade policy and the uncertainty it creates was not a dominant reason.

Jeffrey A. Tucker

Jeffrey A. Tucker served as Editorial Director for the American Institute for Economic Research from 2017 to 2021.