This piece was originally published by Alt-M

By George Selgin

At the risk of sounding like a broken record (well, OK–at the risk of continuing to sound like a broken record), I’d like to say a bit more about economists’ tendency to get their monetary history wrong. In particular, I’d like to take aim at common myths about the gold standard.

If there’s one monetary history topic that tends to get handled especially sloppily by monetary economists, not to mention other sorts, this is it. Sure, the gold standard was hardly perfect, and gold bugs themselves sometimes make silly claims about their favorite former monetary standard. But these things don’t excuse the errors many economists commit in their eagerness to find fault with that “barbarous relic.”

The false claims I have in mind are mostly ones I and others–notably Larry White–have countered before. Still I thought it would be useful to address them again here, because they’re still far from being dead horses, and also so that students wrapping-up the semester will have something convenient to send to their misinformed gold-bashing profs (though I urge them to wait until grades are in before sharing!).

For the sake of those who don’t care to wade through the whole post, here is a “jump to” list of the points covered:

1. The Gold Standard wasn’t an instance of government price fixing. Not traditionally, anyway.

2. A gold standard isn’t particularly expensive. In fact, fiat money tends to cost more.

3. Gold supply “shocks” weren’t particularly shocking.

4. The deflation that the gold standard permitted wasn’t such a bad thing.

5. It wasn’t to blame for 19th-century American financial crises.

6. On the whole, the classical gold standard worked remarkably well (while it lasted).

7. It didn’t have to be “managed” by central bankers.

8. In fact, central banking tends to throw a wrench in the works.

9. “The “Gold Standard” wasn’t to blame for the Great Depression.

10. It didn’t manage money according to any economists’ theoretical ideal. But neither has any fiat-money-issuing central bank.

1. The Gold Standard wasn’t an instance of government price fixing. Not traditionally, anyway.

As Larry White has made the essential point as well as I ever could, I hope I may be excused for quoting him at length:

Barry Eichengreen writes that countries using gold as money ‘fix its price in domestic-currency terms (in the U.S. case, in dollars).’ He finds this perplexing:

But the idea that government should legislate the price of a particular commodity, be it gold, milk or gasoline, sits uneasily with conservative Republicanism’s commitment to letting market forces work, much less with Tea Party–esque libertarianism. Surely a believer in the free market would argue that if there is an increase in the demand for gold, whatever the reason, then the price should be allowed to rise, giving the gold-mining industry an incentive to produce more, eventually bringing that price back down. Thus, the notion that the U.S. government should peg the price, as in gold standards past, is curious at the least.

To describe a gold standard as “fixing” gold’s “price” in terms of a distinct good, domestic currency, is to get off on the wrong foot. A gold standard means that a standard mass of gold (so many grams or ounces of pure or standard-alloy gold) defines the domestic currency unit. The currency unit (“dollar”) is nothing other than a unit of gold, not a separate good with a potentially fluctuating market price against gold. That one dollar, defined as so many grams of gold, continues be worth the specified amount of gold—or in other words that one unit of gold continues to be worth one unit of gold—does not involve the pegging of any relative price. Domestic currency notes (and checking account balances) are denominated in and redeemable for gold, not priced in gold. They don’t have a price in gold any more than checking account balances in our current system, denominated in fiat dollars, have a price in fiat dollars. Presumably Eichengreen does not find it curious or objectionable that his bank maintains a fixed dollar-for-dollar redemption rate, cash for checking balances, at his ATM.

Remarkably, as White goes on to show, the rest of Eichengreen’s statement proves that, besides not having understood the meaning of gold’s “fixed” dollar price, Eichengreen has an uncertain grasp of the rudimentary economics of gold production:

As to what a believer in the free market would argue, surely Eichengreen understands that if there is an increase in the demand for gold under a gold standard, whatever the reason, then the relative price of gold (the purchasing power per unit of gold over other goods and services) will in fact rise, that this rise will in fact give the gold-mining industry an incentive to produce more, and that the increase in gold output will in fact eventually bring the relative price back down.

I’ve said more than once that, the more vehement an economist’s criticisms of the gold standard, the more likely he or she knows little about it. Of course Eichengreen knows far more about the gold standard than most economists, and is far from being its harshest critic, so he’d undoubtedly be an outlier in the simple regression, y = α + β(x) (where y is vehemence of criticism of the gold standard and x is ignorance of the subject). Nevertheless, his statement shows that even the understanding of one of the gold standard’s most well-known critics leaves much to be desired.

Although, at bottom, the gold standard isn’t a matter of government “fixing” gold’s price in terms of paper money, it is true that governments’ creation of monopoly banks of issue, and the consequent tendency for such monopolies to be treated as government- or quasi-government authorities, ultimately led to their being granted sovereign immunity from the legal consequences to which ordinary, private intermediaries are usually subject when they dishonor their promises. Because a modern central bank can renege on its promises with impunity, a gold standard administered by such a bank more closely resembles a price-fixing scheme than one administered by a commercial bank. Still, economists should be careful to distinguish the special features of a traditional gold standard from those of central-bank administered fixed exchange rate schemes.

2. A gold standard isn’t particularly expensive. In fact, fiat money tends to cost more.

Back in the early 1950s, and again in 1960, Milton Friedman estimated that the gold required for the U.S. to have a “real” gold standard would have cost 2.5% of its annual GNP. But that’s because Friedman’s idea of a “real” gold standard was one in which gold coins alone served as money, with no fractionally-backed bank-supplied substitutes. As Larry White shows in his Theory of Monetary Institutions (p. 47) allowing for 2% specie reserves–which is more than what some former gold-based free-banking systems needed–the resource cost of a gold standard taking advantage of fractionally-backed banknotes and deposits would be about one-fiftieth of the number Friedman came up with. That’s a helluva bargain for a gold “seal of approval” that could mean having access to international capital at substantially reduced rates, according to research by Mike Bordo and Hugh Rockoff.

Friedman himself eventually changed his mind about the economies to be achieved by employing fiat money:

Monetary economists have generally treated irredeemable paper money as involving negligible real resource costs compared with a commodity currency. To judge from recent experience, that view is clearly false as a result of the decline in long-term price predictability.

I took it for granted that the real resource cost of producing irredeemable paper money was negligible, consisting only of the cost of paper and printing. Experience under a universal irredeemable paper money standard makes it crystal clear that such an assumption, while it may be correct with respect to the direct cost to the government of issuing fiat outside money, is false for society as a whole and is likely to remain so unless and until a monetary structure emerges under an irredeemable paper standard that provides a high degree of long-run price level predictability.*

Unfortunately, neither White’s criticism of Friedman’s early calculations nor Friedman’s own about-face have kept gold standard critics from repeating the old canard that a fiat standard is more economical than a gold standard. Ross Starr, for example, observes in his 2013 book on money that “The use of paper or fiduciary money instead of commodity money is resource saving, allowing commodity inventories to be liquidated.” Although he understands that fractionally-backed banknotes and deposits may go some way toward economizing on commodity-money reserves, Starr (quoting Adam Smith, but failing to look up historic Scottish bank reserve ratios) insists nonetheless that “a significant quantity of the commodity backing must be maintained in inventory to successfully back the currency,” and then proceeds to build a case for fiat money from this unwarranted assertion:

The next step in economizing on the capital tied up in backing the currency is to use a fiat money. Substituting a government decree for commodity backing frees up a significant fraction of the economy’s capital stock for productive use. No longer must the economy hold gold, silver, or other commodities in inventory to back the currency. No longer must additional labor and capital be used to extract them from the earth. Those resources are freed up and a simple virtually costless government decree is substituted for them.

Tempting as it is to respond to such hooey simply by noting that the vaults of the world’s official fiat-money managing institutions presently contain rather more than zero ounces of gold–31,957.5 metric tons more, to be precise–that response only hints at the fundamental flaw in Starr’s reasoning, which is his treatment of fiat money as a culmination, or limiting case, of the resource savings to be had by resort to fractional commodity-money reserves. That treatment overlooks a crucial difference between fiat money and readily redeemable banknotes and deposits, for whereas redeemable banknotes and deposits are generally understood by their users to be close, if not perfect, substitutes for commodity money, fiat money, the purchasing power of which is unhinged from that of any former money commodity, is nothing of the sort. On the contrary: its tendency to depreciate relative to real commodities, and to gold in particular, is notorious. Consequently holders of fiat money have reason to hold “commodity inventories” as a hedge against the risk that fiat money will depreciate.

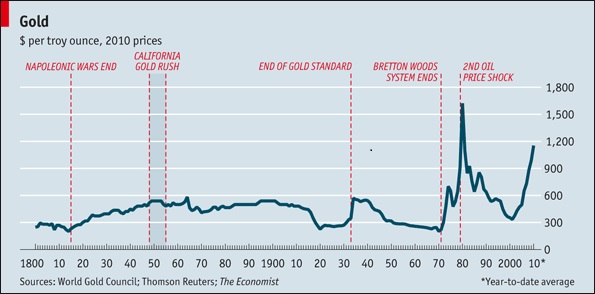

If the hedge demand for a former money commodity is large enough, resort to fiat money doesn’t save any resources at all. Indeed, as Roger Garrison notes, “a paper standard administered by an irresponsible monetary authority may drive the monetary value of gold so high that more resource costs are incurred under the paper standard than would have been incurred under a gold standard.” A glance at the history of gold’s real price suffices to show that this is precisely what has happened:

From “After the Gold Rush,” The Economist, July 6, 2010.

Taking the long-run average price of gold, in 2010 prices, to be somewhere around $470, prior to the closing of the gold window in 1917, that price was exceeded on only three occasions, and never dramatically: around the time of the California gold rush, around the turn of the 20th century, and for several years following FDR’s devaluation of the dollar. Since 1971, in contrast, it has exceeded that average, and exceeded it substantially, more often than not. Here is Roger Garrison again:

There is a certain asymmetry in the cost comparison that turns the resource-cost argument against paper standards. When an irresponsible monetary authority begins to overissue paper money, market participants begin to hoard gold, which stimulates the gold-mining industry and drives up the resource costs. But when new discoveries of gold are made, market participants do not begin to hoard paper or to set up printing presses for the issue of unbacked currency. Gold is a good substitute for an officially instituted paper money, but paper is not a good substitute for an officially recognized metallic money. Because of this asymmetry, the resource costs incurred by the State in its efforts to impose a paper standard on the economy and manage the supply of paper money could be avoided if the State would simply recognize gold as money. These costs, then, can be counted against the paper standard.

So if it’s avoidance of gold resource costs that’s desired, including avoidance of the very real environmental consequences of gold mining, a gold standard looks like the right way to go.

3. Gold supply “shocks” weren’t particularly shocking

Of the many misinformed criticisms of the gold standard, none seems to me more wrong-headed than the complaint that the gold standard isn’t even a reliable guarantee against serious inflation. The RationalWiki entry on the gold standard is as good an example of this as any:

Even gold can suffer problems with inflation. Gold rushes such as the California Gold Rush expanded the money supply and, when not matched with a simultaneous increase in economic output, caused inflation. The “Price Revolution” of the 16th century demonstrates a case of dramatic long-run inflation. During this period, western European nations used a bimetallic standard (gold and silver). The Price Revolution was the result of a huge influx of silver from central European mines starting during the late 15th century combined with a flood of new bullion from the Spanish treasure fleets and the demographic shift brought about by the Black Plague (i.e., depopulation).

Admittedly the anonymous authors of this article may not be professional economists; but take my word for it that the same arguments might be heard from any number of such professionals. Brad DeLong, for example, in a list of “Talking Points on the Likely Consequences of re-establishment of the Gold Standard” (my emphasis), includes observation that “significant advances in gold mining technology could provide a significant boost to the average rate of inflation over decades.”

Like I said, the gold standard is hardly free of defects. But being vulnerable to bouts of serious inflation isn’t one of them. Consider the “dramatic” 16th century inflation referred to in the RationalWiki entry. Had that entries’ authors referred to plain-old Wikipedia‘s entry on “Price revolution,” they would have read there that

Prices rose on average roughly sixfold over 150 years. This level of inflation amounts to 1-1.5% per year, a relatively low inflation rate for the 20th century standards, but rather high given the monetary policy in place in the 16th century.

I have no idea what the authors mean by their second statement, as there was certainly no such thing as “monetary policy” at the time, and they offer no further explanation or citation. So far as I can tell, they mean nothing more than that prices hadn’t been rising as fast before the price revolution than they did during it, which though trivially true says nothing about how “high” the inflation was by any standards, including those of the 16th century. In any case it was not only “not high” but dangerously low according to standards set, rightly or wrongly, by today’s monetary experts. Finally, though the point is often overlooked, the European Price Revolution actually began well in advance of major American specie shipments, which means that, far from being attributable to such shipments alone, it was a result of several causes, including coin debasements.

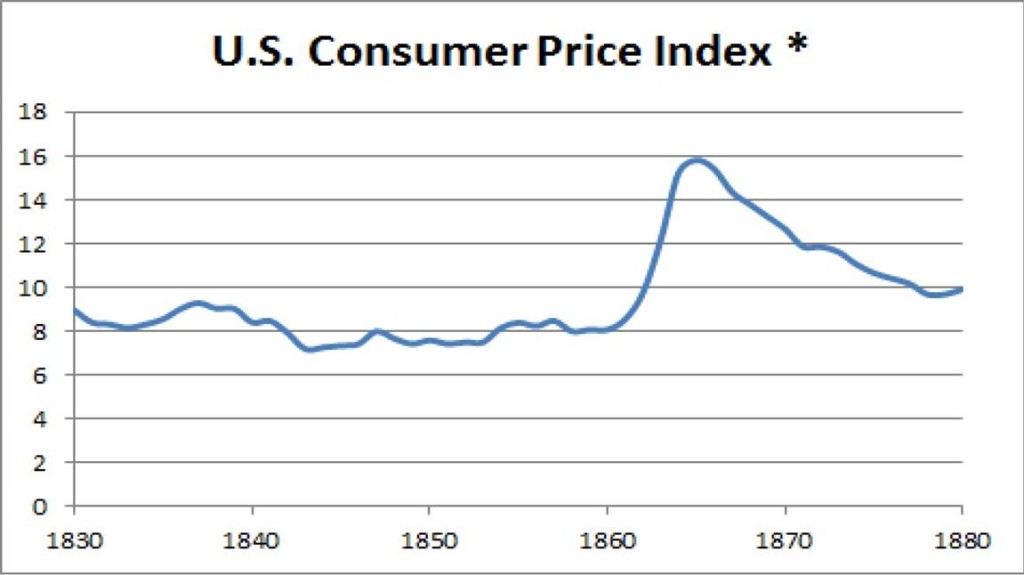

What about the California Gold rush, which is also supposed to show how changes in the supply of gold will lead to inflation “when not matched with a simultaneous increase in economic output”? To judge from available statistics, it appears that producers of other goods were almost a match for all those indefatigable forty-niners: as Larry White reports, although the U.S. GDP deflator did rise a bit in the years following the gold rush,

The magnitude was surprisingly small. Even over the most inflationary interval, the [GDP deflator] rose from 5.71 in 1849 (year 2000 = 100) to 6.42 in 1857, an increase of 12.4 percent spread over eight years. The compound annual price inflation rate over those eight years was slightly less than 1.5 percent.

Once again, the inflation rate was such as would have had today’s central banks rushing to expand their balance sheets.

Nor do the CPI estimates tell a different story. See if you can spot the gold-rush-induced inflation in this chart:

*Graphing Various Historical Economic Series,” MeasuringWorth, 2015.

Despite popular beliefs, the California gold rush was actually not the biggest 19th-century gold supply innovation, at least to judge from its bearing on the course of prices. That honor belongs instead to the Witwatersrand gold rush of 1886, the effects of which later combined with those of the Klondike rush of 1896 to end a long interval of gradual deflation (discussed further below) and begin one of gradual inflation.

Brad DeLong is thus quite right to refer to the South African discoveries in observing that even a gold standard poses some risk of inflation:

For example, the discovery and exploitation of large gold reserves near present-day Johannesburg at the end of the nineteenth century was responsible for a four percentage point per year shift in the worldwide rate of inflation–from a deflation of roughly two percent per year before 1896 to an inflation of roughly two percent per year after 1896.

Allowing for the general inaccuracy of 19th-century CPI estimates, DeLong’s statistics are correct. But that “For example” is quite misleading. Like I said: this is the most serious instance of an inflationary gold “supply shock” of which I’m aware. Yet even it served mainly to put an end to a deflationary trend, without ever giving rise to an inflation rate substantially above what central banks today consider (rightly or wrongly) optimal. As for the four percentage point change in the rate of inflation “per year,” presumably meaning “in one year,” it’s hardly remarkable: changes as big or larger are common throughout the 19th century, partly owing to the notoriously limited data on which CPI estimates for that era are based. Even so, they can’t be compared to the much larger jumps in inflation with which the history of fiat monies is riddled, even setting hyperinflations aside. Keep this in mind as you reflect upon Brad’s conclusion that

Under the gold standard, the average rate of inflation or deflation over decades ceases to be under the control of the government or the central bank, and becomes the result of the balance between growing world production and the pace of gold mining.

Alas, keeping matters in perspective–that is, comparing the gold standard’s actual inflation record, not to that which might be achieved by means of an ideally-managed fiat money, but to the actual inflation record of historic fiat-money systems, is something many critics of the gold standard seem reluctant to do, perhaps for good reason.

While we’re on the subject, nothing could be more absurd than attempts to demonstrate the unsuitability of gold as a monetary medium by referring to gold’s unstable real value in the years since the gold standard was abandoned. Yet this is a favorite debating point among the gold standard’s less thoughtful critics, including Paul Krugman:

There is a remarkably widespread view that at least gold has had stable purchasing power. But nothing could be further from the truth. Here’s the real price of gold — the price deflated by the consumer price index — since 1968:

Compare Professor Krugman’s chart to the one in the previous section. Then ask yourself (1) Has gold’s price behaved differently since 1968 than it did before?; and (2) Why might this be so? If your answers are “Yes” and “Because gold and paper dollars are no longer close substitutes, and gold is now widely used to hedge against depreciation of the dollar and other fiat currencies,” you understand the gold standard better than Krugman does. But don’t get a swelled head over it, because it really isn’t saying much: Krugman is one of the observations that sits squarely on the upper right end of y = α + β(x).

4. The deflation that the gold standard permitted wasn’t such a bad thing.

The complaint that a gold standard doesn’t rule out inflation is but a footnote to the more frequent complaint that it suffers, in Brad DeLong’s words, from “a deflationary bias which makes it likely that a gold standard regime will see a higher average unemployment rate than an alternative managed regime.” According to Ben Bernanke “There is…a high correlation in the data between deflation (falling prices) and depression (falling output).”

That the gold standard tended to be deflationary–or that it tended to be so for sometimes long intervals between gold discoveries–can’t be denied. But what certainly can be denied is that these periods of slow deflation went hand-in-hand with high unemployment. Having thoroughly reviewed the empirical record, Andrew Atkeson and Patrick Kehoe conclude as follows:

Deflation and depression do seem to have been linked during the1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

More recently Claudio Borio and several of his BIS colleagues reported similar findings. How then (you may wonder), did Bernanke arrive at his opposite conclusion? Easy: he looked only at data for the 1930s–the worst deflationary crisis ever–ignoring all the rest.

Why is deflation sometimes depressing, and sometimes not? The simple answer is that there is more than one sort of deflation. There’s the sort that’s caused by a collapse of spending, like the “Great Contraction” of the 1930s, and then there’s the sort that’s driven by greater output of real goods and services–that is, by outward shifts in aggregate supply rather than inward shifts in aggregate demand. Most of the deflation that occurred during the classical gold standard era (1873-1914) was of the latter, “good” sort.

Although I’ve been banging the drum for good deflation since the 1990s, and Mike Bordo and others have made the specific point that the gold standard mostly involved inflation of the good rather than bad sort, too many economists, and way too many of those who have got more than their fare share of the public’s attention, continue to ignore the very possibility of supply-driven deflation.

Of the many misunderstandings propagated by economists’ tendency to assume that deflation and depression must go hand-in-hand, none has been more pernicious than the widespread belief that throughout the U.S. and Europe, the entire period from 1873 to 1896 constituted one “Great” or “Long Depression .” That belief is now largely discredited, except perhaps among some newspaper pundits and die-hard Marxists, thanks to the efforts of G.B. Saul and others. The myth of a somewhat shorter “Long Depression,” lasting from 1873-1879, persists, however, though economic historians have begun chipping away at that one as well.

5. It wasn’t to blame for 19th-century American financial crises.

Speaking of 1873, after claiming that a gold standard is undesirable because it makes deflation (and therefore, according to his reasoning, depression) more likely, Krugman observes:

The gold bugs will no doubt reply that under a gold standard big bubbles couldn’t happen, and therefore there wouldn’t be major financial crises. And it’s true: under the gold standard America had no major financial panics other than in 1873, 1884, 1890, 1893, 1907, 1930, 1931, 1932, and 1933. Oh, wait.

Let me see if I understand this. If financial crises happen under base-money regime X, then that regime must be the cause of the crises, and is therefore best avoided. So if crises happen under a fiat money regime, I guess we’d better stay away from fiat money. Oh, wait.

You get the point: while the nature of an economy’s monetary standard may have some bearing on the frequency of its financial crises, it hardly follows that that frequency depends mainly on its monetary standard rather than on other factors, like the structure, industrial and regulatory, of the financial system.

That U.S. financial crises during the gold standard era had more to do with U.S. financial regulations than with the workings of the gold standard itself is recognized by all competent financial historians. The lack of branch banking made U.S. banks uniquely vulnerable to shocks, while Civil-War rules linked the supply of banknotes to the extent of the Federal government’s indebtedness., instead of allowing that supply to adjust with seasonal and cyclical needs. But there’s no need to delve into the precise ways in which such misguided legal restrictions to the umerous crises to which Krugman refers. It should suffice to point out that Canada, which employed the very same gold dollar, depended heavily on exports to the U.S., and (owing to its much smaller size) was far less diversified, endured no banking crises at all, and very few bank failures, between 1870 and 1939.

6. 0n the whole, the classical gold standard worked remarkably well (while it lasted).

Since Keynes’s reference to gold as a “barbarous relic” is so often quoted by the gold standard’s critics, it seems only fair to repeat what Keynes had to say, a few years before, not about gold per se, itself, but about the gold-standard era:

What an extraordinary episode in the economic progress of man that age was which came to an end in August, 1914! The greater part of the population, it is true, worked hard and lived at a low standard of comfort, yet were, to all appearances, reasonably contented with this lot. But escape was possible, for any man of capacity or character at all exceeding the average, into the middle and upper classes, for whom life offered, at a low cost and with the least trouble, conveniences, comforts, and amenities beyond the compass of the richest and most powerful monarchs of other ages. The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages… He could secure forthwith, if he wished it, cheap and comfortable means of transit to any country or climate without passport or other formality, could despatch his servant to the neighboring office of a bank or such supply of the precious metals as might seem convenient, and could then proceed abroad to foreign quarters, without knowledge of their religion, language, or customs, bearing coined wealth upon his person, and would consider himself greatly aggrieved and much surprised at the least interference. But, most important of all, he regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable.

It would, of course, be foolish to suggest that the gold standard was entirely or even largely responsible for this Arcadia, such as it was. But it certainly did contribute both to the general abundance of goods of all sorts, to the ease with which goods and capital flowed from nation to nation, and, especially, to the sense of a state of affairs that was “normal, certain, and permanent.”

The gold standard achieved these things mainly by securing a degree of price-level and exchange rate stability and predictability that has never been matched since. According to Finn Kydland and Mark Wynne:

The contrast between the price stability that prevailed in most countries under the gold standard and the instability under fiat standards is striking. This reflects the fact that under commodity standards (such as the gold standard), increases in the price level (which were frequently associated with wars) tended to be reversed, resulting in a price level that was stable over long periods. No such tendency is apparent under the fiat standards that most countries have followed since the breakdown of the gold standard between World War I and World War II.

The high degree of price level predictability, together with the system of fixed exchange rates that was incidental to the gold standard’s widespread adoption, substantially reduced the riskiness of both production and international trade, while the commitment to maintain the standard resulted, as I noted, in considerably lower international borrowing costs.

Those pundits who find it easy to say “good riddance” to the gold standard, in either its classical or its decadent variants, need to ask themselves what all the fuss over monetary “reconstruction” was about, following each of the world wars, if not achieving a simulacrum at least of the stability that the classical gold standard achieved. True, those efforts all failed. But that hardly means that the ends sought weren’t very worthwhile ones, or that those who sought them were “lulled by the myth of a golden age.” Though they may have entertained wrong beliefs concerning how the old system worked, they weren’t wrong in believing that it did work, somehow.

7. It didn’t have to be managed by central bankers.

But how? The once common view that the classical gold standard worked well only thanks to its having been carefully managed by the Bank of England and other central banks, as well as the related view that its success depended on international agreements and other forms of central bank cooperation, is now, thankfully, no longer subscribed to even by the gold-standard’s more well-informed critics. Instead, as Julio Gallarotti observes, the outcomes of that standard “were primarily the resultants [sic] of private transactions in the markets for goods and money” rather than of any sort of government or central-bank management or intervention. But the now accepted view doesn’t quite go far enough. In fact, central banks played no essential part at all in achieving the gold standard’s most desirable outcomes, which could have been achieved as well, or better, by systems of competing banks-of-issue, and which were in fact achieved by means of such systems in many participating nations, including the United States, Switzerland (until 1901), and Canada. And although it is common for central banking advocates to portray such banks as sources of emergency liquidity to private banks, during the classical gold standard era liquidity assistance often flowed the other way, and did so notwithstanding monopoly privileges that gave central banks so many advantages over their commercial counterparts. As Gallarotti observes (p. 81),

That central banks sometimes went to other central banks instead of the private market suggests nothing more than the fact that the rates offered by central banks were better, or too great an amount of liquidity may have been needed to be covered in the private market.

8. In fact, central banking tends to throw a wrench in the works.

To the extent that central banks did exercise any special influence on gold-standard era monetary adjustments, that influence, instead of helping, made things worse. Because an expanding central bank isn’t subject to the internal constraint of reserve losses stemming from adverse interbank clearings, it can create an external imbalance that must eventually trigger a disruptive drain of specie reserves. During liquidity crunches, on the other hand, central banks were more likely than commercial banks to become, in Jacob Viner’s words, “engaged in competitive increases of their discount rates and in raid’s on each other’s reserves.” Finally, central banks could and did muck-up the gold standard works by sterilizing gold inflows and outflows, violating the “rules of the gold standard game” that called for loosening in response to gold receipts and tightening in response to gold losses.

Competing banks of issue could be expected to play by these “rules,” because doing so was consistent with profit maximization. The semi-public status of central banks, on the other hand, confronted them with a sort of dual mandate, in which profits had to be weighed against other, “public” responsibilities (ibid., pp. 117ff.). Of the latter, the most pernicious was the perceived obligation to occasionally set aside the requirements for preserving international monetary equilibrium (“external balance”) for the sake of preserving or achieving preferred domestic monetary conditions (“internal balance”). As Barry Ickes observes, playing by the gold standards rules could be “very unpopular, potentially, as it involves sacrificing internal balance for external balance.” Commercial bankers couldn’t care less. Central bankers, on the other hand, had to care when to not care was to risk losing some of their privileges.

Today, of course, achieving internal balance is generally considered the sine qua non of sound central bank practice; and even where fixed or at least stable exchange rates are considered desirable it is taken for granted that external balance ought occasionally to be sacrificed for the sake of preserving domestic monetary stability. But to apply such thinking to the classical gold standard, and thereby conclude that in that context a similar sacrifice of external for internal stability represented a turn toward more enlightened monetary policy, is to badly misunderstand the nature of that arrangement, which was not just a fixed exchange rate arrangement but something more akin to an multinational monetary union or currency area. Within such an area, the fact that one central bank gains reserves while another looses them was itself no more significant, and no more a justification for violating the “rules of the game,” than the fact that a commercial bank somewhere gained reserves at the expense of another.

The presence of central banks did, however, tend to aggravate the disturbing effects of changes in international trade patterns compared to the case of international free banking. Central-bank sterilization of gold flows could, on the other hand, lead to more severe longer-run adjustments, as it was to do, to a far more dramatic extent, in the interwar period.

9. “The “Gold Standard” wasn’t to blame for the Great Depression.

I know I’m about to skate onto thin ice, so let me be more precise. To say that “The gold standard caused the Great Depression ” (or words to that effect, like “the gold standard was itself the principal threat to financial stability and economic prosperity between the wars”), is at best extremely misleading. The more accurate claim is that the Great Depression was triggered by the collapse of the jury-rigged version of the gold standard cobbled together after World War I, which was really a hodge-podge of genuine, gold-exchange, and gold-bullion versions of the gold standard, the last two of which were supposed to “economize” on gold. Call it “gold standard light.”

Admittedly there is one sense in which the real gold standard can be said to have contributed to the disastrous shenanigans of the 1920s, and hence to the depression that followed. It contributed by failing to survive the outbreak of World War I. The prewar gold standard thus played the part of Humpty Dumpty to the King’s and Queen’s men who were to piece the still-more-fragile postwar arrangement together. Yet even this is being a bit unfair to gold, for the fragility of the gold standard on the eve of World War I was itself largely due to the fact that, in most of the belligerent nations, it had come to be administered by central banks that were all-too easily dragooned by their sponsoring governments into serving as instruments of wartime inflationary finance.

Kydland and Wynne offer the case of the Bank of Sweden as illustrating the practical impossibility of preserving a gold standard in the face of a major shock:

During the period in which Sweden adhered to the gold standard (1873–1914), the Swedish constitution guaranteed the convertibility into gold of banknotes issued by the Bank of Sweden. Furthermore, laws pertaining to the gold standard could only be changed by two identical decisions of the Swedish Parliament, with an election in between. Nevertheless, when World War I broke out, the Bank of Sweden unilaterally decided to make its notes inconvertible. The constitutionality of this step was never challenged, thus ending the gold standard era in Sweden.

The episode seems rather less surprising, however, when one considers that “the Bank of Sweden,” which secured a monopoly of Swedish paper currency in 1901, is more accurately known as the Sveriges Riksbank, or “Bank of the Swedish Parliament.”

If the world crisis of the 1930s was triggered by the failure, not of the classical gold standard, but of a hybrid arrangement, can it not be said that the U.S. , which was among the few nations that retained a full-fledged gold standard, was fated by that decision to suffer a particularly severe downturn? According to Brad DeLong,

Commitment to the gold standard prevented Federal Reserve action to expand the money supply in 1930 and 1931–and forced President Hoover into destructive attempts at budget-balancing in order to avoid a gold standard-generated run on the dollar.

It’s true that Hoover tried to balance the Federal budget, and that his attempt to do so had all sorts of unfortunate consequences. But the gold standard, far from forcing his hand, had little to do with it. Hoover simply subscribed to the prevailing orthodoxy favoring a balanced budget. So, for that matter, did FDR, until events forced him too change his tune: during the 1932 presidential campaign the New-Dealer-to-be assailed his opponent both for running a deficit and for his government’s excessive spending.

As for the gold standard’s having prevented the Fed from expanding the money supply (or, more precisely, from expanding the monetary base to keep the broader money supply from shrinking), nothing could be further from the truth. Dick Timberlake sets the record straight:

By August 1931, Fed gold had reached $3.5 billion (from $3.1 billion in 1929), an amount that was 81 percent of outstanding Fed monetary obligations and more than double the reserves required by the Federal Reserve Act. Even in March 1933 at the nadir of the monetary contraction, Federal Reserve Banks had more than $1 billion of excess gold reserves.

Moreover,

Whether Fed Banks had excess gold reserves or not, all of the Fed Banks’ gold holdings were expendable in a crisis. The Federal Reserve Board had statutory authority to suspend all gold reserve requirements for Fed Banks for an indefinite period.

Nor, according to a statistical study by Chang-Tai Hsieh and Christina Romer, did the Fed have reason to fear that by allowing its reserves to decline it would have raised fears of a devaluation. On the contrary: by taking steps to avoid a monetary contraction, the Fed would have helped to allay fears of a devaluation, while, in Timberlake’s words, initiating a “spending dynamic” that would have helped to restore “all the monetary vitals both in the United States and the rest of the world.”

10. It didn’t manage money according to any economists’ theoretical ideal. But neither has any fiat-money-issuing central bank.

Just as “paper” always beats “rock” in the rock-paper-scissors game, so does managed paper money always beat gold in the rock-paper monetary standards game economists like to play. But that’s only because under a fiat standard any pattern of money supply adjustment is possible, including a “perfect” pattern, where “perfect” means perfect according to the player’s own understanding. Even under the best of circumstances a gold standard is, on the other hand, unlikely to achieve any economist’s ideal of monetary perfection. Hence, paper beats rock. More precisely, paper beats rock, on paper.

And what does this impeccable logic tell us concerning the relative merits of gold versus paper money in practice? Diddly-squat. I mean it. To say something about the relative merits of paper and gold, you have to have theories–good ol’ fashioned, rational optimizing firm and agent theories–of how the supply of basic money adjusts under various conditions in the two sorts of monetary regimes. We have a pretty good theory of the gold standard, meaning one that meshes well with how that standard actually worked. The theory of fiat money is, in contrast, a joke, in part because it’s much harder to pin-down central bankers’ objectives (or any objectives apart from profit-maximization, which is at play in the case of gold), but mostly thanks to economists’ tendency to simply assume that central bankers behave like omniscient angels who, among other things, understand the finer points of DSGE models. That may do for a graduate class, or a paper in the AER. But good economics it most certainly isn’t.

***

I close with a few words concerning why it matters that we get the facts straight about the gold standard. It isn’t simply a matter of winning people over to that standard. Though I’m perhaps as ready as anyone to shed a tear for the old gold standard, I doubt that we can ever again create anything like it. But getting a proper grip on gold serves, not just to make the gold standard seem less unattractive than it is often portrayed to be, but to remove some of the sheen that has been applied to modern fiat-money arrangements using the same brush by which gold has been blackened. The point, in other words, isn’t to make a pitch for gold. It’s to make a pitch for something –anything– that’s better than our present, lousy money.

*I’m astonished to find that Friedman’s important and very interesting 1986 article, despite appearing in one of the leading academic journals, has to date been cited only 64 times (Google Scholar). Of these, nine are in works by myself, Kevin Dowd, and Lawrence White! I only wish I could attribute this neglect to monetary economists’ pro-fiat money bias. More likely it reflects their general lack of interest in alternative monetary arrangements.