Third-Quarter Real GDP Is Revised Higher; Profits Hit a Record

Revised estimates show real GDP grew at a 3.3 percent pace in the third quarter compared to a 3.1 percent pace in the second quarter. The initial estimate for the third quarter was 3.0 percent. The upward revision was spread across several segments of the economy, with the largest coming in fixed investment. The latest report on the economy also provided an initial estimate for third-quarter corporate profits and revised estimates for prices. Most elements of the report suggest the economy remains in very good condition, with moderate real growth, continued gains in profits, and tepid price increases.

Real personal consumption expenditures grew at a revised 2.3 percent pace, slightly below the 2.4 percent gain in the initial estimate and significantly below the 3.3 percent pace of the second quarter. Spending on durable goods and consumer services both decelerated in the quarter while spending on nondurable goods accelerated.

Fixed investment posted a 2.4 percent pace in the latest quarter, revised up from a 1.5 percent gain in the initial estimates. The upward revision still leaves the pace of growth below the 3.2 percent gain in the second quarter. Business (nonresidential) fixed investment posted a 4.7 percent gain, led by a 10.4 percent jump in equipment and a 5.8 percent rise in intellectual products, while nonresidential-structure investment fell 6.8 percent. Residential investment (housing) posted its second consecutive quarterly decline, dropping 5.1 percent following a 7.3 percent drop in the second quarter.

Combined, PCE, business investment, and housing rose at a 2.3 percent pace in the third quarter, below the 3.3 percent pace of the second quarter. These core components, also know as private domestic demand, have been the main drivers of growth over the past several years. Despite the slowdown in the third quarter, fundamentals supporting private domestic demand remain very solid and are likely to support faster growth over the next several quarters.

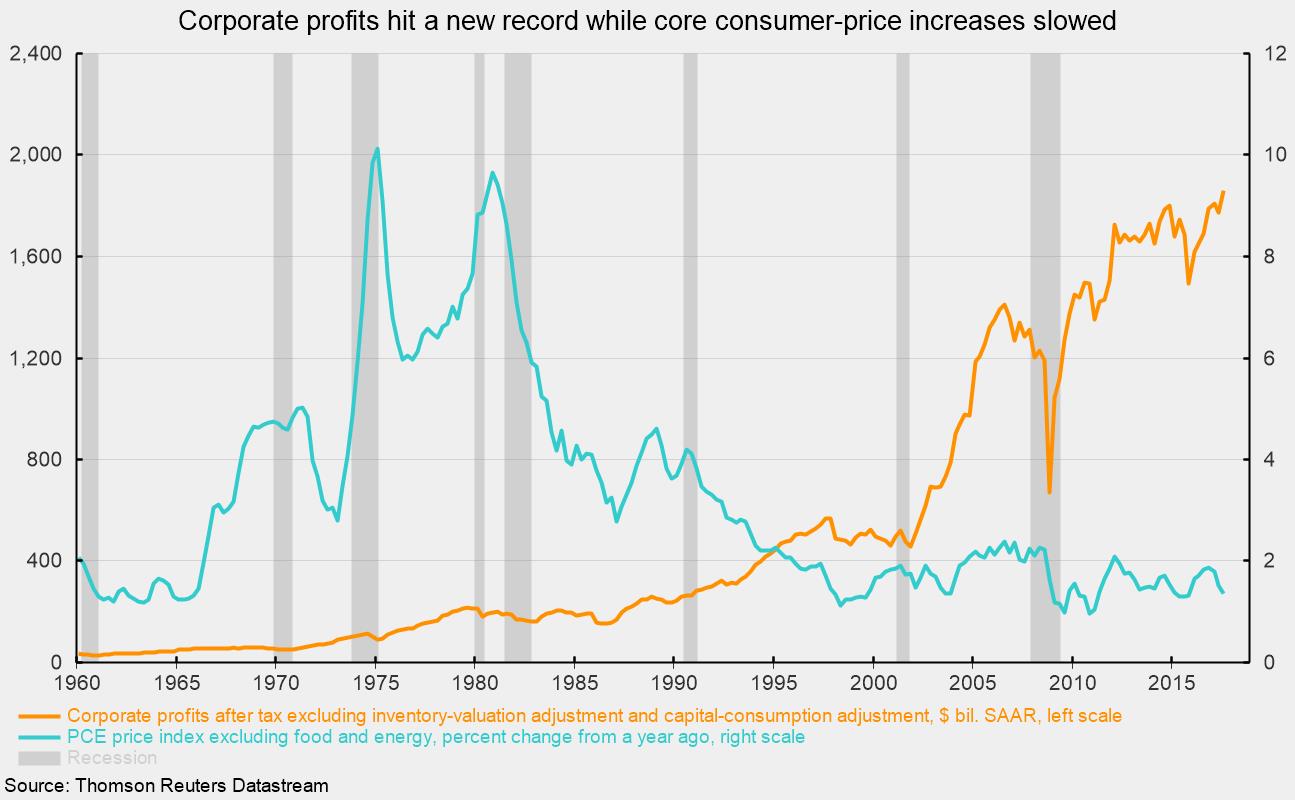

Solid growth from domestic demand combined with accelerating growth overseas has helped push U.S. corporate profits to a new record high. For the economy in aggregate, after-tax corporate profits excluding inventory-valuation adjustments and capital-consumption adjustments — both used in national income accounting — hit an all-time high of $1.86 trillion at a seasonally adjusted annual rate in the third quarter (see chart). That represents a 10.0 percent gain from the third quarter of 2016. These economy-wide measures corroborate public companies’ reports — followed closely by market analysts — of generally strong corporate earnings. Strong profits gains combined with solid growth in demand, low cost of capital, and generally healthy balance sheets for the corporate sector suggest a positive outlook for future business fixed investment.

The third key aspect of the latest report on the broad economy is the continued tepid increases in prices. The overall GDP price index rose at a 2.1 percent pace compared to just 1.0 percent in the second quarter. Over the last four quarters, the GDP price index is up a more mild 1.8 percent. The largest price increases in the third quarter came from residential and nonresidential structures (both increasing 4.5 percent), services imports (up 5.0 percent), and state and local prices (rising 3.2 percent).

PCE prices, the measure preferred by the Fed, rose 1.5 percent in the third quarter. From a year ago, the PCE price index is up 1.5 percent while the core PCE prices index, which excludes volatile food and energy items, is up just 1.4 percent over the last year. The core PCE price index has been rising at less than 2 percent for most of the past 20 years (see chart). That stretch of sub-2 percent increases is about as close to price stability as the United States has ever experienced.

Overall, economic data suggest an economic environment with solid growth and slow price increases that is likely to continue well into 2018.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.