Understanding the Affordable Care Act

While the vast majority of people in the United States had health insurance before the ACA, the new law is aimed at people who would not or could not buy insurance. It is also aimed at those referred to as the underinsured, people who have health care coverage that does not adequately protect them from high medical expenses.

The provisions of the ACA that affect insurance costs for individuals are being implemented over a number of years. Congress intended its core elements to become effective in 2014. However, some pieces of the law relating to employer mandates and some individual insurance requirements are being delayed by the Obama administration until 2015 and 2016. Other provisions do not become effective until 2018.

The ACA will have its greatest impact on the insurance costs of the uninsured, those in the individual insurance market, and many in the small group market. Most of those covered by large group plans and by federal programs are likely to see fewer changes to their health insurance costs directly attributable to the ACA.

How Americans Were Insured Before the ACA

Just 5 percent of people in the United States, 16 million, purchased insurance directly from insurance providers in the individual market, as shown in Figure 1 on page 1. Another 5 percent were covered in the small group market.

The largest share of the insured, some 147 million in 2012, got their health coverage through group plans sponsored by their employers or that of their spouses or parents. These group plans are divided between large groups (51 or more employees, changing to 101 or more in 2016) and small groups (2-50 employees, increasing to 2-100 in 2016). Large group insurance covered 131 million in 2012, while small group insurance covered approximately 16 million.

The government is the next largest source of health insurance in the U.S. Fully 49 million people, or 16 percent, are covered by Medicare, the federal health program for Americans who are aged 65 and older. Medicaid, a joint federal and state program for low-income people, provided health coverage for 46 million people in 2012, or 14 percent of the U.S. population. Another 3 percent of the population received coverage through federal health care programs such as the Child Health Insurance Program, TRICARE (for uniformed members of the military), the Indian Health Service, and the Veterans Affairs program.

Nearly 15 percent of the U.S. population, an estimated 46 million in 2012, had no health insurance during most of the calendar year. Three-quarters of these uninsured are in families with incomes near or below the federal poverty level ($11,670 for an individual and $23,850 for a family of four in 2014 within the continental U.S.). The remaining uninsured have annual incomes ranging from two-and-a-half to four times the poverty level (between $29,175 and $46,680 for an individual and between $59,625 and $95,400 for a family of four in 2014).

How the ACA Affects Insurance Costs

The ACA does not create a national health insurance plan. Rather, it sets national standards for how health insurance is structured and priced, and places new requirements on individuals and employers.

The new law affects health insurance premiums and out-of-pocket costs in a few fundamental ways. It establishes insurance exchanges where people can purchase individual coverage from participating insurers. It mandates that all individuals acquire health insurance and requires that businesses with more than 50 employees offer health insurance to their full-time employees.

The ACA also requires that insurance plans in the individual and small group markets provide coverage for 10 specific benefits, shown in the table below. It also caps out-of-pocket costs and provides federal subsidies to help lower-income people pay for premiums and out-of-pocket costs, and establishes financial incentives to states that expand Medicaid coverage.

The combined effect of these features is likely to increase premiums for millions of people and to reduce them for millions of others. Many people will be required to purchase more coverage than they prefer, which will increase their costs. Other people will pay more for the same amount of coverage they had before the ACA because their premium calculations will include people with higher health-risk profiles.

At the same time, many will purchase coverage they could not buy at any price before the law because of a pre-existing condition. Moreover, the broader coverage required by the law and the limits it places on out-of-pocket costs will reduce the amount many will pay in the event that they need health care.

A quirk in the new law and the refusal of some states to expand Medicaid has created a coverage gap for millions of people. Because the ACA anticipated that all states would expand Medicaid eligibility, it sets a minimum income level to qualify for premium subsidies. However, 25 states did not expand Medicaid. As a result, millions of people in these states have incomes that are too high to qualify for Medicaid and too low to qualify for subsidies through the insurance exchanges created by the ACA.

Most people, however, are unlikely to see much change in their insurance costs from the ACA, at least in the short term. That is because the vast majority of people in the United States get their health insurance through a large group plan at work or through Medicaid or Medicare. The ACA makes only modest changes to the way insurance is provided in large group plans.

Moreover, most large group plans are excluded from the ACA’s benefits mandates and out-of-pocket caps. For instance, self-funded plans, which insured 61 percent of covered workers in 2013, are exempt from many ACA requirements. So, too, are grandfathered plans, that is, plans already in place in 2010 that have not been significantly altered since.

How Many Pay Less? How Many Pay More?

It is very difficult to directly compare pre-ACA insurance costs with post-ACA costs and to know how many people will see higher costs because of the ACA and how many will see lower costs. The available data on premiums in the individual and small group markets is very limited. Moreover, individual and small group insurance plans prior to the ACA varied so widely that averaging costs across states and the nation would be difficult to interpret.

In addition, the degree to which the ACA affects an individual’s insurance costs will depend largely on how and where people acquire coverage. Finally, important elements of the law have been delayed. So, many of the decisions by employers and individuals that will affect costs have yet to be made.

Nonetheless, we make rough estimates of how many people are likely to face higher premiums, lower premiums, or see little change in premiums. We also estimate how many people will likely be protected from high out-of-pocket costs and how many will not.

Among those likely to face the stiffest cost increases are people who purchase insurance in the individual market and who do not qualify for federal subsidies. Previously uninsured people who do not qualify for federal subsidies are also likely to experience significant cost increases.

So will most workers who are dropped from their employers’ small or large group plans. These people must purchase insurance in the individual market where they pay full premium costs and lose the benefit of sharing costs with their employer. It’s not likely that a large number of people will be in this position because employers who drop insurance will have more difficulty competing for workers.

Those likely to see the greatest cost benefits from the ACA are people who qualify for federal subsidies and those now eligible for Medicaid. People with high-risk health profiles who purchase insurance in the individual market will also likely see substantial savings. Their premiums are now based largely on the average health risks of those in the region in which they live, rather than on their individual condition. Moreover, these higher-risk individuals now receive coverage for services for which they previously had to pay in full.

Many small group employers face conflicting pressures from the ACA. For many small group plans, the ACA’s stricter limits on medical underwriting will help hold down premium costs. However, employers will also face upward price pressure from the additional administrative costs associated with complying with the ACA and the costs of higher take-up rates by employees.

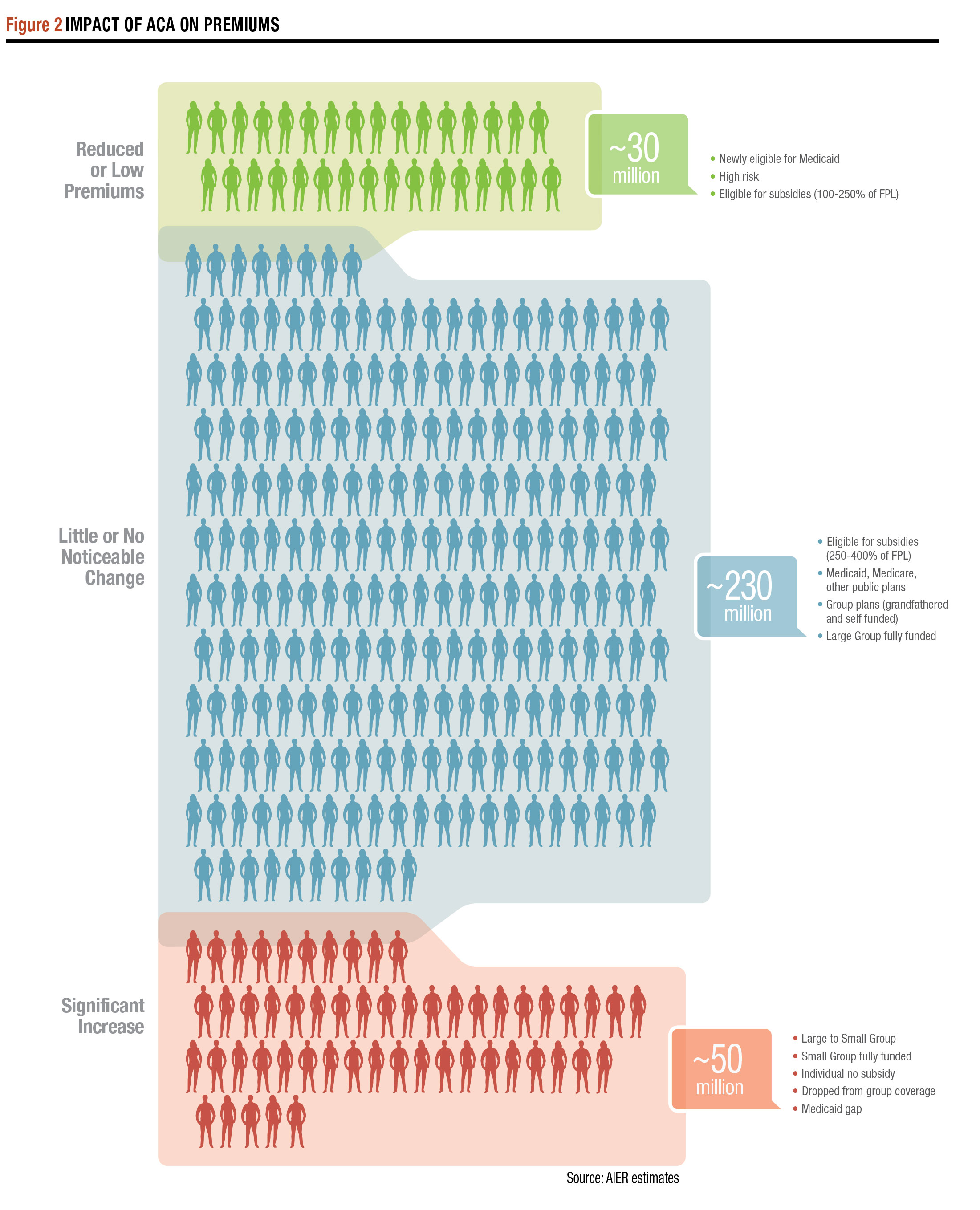

Figure 2 on page 4 illustrates how the ACA is likely to affect premiums paid by individuals. As it shows, more than 30 million people will likely see insurance premiums decline or be very inexpensive. This includes about 3 million low-income individuals who purchased insurance in the individual market and who are eligible for subsidies to help pay premiums and/or out-of-pocket expenses. It also includes another 3 million from the individual market who are now eligible for Medicaid because of the ACA. This group also contains about 26 million uninsured who either are now eligible for Medicaid or for subsidies to reduce health insurance costs.

Approximately 230 million in the U.S. who get insurance from a large employer plan or government program such as Medicare or Medicaid will see little noticeable change in their insurance costs attributable to the ACA.

More than 50 million people could pay higher premiums, some sharply higher. These include people purchasing insurance in the individual market who must buy more coverage because of ACA requirements, and those whose premiums are driven up by being grouped with higher-risk people. Also in this group are many of the roughly 9 million people estimated by AIER to lose their employer-sponsored coverage. Some of those facing higher premiums may elect to not purchase insurance and will pay a penalty.

Roughly 6 million people fall into the Medicaid coverage gap. They have incomes above their state’s Medicaid eligibility and below the level required to qualify for ACA subsidies. Those in this gap who elect to purchase insurance will likely see steep premium increases.

At the same time that many will see higher premiums, the ACA will reduce the out-of-pocket costs of most covered people who use significant amounts of health care services. The minimum benefits standard established by the ACA means that people who would have purchased less generous benefits will now be covered for additional health costs should they need services. The law also eliminates lifetime limits on the benefits paid by insurers and sets caps on deductibles for many plans. It also provides subsidies for out-of-pocket costs for some low-income people.

The benefit of out-of-pocket cost limits applies only to those who actually incur health care expenses. Moreover, the out-of-pocket cost limits established by the ACA do not apply to the roughly 53 million people with grandfathered insurance plans.

An Uncertain Path to Success

The success of the Affordable Care Act depends greatly on how people, employers, and insurers respond to the environment created by the new law. It also depends on how well the costs to taxpayers are kept under control.

A principal measure of ACA success will be whether enough people from a range of risk profiles purchase health insurance in the individual market. The Congressional Budget Office estimates that 22 million will enroll by 2016. However, the flawed rollout of the federal and state exchanges has dampened enrollment.

As of March 1, 4.2 million had selected a plan on a state or federal exchange, fewer than the 7 million originally estimated to enroll during the year by the CBO and the Joint Committee on Taxation. (The CBO reduced this estimate to 6 million in 2014 to reflect the rollout problems.)

Even these sign-up figures may overstate the true number of people enrolling in health insurance plans on the exchanges. Insurance companies have reported that as many as 20 percent of those who selected a plan in January have not paid premiums and could lose their insurance.

How firms will respond is also unknown. The ACA assumes few significant changes in employer behavior with regard to health insurance, especially among large group employers (more than 100 employees). But various employer surveys suggest a wide range of possibilities. In a 2011 study by McKinsey and Company, 30 percent of responding firms said they would probably or definitely drop insurance altogether, despite the federal penalty. A 2013 survey of employers by Towers Watson found just 1 percent likely to drop insurance altogether.

The CBO estimated that 6 million people will be removed from their employers’ plans. Most of these are expected to be part-time employees in larger firms, as the employer mandate to offer insurance extends only to full-time workers.

However, an unknown number of small firms could also drop insurance altogether. These employers are more likely than large firms to see significant premium impacts. In addition, the ACA imposes significant new administrative requirements that will be disproportionately burdensome on small firms.

If many more small firms drop insurance than anticipated when the ACA was adopted, more people would enter the individual market and more would join the uninsured. However, the small group market now represents only 5 percent of all insured people and will represent less than 9 percent in 2016, when the small group expands to include firms with up to 100 employees. So, even a larger-than-anticipated reaction by small firms will have a limited impact.

The ACA anticipates that a balance of healthy and less healthy enrollees into the individual market will hold down rate increases. It also closely circumscribed how premiums would be set in 2014, the initial year of operation for the public exchanges. CBO estimates assume that premiums will rise by an average 6 percent annually after that. In fact, premiums could rise much higher. As insurers absorb actual experience, premiums will come to reflect the usage rates and revenues from the newly insured. If a disproportionate number of heavy users of health care enroll, premiums are likely to rise faster than anticipated.

The combination of increasing health care costs and even modest ACA-related premium increases could also affect the insurance purchase decisions of individuals and businesses. Increases in health care costs have been relatively low in recent years, as shown in Figure 3, above, in part because of lower demand. The ACA could drive up demand for health services and push up costs. This would contribute to premiums rising above levels acceptable to many consumers and businesses, and lead more businesses to drop insurance and more individuals to remain uninsured.

It also remains to be seen if the taxpayer costs of the ACA can be held within acceptable bounds. The CBO has estimated that by 2016 annual subsidy costs would reach $85 billion and the cost of Medicaid expansions would rise to $62 billion. By 2018, these are estimated to reach $118 billion per year and $76 billion per year, respectively.

Actual subsidy costs will depend on the number of people who sign up, the pace of premium cost increases, and the rate of increase in the cost of health care services. Lower-than-expected sign-ups will reduce total demand for subsidies, but it could drive premiums higher if the number of higher risk people dominates the newly insured population. Medicaid expansion costs will depend on whether more states expand eligibility and the pace of health care cost increases.

Acknowledgements

AIER benefited from the advice and cooperation of numerous individuals including Jeyaraj (Jay) Vadiveloo PhD, FSA, MAAA, CFA, professor and director of the University of Connecticut Goldenson Center for Actuarial Research and his team: Mark Spong, Nehal Sapre, and Pete Camacho. AIER would also like to thank Nancy Trumbull of Harvard School of Public Health; Nancy Kane of Harvard Business School; Marilyn Tavenner and Teresa Miller at the Centers for Medicaid and Medicare Services of the U.S. Department of Health and Human Services; Ryan Lore of Towers Watson; and Daniel Okwaisie, AIER intern. All analysis and any errors or omissions are the responsibility of AIER.

This Executive Brief summarizes the findings of an AIER analysis of the impact of the Patient Protection and Affordable Care Act, also known as the Affordable Care Act, on insurance costs through 2016. The full Research Study, including a bibliography, appendices, and the methodology, is available at https://www.aier.org/cost-Affordable-Health-Care-Act.

[pdf-embedder url=”https://www.aier.org/wp-content/uploads/2014/05/AIER_ACAExecutive-Brief_March2014.pdf“]Luke F. Delorme

Luke F. Delorme is Director of Financial Planning for American Investment Services. Articles do not constitute personal investment advice. Please seek the advice of a professional before implementing any financial decision. Luke can be reached at LukeD@americaninvestment.com.