The never-ending Argentine fiscal business cycle

15 years after carrying out the biggest sovereign default in its history, Argentina finally reached a debt accord with its holdouts. The agreement between Mauricio Macri’s administration and the holdout litigants in the U.S. Court of Law has finally been reached. This is good news for the country. The government can resort, if needed, to international financial markets and issue government debt. Until now this possibility was constrained to only a few creditors like Venezuela, who would charge a considerably high interest rate to lend money to the Kirchner administration, its political ally.

The big question that remains unanswered is what the government plans to do with this new scenario. Is there going to be a serious fiscal reform to put an end to 60 years of fiscal deficit, or is it the access of credit going to be used to finance a slow gradual reduction in the fiscal deficit that endangers the success of the plan. The Argentine economy is quite weak. Can it bear another four years of gradually reduced deficits? If one looks at Argentine history, the spikes in GDP growth rates were not the result of successful gradual plans, but rather the outcome of forced shock policies after the failure of gradual plans (late 1980s/early 1990s and 2001 crises). Because the “shock” policies were implemented by necessity more than conviction, these policies were usually not consistent in the long-run, unnecessarily costly, and not fully implemented.

The case of Argentina is of international interest. In the last decades, it has pushed policies that are present in many countries of the Western World (North America and Europe) to their limits. The problem with structural, or chronic, fiscal deficits is that sooner or later they affect a country’s currency. It is very hard to have a sound and strong money when the Treasury cannot control itself. If debt is not an option to finance the deficit, then “printing money” becomes the alternative. That’s what happened in the 1980s and 2000s in Argentina. When debt is an option, then the problem can be a default. That’s what happened to Argentina in 2001. Now that Argentina is to gain access to credit markets, is it going to repeat the mistakes of the 1990s or will there be a genuine change? It is too early to say, but some expressions from government officials are not very promising. When the fiscal deficit is pushed to its limits there are two options: (1) a fiscal reform or (2) transfer the cost to the society through inflation or default.

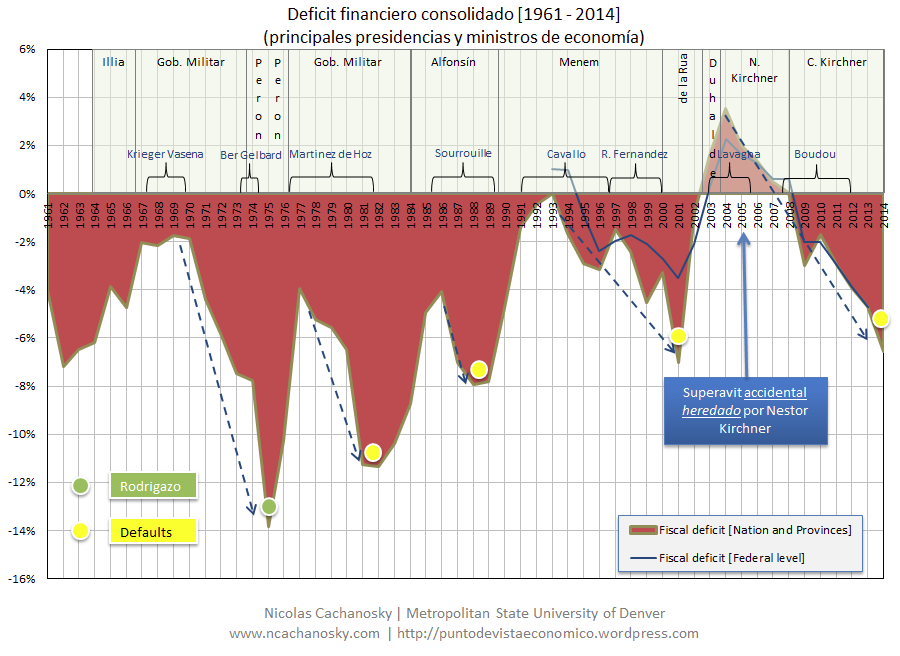

Pundits often mention the Argentine crisis of 2001 as a reference when Greece was going through its debt crisis not so long ago. But just as Argentina’s actions in the year 2000 that put her in a satiation of stagflation with unmatched conditions in the international markets have been studied, economists should also pay attention to what Argentina does from here on out. The picture below shows the fiscal deficit of Argentina over the last 50 years. Will it change from now on, or is the country going to fall for the same temptation to spend as previous governments have?

Nicolás Cachanosky

Dr. Cachanosky is Associate Professor of Economics and Director of the Center for Free Enterprise at The University of Texas at El Paso Woody L. Hunt College of Business. He is also Fellow of the UCEMA Friedman-Hayek Center for the Study of a Free Society. He served as President of the Association of Private Enterprise Education (APEE, 2021-2022) and in the Board of Directors at the Mont Pelerin Society (MPS, 2018-2022).

He earned a Licentiate in Economics from the Pontificia Universidad Católica Argentina, a M.A. in Economics and Political Sciences from the Escuela Superior de Economía y Administración de Empresas (ESEADE), and his Ph.D. in Economics from Suffolk University, Boston, MA.

Dr. Cachanosky is author of Reflexiones Sobre la Economía Argentina (Instituto Acton Argentina, 2017), Monetary Equilibrium and Nominal Income Targeting (Routledge, 2019), and co-author of Austrian Capital Theory: A Modern Survey of the Essentials (Cambridge University Press, 2019), Capital and Finance: Theory and History (Routledge, 2020), and Dolarización: Una Solución para la Argentina (Editorial Claridad, 2022).

Dr. Cachanosky’s research has been published in outlets such as Journal of Economic Behavior & Organization, Public Choice, Journal of Institutional Economics, Quarterly Review of Economics and Finance, and Journal of the History of Economic Thought among other outlets.