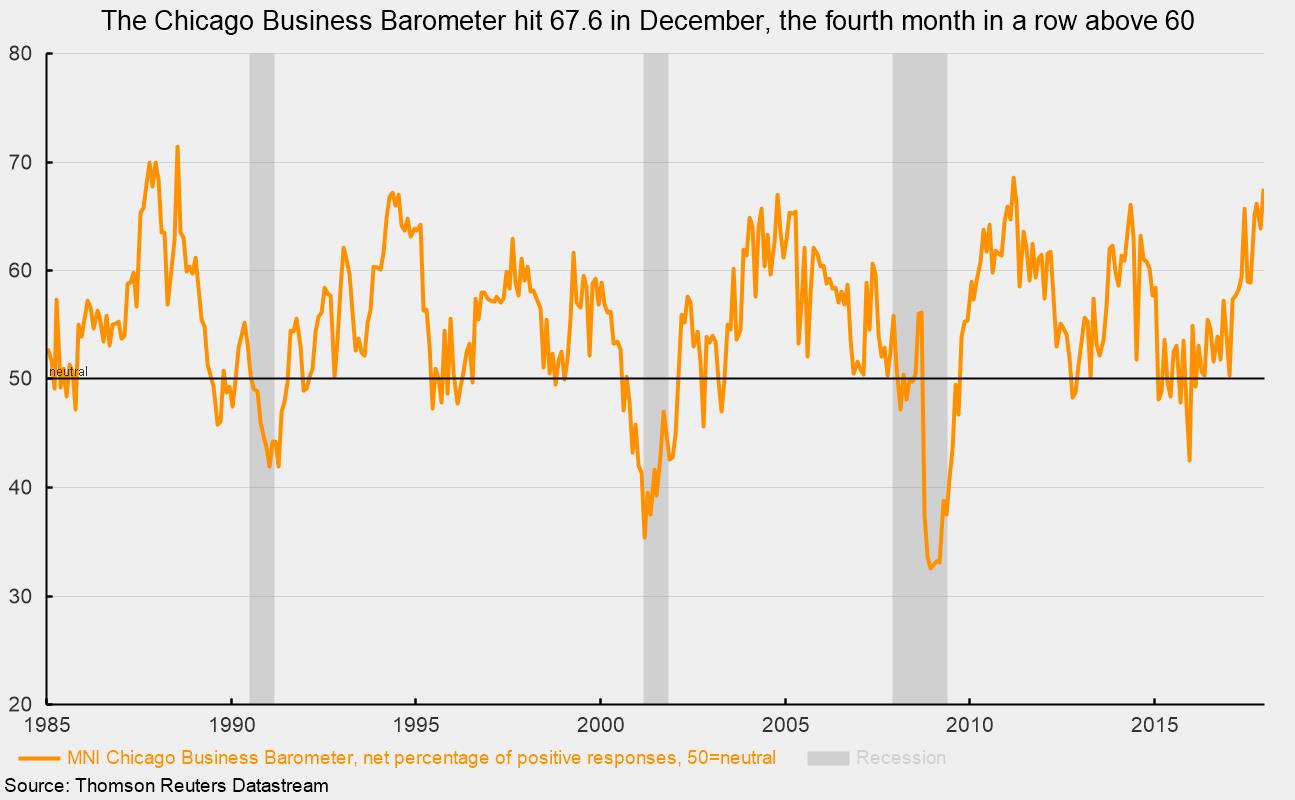

Chicago Business Barometer Rises to Highest Level Since 2011

The Chicago Business Barometer, a composite index based on a survey of purchasing managers in the Chicago area, rose 3.7 points to 67.6 in December, the highest level since March 2011. December also marks the fourth month in a row with a reading above 60, the first such occurrence since 2014. The index is the net percentage of positive responses to the survey questions, with 50 being neutral.

Among the components of the composite index, output and demand posted strong gains in the latest month, with both hitting multi-year highs. Production matched the highest level in 34 years while new orders rose to a three-and-a-half-year high.

Employment expanded in December but at a slower pace than in November as the employment indicator fell slightly in the latest month but remained above neutral. Over the last 12 months, the employment index has fallen below the neutral 50 level just four times.

Order backlogs increased in December. The unfulfilled-orders indicator rose in December but remained below October levels. Substantial backlogs are generally considered a positive sign for future production.

Supplier delivery times shortened in December compared to November, with the indicator dropping to the lowest level since April. Despite the drop in the delivery-times indicator, delivery times remain somewhat lengthy by historical measures. Furthermore, inventories rose in November as the Inventories indicator hit a new three-year high in December. According to the report, “There was evidence of firms carrying a larger level of stock to support stretched lead times and in preparation for product launches scheduled for the New Year.”

Price pressures continued for manufacturers in December, though the price indicator for input materials did fall to the lowest level since August. According to the report, “The upswing in global demand, along with input shortages induced by this year’s hurricanes, saw prices elevated throughout the year.”

Finally, each month the survey asks special questions. According to the report:

This month’s special question asked firms to predict how both their businesses and the US economy would fare in the upcoming new year. Just over 50% saw their company growing somewhere between 0-5%, with 37% forecasting growth between 5-10% and the remaining 12% expecting growth above 10%. Regarding the bigger picture, 61% of firms thought the US economy would grow somewhere in the region of 2 to 5% over 2018, while 29% put growth at between 0 and 2%. Just under 6% of businesses saw the US economy contracting in 2018 while the remaining 4% saw economic growth running above 5%.

Overall, the results of the latest survey of Chicago-area purchasing managers suggest continued economic growth for the region.

Also out this morning were weekly initial claims for unemployment insurance. Weekly claims held at 245,000 for the week ending December 23. That is unchanged from the prior week. The four-week average, used to help smooth out weekly volatility, came in at 237,750, above the prior four-week average of 236,000. Claims remain at multi-decade lows in absolute terms, and claims remain near all-time record lows as a share of employment.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.