Deposit Insurance Is Not Fair

Although most people assume that FDIC insurance prevents bank failures, the expected net effect of government deposit insurance on bank failures is, at best, unclear. On the one hand, deposit insurance discourages bank runs. If depositors know their money is insured by the government, then they have no reason to run on a bank. As such, we should expect fewer run-generated bank failures and panics under a government deposit insurance regime. On the other hand, deposit insurance poses a moral hazard problem. If bankers know that insured depositors are unlikely to withdraw funds from risky banks, they can boost their returns by taking on additional risk without fear that customers will move their savings to more prudent banks. Thus, deposit insurance might increase the number of risky banks and bank failures.

In theory, the problem of moral hazard can be offset if the government sets deposit insurance premiums exactly equal to the bank’s cost of risk—that is, the actuarially fair rate for deposit insurance. If the rate assessed for insurance is too low, then banks are likely to increase their risk-taking activities. If the rate is too high, then banks will constrain credit, resulting in less economic activity than is desirable. In other words, the actuarially fair rate provides the perfect balance of risk minimization and economic production maximization.

In practice, the actual cost of FDIC insurance has differed markedly from most estimates of the actuarially fair rate. This is not surprising considering how the FDIC manages its Deposit Insurance Fund (DIF). Rather than operating a true insurance program, the DIF is treated like a rainy-day fund. The FDIC assesses member banks with an annual fee and these funds accumulate over time in the DIF. When a bank fails, the DIF is depleted in order to repay insured depositors. Then, assessment rates are raised on the remaining banks to replenish the fund. In other words, the FDIC’s assessment rates are based on actual historical losses. Actuarially fair insurance, in contrast, sets rates according to expected future losses.

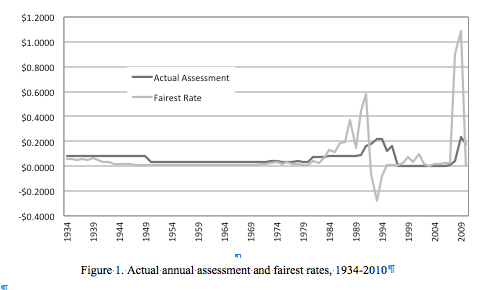

In Figure 1, we present the actual assessment rate in each year between 1934 and 2010 alongside the actuarially “fairest” rate in each year. Over the history of the program, the average annual rate of DIF losses is roughly 0.05 percent – that is $0.05 cents per $100 in deposits. After including annual expenses, the average fairest rate ranges from 0.06 to 0.09 percent per year. Actual rates were less than the average fairest rate from 1934 to 1941, 1950 to 1980, and again from 1997 to 2008. Recall that, when the price of insurance is lower than the actuarially fair rate, banks have an incentive to take excessive risk. For example, an actuarially fair rate would have been high in 2006 with risk building up in the banking system, but the actual assessment rate was only $0.0005, the lowest rate in FDIC history!

The FDIC has also erred in the opposite direction. From 1942 to 1949, 1981 to 1996, and again from 2009 to 2010, actual rates exceeded the average fairest rate. Recall that, when the price of insurance is higher than the actuarially fair rate, banks overpay for insurance. Resources that could have been marshaled to fund useful banking services will instead be devoted to providing insurance, making depositors worse off.

Our rough comparisons of actual assessment rates and the actuarially fairest rates are consistent with the bulk of historical studies on deposit insurance. Studies of the FDIC find that higher levels of deposit insurance are associated with higher rates of bank failures and that the moral hazard created by deposit insurance may have contributed to the Savings & Loan crisis of the 1980s and the recent financial crisis of 2008.[i] More generally, studies of deposit insurance systems around the world find that “the relationship between deposit insurance and bank fragility is economically large”[ii] and “countries with an explicit deposit insurance scheme were particularly at risk.”[iii] Unlike the United States, most developed nations have partly or fully privatized deposit insurance systems that are associated with few failures and crises.[iv]

Despite the widespread belief that government deposit insurance reduces the number of bank failures, the consensus view emerging from the academic literature is that higher levels of deposit insurance and more government involvement in the deposit insurance system are associated with higher probabilities of bank failures and financial crises. These higher rates of failures and crises occur in part because government deposit insurance is not fairly priced according to actual levels of bank risk. To prevent the next crisis, we should look to private alternatives to government deposit insurance.

[i] See pp.435-437 in Hogan, Thomas L. and Kristine Johnson (2016) “Alternatives to the Federal Deposit Insurance Corporation,” The Independent Review 20(3): 433-454.

[ii] P.237 in Barth, James R., Gerard Caprio, and Ross Levine (2004) “Bank Regulation and Supervision: What Works Best?” Journal of Financial Intermediation 13(2): 205–248.

[iii] P.81 in Demirgüc-Kunt, Asli, and Enrica Detragiache (1998) “The Determinants of Banking Crises in Developing and Developed Countries,” IMF Staff Papers 45(1): 81–109.

[iv] Prior to the creation of the FDIC, US states created a variety of government and private deposit insurance systems. As with more modern experiments with deposit insurance, studies of this period find that “state-run systems were largely unsuccessful and increased bank failures” while “self-regulating systems privately managed by banks that bore a portion of liability were the most successful.” See pp.440-441 in Hogan and Johnson (2016).

Thomas L. Hogan

Thomas L. Hogan, Ph.D., is senior research fellow at AIER. He was formerly the chief economist for the U.S. Senate Committee on Banking, Housing and Urban Affairs. He has also worked at Rice University’s Baker Institute for Public Policy, Troy University, West Texas A&M University, the Cato Institute, the World Bank, Merrill Lynch’s commodity trading group and for investment firms in the U.S. and Europe. Dr. Hogan’s research has been published in academic journals such as the Journal of Macroeconomics and the Journal of Money, Credit and Banking. He has appeared on programs such as BBC World News, Stossel TV, and Bloomberg Radio and has been quoted by news outlets including CNN Business, American Banker, and the National Review.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.