Cause and Control of the Business Cycle Today

The Great Recession was the worst economic downturn since the Great Depression. Like the Depression, the Great Recession was precipitated by a combination of excessive credit creation and misguided government policy. Excessive credit, or purchasing media, makes people feel wealthier than they really are, triggering unsustainable consumption. For decades, AIER has pointed to excessive credit creation as a risk to economic expansions.

Originally published in 1932, Col. E.C. Harwood’s “Cause and Control of the Business Cycle” described the process of economic booms and inevitable busts. (Harwood was the founder of AIER.) First, the boom aspect of the cycle is made possible by an excess of demand in relation to current production. Second, the depression phase of the cycle reflects a deficiency of demand in relation to current production. To some extent depression represents a recovery to a sound basis, a liquidation of past excess. In other words, a depression is the hangover after the party.

The Great Recession was caused by an over-extension of consumer credit and government policy. Easy money policies allowed banks to make many mortgage loans (later dubbed NINJA loans) to consumers. The acronym NINJA stands for “no income, no job application.” The banks turned around and sold the subprime mortgages to Fannie Mae and Freddie Mac. The banks would then relend the same money to another consumer. Both the banks and Fannie and Freddie lowered lending standards in response to the Community Investment Act, which sought to expand home ownership. The process of irresponsible lending, borrowing, and government policy led to a massive misallocation of capital to housing. The result has been a slow deleveraging and recovery process.

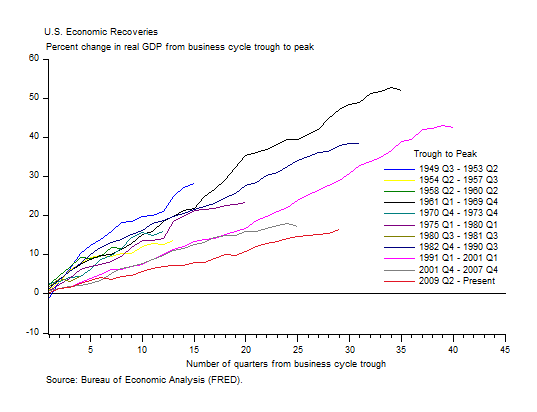

The current economic expansion has seen slow cumulative growth in real GDP compared with other post-World War II recoveries. Over the current expansion, real GDP has increased 16 percent from the trough, or low point, in 2009. In comparison, the strongest post-World War II recovery was from 1961 to 1969, when GDP grew 52 percent. In recent decades, economic recoveries have tended to be weaker. In the 1980s, expansions averaged 21 percent. During the go-go 1990s the economy expanded 43 percent, and after the dot-com bubble burst real GDP grew just 17 percent.

Although the current recovery is slow by historical standards, it is approaching the third longest. Looking ahead, does the current recovery have room to grow? Probably. Consumers are in decent shape with a solid labor market and improving household net worth. Corporate America is looking forward to a tax cut under President Donald Trump. A tax cut will likely help sluggish investment. AIER’s broad set of statistical indicators, which have a long history of predicting recessions, indicate a low risk of a recession in the coming months.