Policy

Elections and the Economy

The election season is heading into the final stretch. The state of the economy and economic policies, actual or proposed, are almost always among the most debated election topics, and this cycle is no exception.

For decades, politicians from both parties, from the president on down, have praised their own economic record and found fault with that of their opponents. But when looking at the larger economic picture over the past 60 years or so, it is hard to argue that one party has systematically performed better than the other.

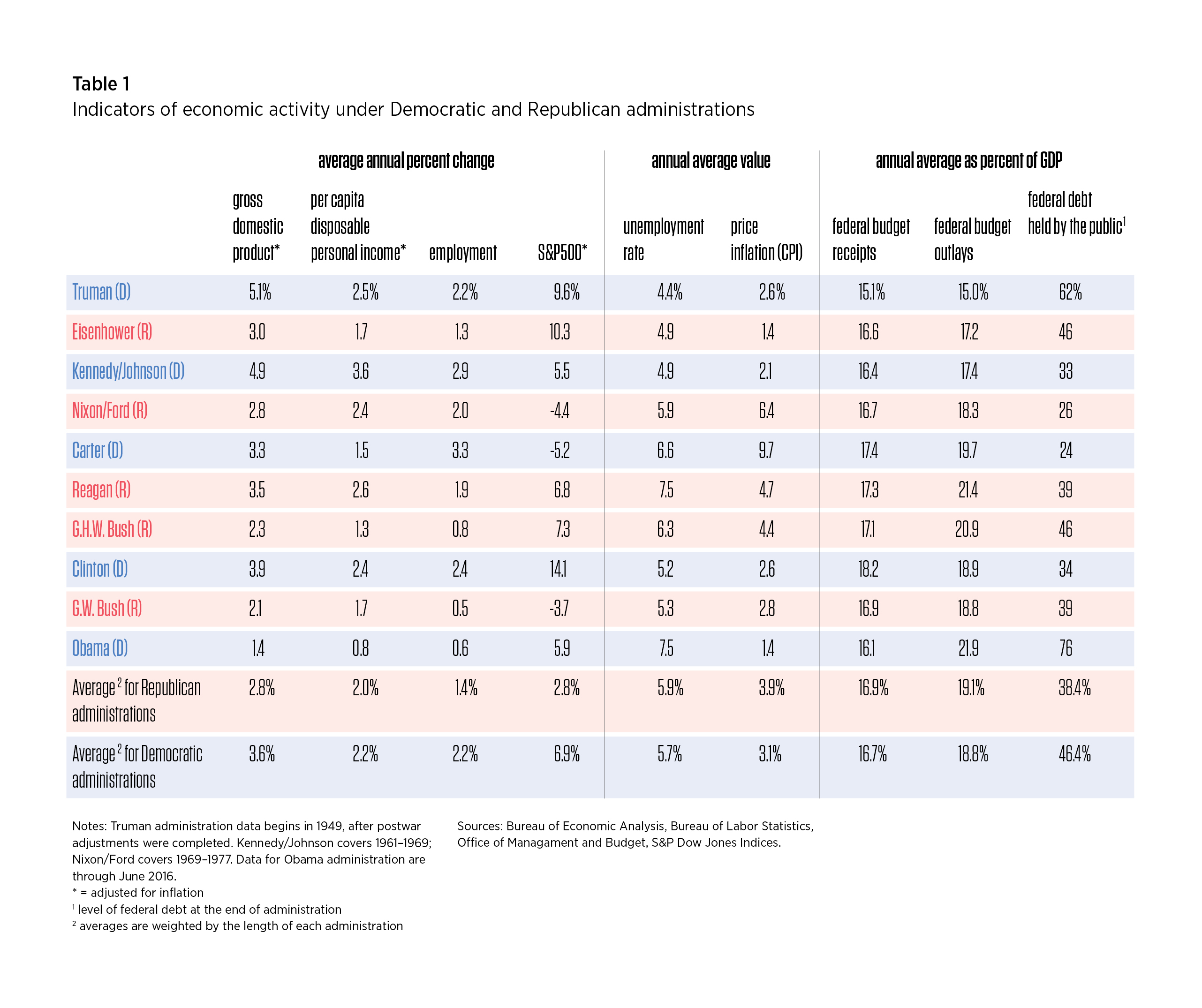

Table 1 presents a summary of economic measures during every presidential administration since 1949. But these numbers should be interpreted with caution, because economic processes take time to play out, making it tricky to attribute the effects of an economic policy. To avoid charges of subjectivity, we are following the common convention of looking at economic data by the calendar year of each administration.

The data show a mixed record for both parties. The periods of highest growth in gross domestic product, the main measure of economic output, were during the Truman, Kennedy, and Johnson administrations, all Democrats. But the slowest GDP growth was also during a Democratic administration (Obama).

The lowest unemployment rates were seen during the Truman, Eisenhower, Kennedy, and Johnson administrations, and Clinton’s also came close. The highest unemployment was during the Reagan and Obama administrations. The fastest job growth was during the Carter administration, followed by the Kennedy, Johnson, and Clinton years. The slowest was during the George W. Bush and Obama administrations—in other words, around the Great Recession.

The fastest growth in income per person (disposable income per capita) happened during Democratic administrations (Kennedy and Johnson), but the slowest also happened under a Democratic president (Obama). The stock market performed well under Clinton, growing in excess of 10 percent a year. Somewhat slower, but similar growth, was seen under Eisenhower.

The largest increase in the federal debt occurred during the Obama administration, when the federal debt held by the public reached 76 percent of GDP. This level was exceeded only at the start of the Truman administration, which inherited high debt after World War II.

These comparisons show that the economy’s performance is most likely not determined by the political party holding the presidency. The forces that affect the economy do not depend on the president, and they act over long periods of time.

The bulk of the Great Recession took place during the George W. Bush administration, but most of its aftermath unfolded under Obama. However, the forces that brought it about—monetary policy, housing policies, new financial instruments, and many others—were set in motion years or even decades before. The decline in manufacturing employment, which eroded the economic base in many cities, diminished union membership, and, some would argue, led to stagnating U.S. wages, happened over decades, driven by forces that no president could possibly stop.

Similarly, the apparent stellar performance of the economy during the Truman and Eisenhower administrations may have more to do with the U.S. (and global) economy recovering after World War II than with anything these presidents did.

Nevertheless, presidential candidates will always claim that they have the recipe for improving the economy. This happens because the voters would like to hear it, not because it is, or can be, supported by data. Elections may also influence the behavior of the Federal Reserve, even though the Fed is usually thought to be isolated from politics. Some economists who analyze monetary policy argue that the Fed (and central banks in general) avoids adjusting monetary policy close to an election for fear of being accused of political meddling. There is not enough data to convincingly demonstrate this behavior, because there have only been a few elections when interest rates could easily be used to characterize monetary policy.

But the logic behind the argument is compelling, and it suggests that the Fed would be even more reluctant to raise interest rates later this year as we approach election day, Nov. 8. At its latest meeting, in July, the Fed left interest rates unchanged. This was widely expected. If the economic data remain subdued, and with the election approaching, the Fed may not want to raise interest rates for a while.

Next/Previous Section:

1.Overview

2. Economy

3. Policy

4. Investing

5. Appendix