AIER founder Col. E.C. Harwood believed that business cycles matter and should be taken into account when making personal financial plans. He wrote his classic, “Cause and Control of the Business Cycle,” (https://www.aier.org/sites/default/files/Documents/Research/pdf/eeb197409.pdf) published in 1932, to help people understand their significance.

READ MORE

With the backdrop of mixed economic signals in recent weeks, two reports this week suggest some good news for U.S. consumers.

READ MORE

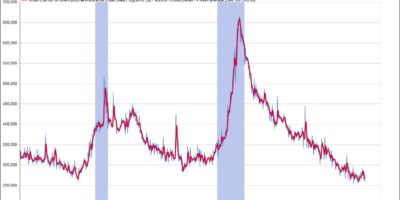

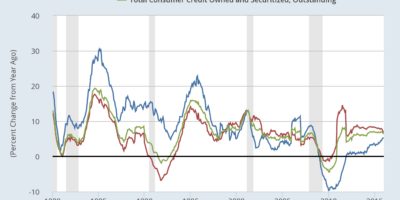

Consumers continued to add debt to their balance sheets in January, according to data released by the Federal Reserve on Monday.

READ MORE

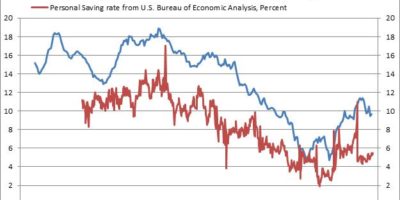

When it comes to personal savings, Americans are doing better than many people think. But there’s still a lot of room for improvement, especially when you look at it in a historical context.

READ MOREThe U.S. economy has struggled with inconsistent performance for much of the current expansion, which began halfway through 2009. That inconsistency reared up again in the last three months of 2015. The initial estimate for gross domestic product, or GDP, the broadest measure of economic activity, shows that growth slowed in that period. Future revisions based on more complete data may show a different picture, but the first take puts real GDP rising at a meager 0.7 percent annual rate compared with a 2 percent pace in the third quarter and 3.9 percent in the second.

READ MORE

Wages – average hourly earnings – rose a decent 0.3 percent in January for production and nonsupervisory workers, and an even more impressive 0.5 percent for all workers. Both are up 2.5 percent from a year ago, about as strong a gain as we’ve seen in the current expansion, but well below the peak rates of about 4 percent per year in prior expansions. But that’s only part of the story.

READ MORE

Although the economy and the stock market are very different entities, they can and do intersect. Their health rely on some of the same fundamentals. Short-term stock market fluctuations, including the recent double-digit percentage plunge, are difficult to fully explain and even more difficult to predict. However, over time, equity markets tend to be driven by fundamentals – sales, margins, and earnings.

READ MOREU.S. consumers are supporting growth, while credit tightening at the Federal Reserve and moderate economic expansion in the U.S. contrast with a sluggish global economy and generally stimulative central bank policies. Dollar strength and commodity weakness continue. Despite a roughly flat year for the broader market, commodity-related equities sharply underperformed the S&P 500 Index. Looking ahead, interest rates are likely to rise slowly, while the risk of recession remains relatively low.

READ MORE

A strong December payroll gain plus upward revisions to November and October suggest the economy is entering 2016 with good momentum.

READ MORE

This institute has long been known for its work in identifying turning points in the economy, including predicting recessions. And we have a pretty good track record in that regard since we started studying business cycles in 1953. But such work requires vigilance, and changing with the times as necessary.

READ MORE

Despite some risks, the U.S. economic outlook for 2016 appears favorable. Overview The Economy… Despite some risks, the U.S. economic outlook for next year appears favorable. Consumer fundamentals continue to improve while household and corporate balance sheets are generally healthy. However, the prospect of rising interest rates poses a risk. Fed policy makers have indicated a gradual path is likely for future rate increases, suggesting a keen awareness of the risks to growth from overly aggressive tightening. Global economic expansion is also a concern. While the U.S. depends less on exports than many other nations, the combination of slow growth and a strong dollar weighs on some sectors. Our Leader’s index rose to 56 in the latest month from 50 in the prior month. Combined with our cyclical score of 70, we see the probability of recession in the next six to twelve months as relatively low. …Inflation… The CPI rose in October after falling in the previous two months, helped by a slight increase in energy prices. The latest AIER Inflationary Pressures Scorecard points to a neutral reading, with 10 indicators supporting rising inflationary pressure and 11 suggesting pressure is falling. Two are stable. The major change this month came from wages and productivity. Rising private compensation levels and higher labor costs, along with lower growth in productivity, put upward pressure on inflation. But this was offset by a decrease in other producer costs. Overall, there is no evidence that inflation will change significantly in either direction in the coming months. …Policy… The Fed is expected to raise its target for the overnight lending rate between banks by a small amount this month, the first increase in almost a decade. Since this move is widely anticipated, it is unlikely to have significant economic effect. At the same time, legislation pending before Congress would impose a new requirement that the Fed publicly disclose its interest-rate strategy and its reasons for any deviations. The bill, which has passed the House and is unlikely to pass the Senate, raised objections from the Fed, which is worried about its independence. …Investing With bond yields near 60-year lows, it’s difficult to justify expected total returns in the high single-digit range, as we have seen since 1982 for this asset class. Investors should carefully review asset allocations and be prudent in estimating future gains. U.S. equities have struggled this year as the effects of falling commodity prices and slow global growth weigh on the economy and earnings for some sectors. However, earnings are expected to rebound in 2016. Valuations remain close to the long-term average, especially given the low inflation environment. Overall, that suggests a neutral to slightly positive outlook for stocks. Investors may look to maximize exposure to domestic sources of growth such as consumer spending and capital investment outside of commodity-related industries.

READ MORE

Today’s retail sales report from the Commerce Department contained more good signs for the holiday shopping season, as consumers focus on small-ticket items.

READ MORE