GAO Endorses Small Change

In a recent report on U.S. coinage, the General Accountability Office (GAO) made three recommendations:

- It argued against replacing the $1 bill with a $1 coin.

- It suggested altering the metal content of the nickel.

- It cast doubt on the benefits of suspending production of the penny.

The GAO is certainly correct in its first recommendation. Replacing the $1 banknote with a $1 coin doesn’t make much sense. But how about changing the composition of the five-cent coin and maintaining the status of the penny?

Changing the metal composition of the nickel

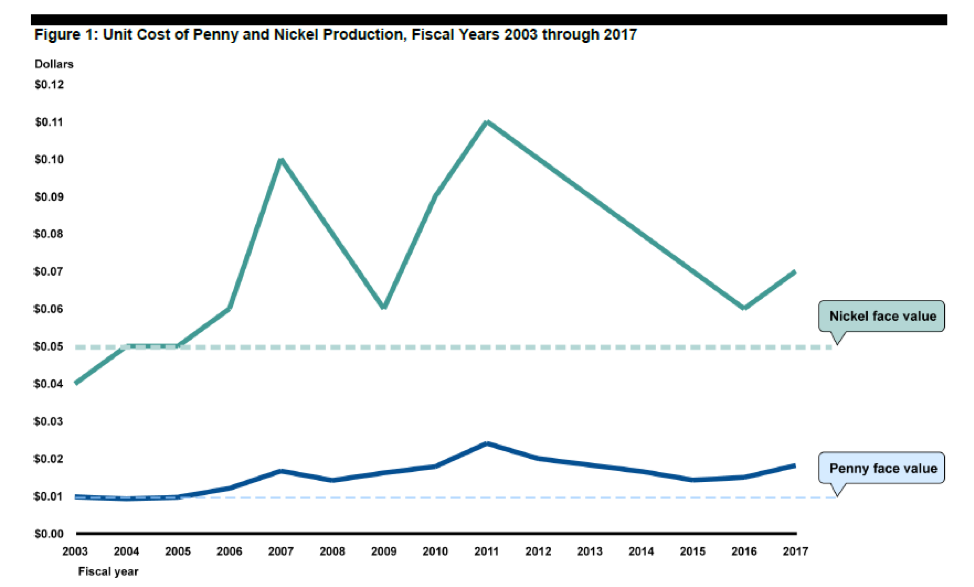

The nickel currently consists of 75 percent copper and 25 percent nickel. According to the GAO, by moving to 80 percent copper and 20 percent nickel or by changing the metal composition to a copper, nickel, manganese, and zinc alloy (C99750T-M), the U.S. Mint could save a few million dollars per year.

This is a good idea, but it wouldn’t do much to fend off a much bigger problem. The commodity value of a five-cent coin is currently around four cents. A doubling in copper and nickel prices would push the metal value of the nickel well above its face value. When the commodity value of a coin exceeds its face value, people have an incentive to melt it down and sell the metal in raw form.

Speculators are already starting to hoard nickels in anticipation of this event. In 2011, hedge fund operator Kyle Bass bought 20 million nickels for storage.

Hoarding and melting can lead to crippling small-change shortages. The U.S. would see a repeat of the 1960s, when shortages of nickels and quarters appeared after the silver value of U.S. coinage approached and then exceeded the coins’ face value.

Reducing the intrinsic value of the nickel is one way to put off the inevitable melting and hoarding of nickels and ensuing coin shortages. But going from a 75/25 nickel to an 80/20 nickel or one made of C99750T-M (as the GAO recommends) wouldn’t achieve more than a token reduction.

One alternative is to emulate countries like Canada that have begun to produce nickels out of steel. But there are a number of hassles that the American public would have to cope with if the metal composition of the five-cent coin changed too dramatically. For example, vending machines often read a coin’s electromagnetic signature to determine its denomination. A move to steel coinage would require the vending machine industry to make significant — and pricey — changes to its coin-reading apparatuses.

There are other ways to put off the inevitable coin shortages. In 2006, the mint implemented a rule banning the melting down or export of nickels. The punishment is up to five years in prison and a fine of up to $10,000. But these sorts of punishments can’t stop melting. They can only render the process riskier. And they can’t stop nickel hoarding by speculators such as Kyle Bass.

The most definitive solution is to simply put an end to the minting of the nickel and require retailers to round receipts to the nearest dime (see the discussion of Swedish rounding below). New Zealand did this back in 2006. Which gets us to the penny.

Suspending the one-cent coin

Where the GAO report goes awry is where it discusses suspending production of the penny.

For many Americans, the penny is little more than monetary detritus. To provide small change to customers, businesses buy pennies from banks, which in turn buy them from the Fed. The pennies that get paid out to the public rarely get re-used or re-deposited. Rather, consumers tend to either throw them in the garbage or forget about them in piggy banks.

Making matters worse is that each penny that the mint fabricates costs 1.6 cents to produce. In 2017, the mint lost $69 million producing pennies!

Source: GAO

The GAO addressed a very specific question in its report: should production of the penny be suspended for 10 years? Although a suspension would save taxpayers hundreds of millions of dollars, the GAO has refused to recommend it. To support its conclusion, it has cited Federal Reserve officials, who noted that “suspending production could create a shortage of pennies if demand is greater than the supply of pennies.”

Now, the Fed officials are entirely right. When a customer pays for a $4.96 purchase with a $5 note, stores need pennies on hand so that they can make change. If the mint stops producing pennies, then stores will be left without a way to accurately settle bills.

But the GAO hasn’t taken the next step in its analysis. All nations that have ended the penny (Canada, Australia, Finland) have simultaneously implemented a complementary policy that reduces the demand for pennies, thereby preventing a shortage. This policy is sometimes referred to as Swedish rounding.

Under Swedish rounding, retailers are free to continue setting their sticker prices in penny terms — for example, the ever-popular $0.99 or $1.99. But when the final receipt is printed out at the checkout counter and bills or coins are presented as payment, the amount owed gets rounded to the nearest five cents. (Debit and credit card payments are still settled to the penny.) That way shops never need to have any pennies on stock. If the U.S. adopted this policy, the Fed’s concerns about coin shortages would be allayed.

By leaving its analysis incomplete, the GAO missed an opportunity to free Americans from the shackles of the penny. The burden will only increase over time as inflation pushes the mint’s labor and materials costs higher but the penny’s face value stays fixed.

J.P. Koning

J.P. Koning is a financial writer and blogger with interests in monetary economics, economic history, finance, and fintech. He has worked as an equity researcher at a Canadian brokerage firm and a financial writer and publisher at a large Canadian bank. More recently, he has written several papers for R3, a distributed ledger company, on the topics of central bank cryptocurrency and cross border payments. He founded the popular blog Moneyness in 2012. He designs economics and financial wallcharts at Financial Graph & Art.

Koning earned his B.A. in Economics from McGill University.