The Trouble With Stephen Moore

On Friday, President Trump announced via Twitter that he would nominate Stephen Moore to fill one of two vacancies on the Federal Reserve’s Board of Governors. A political pundit and former editorial board member of the Wall Street Journal, Moore is currently a distinguished visiting fellow at the Heritage Foundation.

Many economists took to Twitter following the announcement. And they were not pleased. “Moore’s monetary commentary has for well over a decade been relentlessly partisan, illogical, and fact-fudged,” wrote Benn Steil, a senior fellow and director of international economics at the Council on Foreign Relations. “This is appalling.”

“This is the first genuinely bad Trump pick for the Fed. But make no mistake: It’s a terrible, horrible, no good, very bad pick,” Justin Wolfers, a professor of public policy and economics at the University of Michigan, remarked. “He hasn’t gotten a thing right in twenty years, (check the record), and the Senate should not confirm him.”

“Here’s my challenge to any informed voter of any partisan leaning,” Wolfers continued. “Call your favorite economist. Whether they’re left, right, libertarian or socialist, none of them will endorse Stephen Moore for the Fed. He’s manifestly unqualified.”

I hate to pile on. But they are right: Moore is a terrible pick. His views on monetary policy are either ignorant or hyper-partisan. And his appointment would further politicize a Fed that is already seriously lacking in independence.

Most economists accept that the monetary authority should do its best to mitigate aggregate demand shocks. If nominal spending growth declines, the Fed should increase the growth rate of money to prevent a recession. If nominal spending growth increases, the Fed should decrease the growth rate of money to prevent an unsustainable boom. Economists of different persuasions might quibble about how best to achieve that end — whether the Fed should target nominal income, inflation, or the federal funds rate or, instead, use its discretion while considering a host of indicators. But, by and large, they agree on the overall objective.

Moore’s stated positions are difficult to reconcile with the consensus view. In the depths of the Great Recession, when nominal spending had collapsed, he advised against increasing the growth rate of money. “I call this, you know, the Argentina, Bolivia and Mexico model of economic development,” Moore said in November 2010. “Because that’s what those countries do — they print money every time they get into this kind of crisis.”

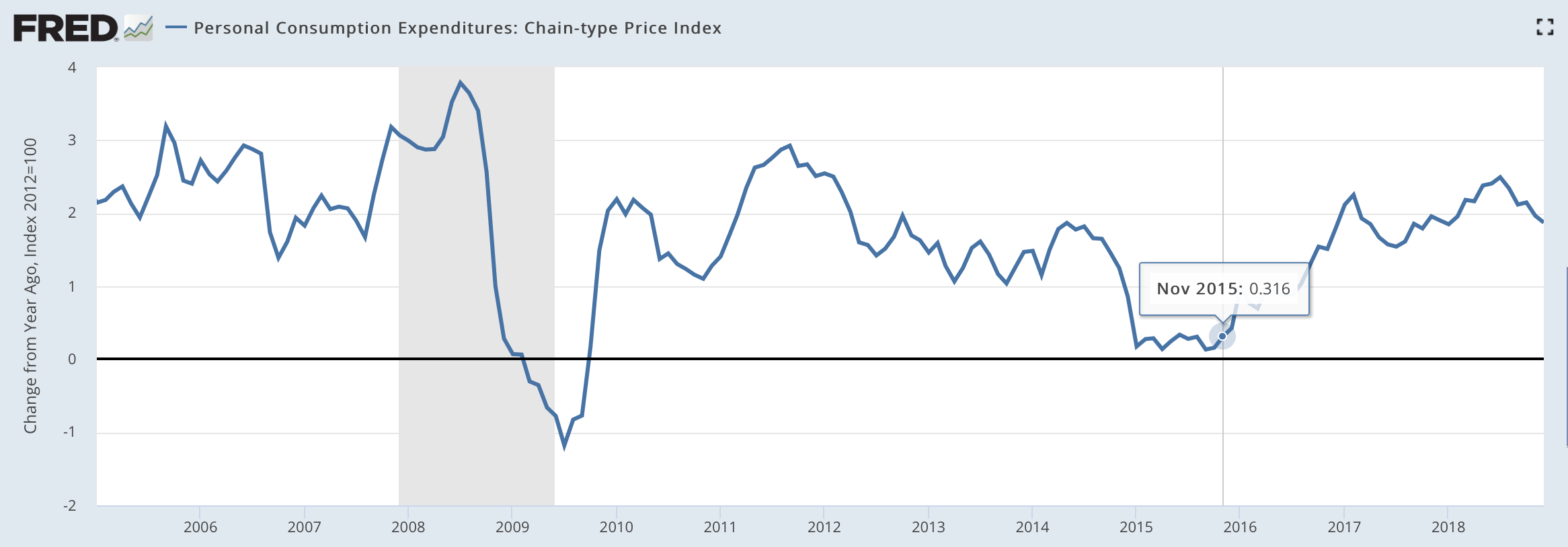

Even as late as November 2015, when the inflation rate was just 0.32 percent (down from a mere 1.25 percent a year earlier), Moore worried that the Fed was “potentially creating another bubble.”

More recently, Trump’s pick has erred in the opposite direction. After a decade of undershooting its target, the Fed is finally achieving 2 percent inflation. The unemployment rate is down to 3.8 percent. Nominal spending growth appears to be more or less in line with what market participants expect. But, despite all of the evidence, Moore thinks “the Fed should be worried about deflation.” Indeed, he maintains that we are currently experiencing deflation.

Let me be clear: we are not experiencing deflation. Prices are going up. The Bureau of Labor Statistics initially announced that the Consumer Price Index (CPI) had declined 0.1 percent in December (though it was still up 1.9 percent for the year). However, the December estimate was ultimately revised to 0.0 percent, with the price level increasing by 1.5 percent from February 2018 to February 2019. At most, the CPI suggests we are experiencing a disinflation — the rate of inflation has declined. We are not experiencing deflation — a negative rate of inflation. A Fed governor should know the difference.

Moore points to commodity prices to support his view. However, most economists agree that the Fed should look past changes in volatile commodity prices, which largely reflect real shocks and rarely persist. As George Selgin, director of the Cato Institute’s Center for Monetary and Financial Alternatives, writes in a letter to the Wall Street Journal:

…contrary to Mr. Moore’s claims, “core” inflation rate measures, which exclude energy and food prices and are, for that reason, less volatile and more reliable inflation measures, have been both remarkably stable and very close to the Fed’s two percent target over the last six months — and longer. The core CPI rate has actually remained slightly above two percent, while the core PCE (Personal Consumption Expenditures) rate, the Fed’s preferred measure, has hovered just an insignificant smidgen below it.

Again: we are not experiencing deflation.

While Moore’s stated positions are consistently at odds with the consensus view in macroeconomics, they map incredibly well to a hyper-partisan policy framework. As the Mercatus Center’s Scott Sumner has written, Moore seems to favor “tighter money when a Democrat is president, and the economy is depressed and clearly needs easier money,” and “easier money when Trump is president, and the economy is booming and does not obviously need easier money.”

Moore provides further support for the hyper-partisan explanation. Whereas most economists would prefer to insulate the Fed from short-term political pressures, Moore seems to want a Fed that is entirely beholden to the president — at least while his man is in the White House. “Who is the Fed responsive to, if not the president?” he said on CNN in December 2018.

Moore has also recommended that President Trump fire Chairman Powell. “What the law says, I believe, is he can replace the Federal Reserve Chairman for cause,” he remarked in a recent interview. “And, you know, I would say, well, the cause is that he’s wrecking our economy.”

The Fed is far from perfect. It exacerbated the two biggest macroeconomic downturns in American history. It generated stagflation in the 1970s. It could be much better than it is. But it could also be much worse. Adding Stephen Moore to the Board of Governors would be a step in the wrong direction.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News. Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.