Bubbles, Technology, and Bitcoin

The price of cryptocurrencies have gone parabolic. It appears to many, that we are experiencing a mania. Individuals are moving into cryptocurrency markets who apparently have no intention of using these instruments as money. Are cryptocurrencies a bubble? If they are, is this necessarily a bad thing? More importantly, can we expect cryptocurrencies to be around for the foreseeable future?

To appropriately frame the emergence of the cryptocurrency market, it is useful to evaluate the significance and role of bubbles. A bubble occurs when an asset’s price exceeds its fundamental value–that is, the value produced or expected in the future. During the late 1990s, the tech sector experienced a boom that appears to have been a bubble. Investors realized the growing potential of tech and rushed in to exploit these gains. When money flows into a sector, investors seek to find companies that are undervalued, especially if they did not invest in the earliest stages of the boom. This tends to lift the whole sector. The NASDAQ composite index reached a value of over $5,100. It soon fell below $1,200. It would take more than a decade for the index to return to that height. Many investments were shown to have been bad bets for investors. But many proved their worth over the decade that followed the crash. The value of Apple (AAPL) stock grew from a low of around $0.45 to a well over $5. After the crash, it’s value hovered in the range of $1 to $2. Then, in 2004, the value of the stock started climbing and has followed a generally upward trend ever since. Was there a bubble in tech? Certainly. And Apple was part of this bubble. At the same time, Apple is a company that has proved to be extremely valuable. From the post-crash low, it’s value has increased by 17,900%!

Some view bubbles and the business fluctuations that accompany them as a problem to be avoided or, at the very least, moderated by monetary or fiscal policy. In an op-ed that briefly reviews the series of bubbles observed since the 1980s, Paul Krugman notes that “the main lesson of this age of bubbles . . . is that when the financial industry is set loose to do its thing, it lurches from crisis to crisis.”

Krugman is right. The financial system may fuel bubbles from time to time. What he does not seem to realize, however, is that this is both necessary and efficient so long as the bubble is not the result of state-led market distortions like the ones we observed during the recent housing crisis. Absent intervention, a bubble is a sign that the market has discovered potential for value creation. Jason Potts argues that “bubbles are a normal part of the market capitalist system when they emerge spontaneously from the market discovery process, and problematic only when artificially induced by ill-considered policy.”

Assets subject to an industry wide boom are not easy to price. As we observed with the NASDAQ bubble, investors rush in to find assets that they believe are undervalued. As the bubble progresses, however, pricing seems to lack an anchor. Part of the reason for this is that not only are lower quality assets being included in the bubble, but lower quality investors are entering into the market. Once liquidity dries up and the firms and investors face the strain of a decreased flow of funds, prices finally correct to reflect underlying value. Those assets that were bid up by uninformed investors must be liquidated. Due to the systemic nature of credit fluctuations, many assets that truly have higher earning potential will also lose value during the crisis period. But, as with Apple stock, those assets will be revalued sooner or later.

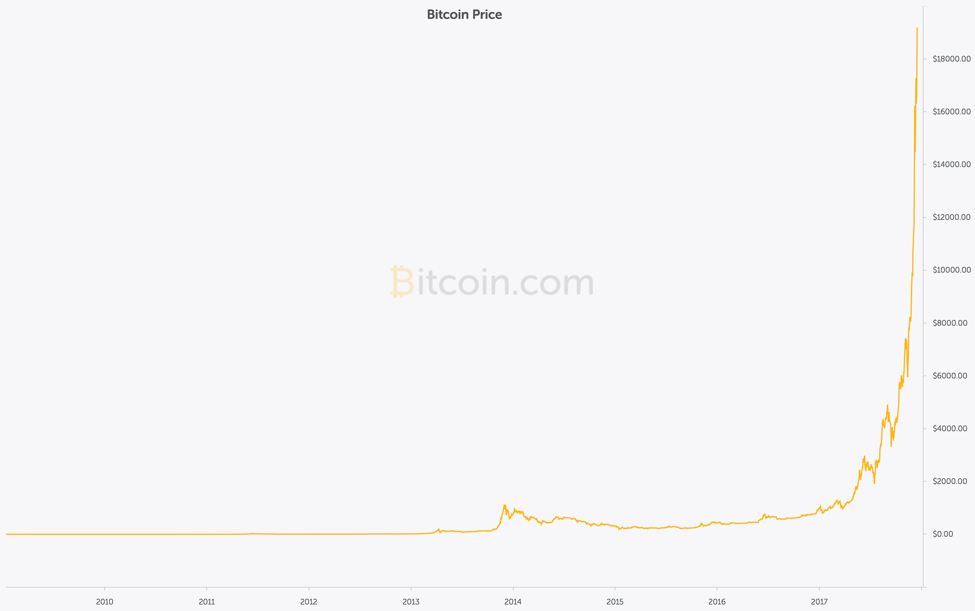

A sketch of bubbles can inform our interpretation of Bitcoin and the cryptocurrency market more generally. Bitcoin has been the most popular cryptocurrency, leading the others in terms of price and market capitalization. Discussion of a bubble in Bitcoin began in 2013, when it surged from just over $10 in value to over $100 and again to over $1000. Its most recent surge to over $19000 is again leading many to speculate that it is in bubble territory.

Following behind Bitcoin are a number of other cryptocurrencies, like Litecoin and Bitcoin Cash (a hard fork originating from Bitcoin). The alt-coins have also experienced a significant rise in value over the last year, as investors speculate on whether they might provide superior service on different margins and even challenge Bitcoin’s status the most dominant cryptocurrency. And the market for cryptocurrencies is by no means thin. The top 100 cryptocurrencies by market capitalization are valued at over $500 billion at present. It is possible that this value will continue to grow as more investors enter this market. But one thing seems certain: cryptocurrencies are attracting the resources necessary to develop and sustain highly functional platforms that may one day lead to their use as a currency, much as F. A. Hayek imagined over 40 years ago. There will probably be a downturn at some point that thins the market. However, we can expect that the most functional currencies will remain in use in much the same way that Apple survived the tech crunch more than 15 years ago.

James L. Caton

James L. Caton is an Assistant Professor in the Department of Agribusiness and Applied Economics and a Fellow at the Center for the Study of Public Choice and Private Enterprise at North Dakota State University. His research interests include agent-based simulation and monetary theories of macroeconomic fluctuation. He has published articles in scholarly journals, including The Southern Economic Journal, the Journal of Entrepreneurship and Public Policy, and the Journal of Artificial Societies and Social Simulation. He is also the co-editor of Macroeconomics, a two-volume set of essays and primary sources in classical and modern macroeconomic thought. Caton earned his Ph.D. in Economics from George Mason University, his M.A. in Economics from San Jose State University, and his B.A. in History from Humboldt State University.