Pulling It All Together/Appendix

The Economy…

The strengthening dollar threatens to reduce U.S. economic growth by spurring imports and curbing exports, widening the trade deficit and crimping GDP expansion. However, net international trade, exports minus imports, is a relatively small share of the nation’s economy, so the threat to growth is relatively small as well.

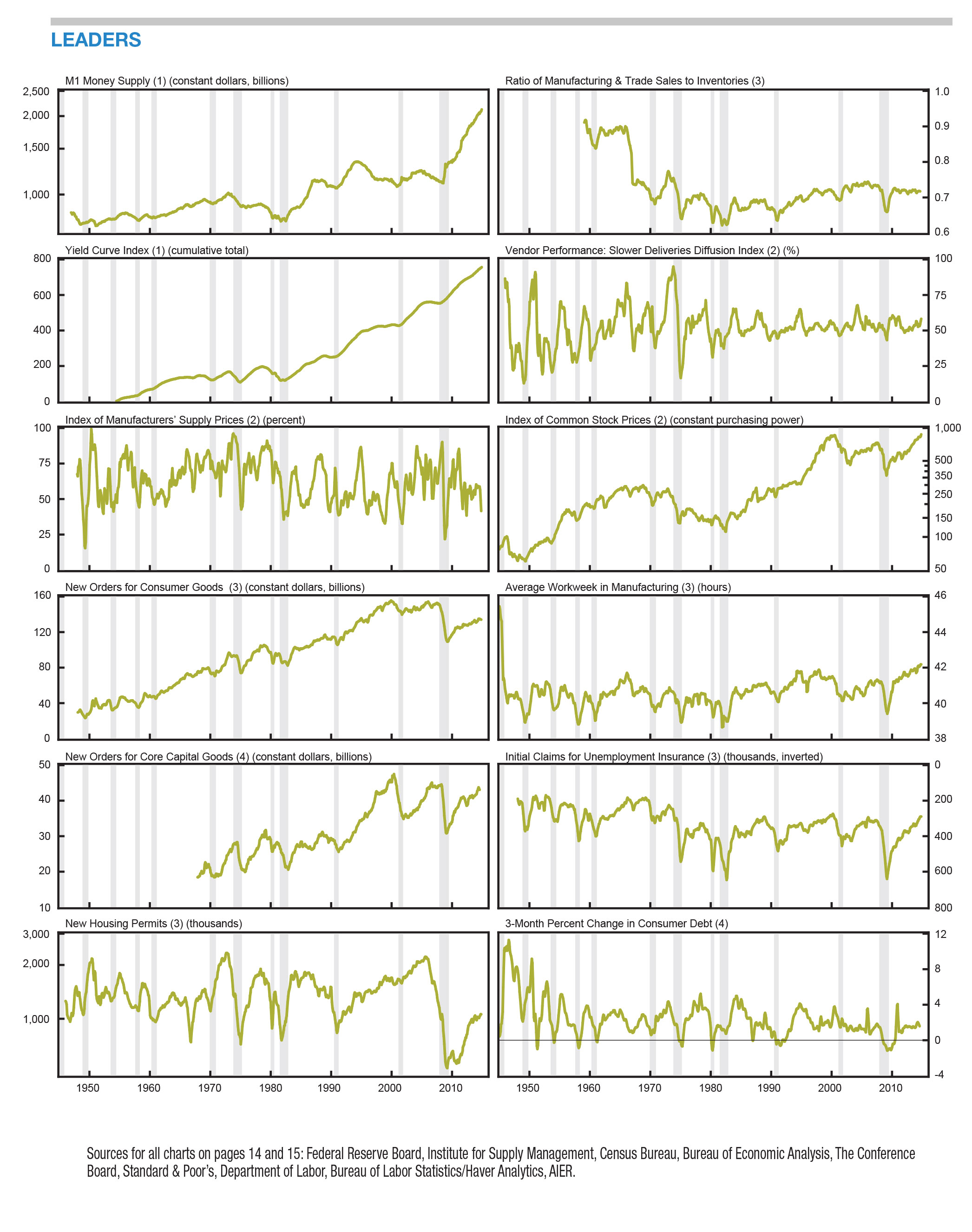

The AIER leading indicators index pulled back in January for a second straight month, consistent with a widening soft patch for U.S. growth. However, at a reading of 67, the index remains solidly above the neutral level of 50, suggesting that continued growth is likely.

…Inflation…

In general, a rising dollar is a positive for U.S. consumer prices. A strong dollar lowers the cost of imports, restraining CPI gains while also increasing pressure on American producers of goods that compete with lower-priced imports.

The AIER inflationary pressures scorecard was more balanced in the latest reading as two indicators shifted from falling to rising, resulting in a more closely balanced score of 9 rising to 12 falling and two remaining stable. The key changes came in personal income, which changed to rising from falling, reflecting improvements in the labor market. The second indicator that moved to rising from falling, the producer price index for services, rose to a 3.0 percent annualized growth rate for the three months through December, from a 1.9 percent rate in the previous three months.

…Washington…

While cheaper imports may ratchet up pressure on competing domestic producers, historical data suggests actual job losses as a result of import competition in recent years have been relatively small. Because of changes in economic circumstances, slower global growth and more limited options for the federal government than during the 1990s boom in the dollar, whatever pressure may emerge for changes in policy is likely to have little effect. Besides, a government program designed to help displaced workers is already in place.

…Investing

A stronger dollar can lead to higher commodity prices in other currencies in the short run, followed by weaker demand, slower growth, and ultimately lower prices overall in the longer run.

A stronger dollar can lead to higher commodity prices in other currencies in the short run, followed by weaker demand, slower growth, and ultimately lower prices overall in the longer run.

One increasing risk in fixed-income markets may be the sizable amount of foreign-issued dollar-denominated debt. As the U.S. currency appreciates, it becomes more expensive to service these debts with weakening currencies. The resulting amplified risk levels may affect both sovereign debt issued by foreign governments and corporate debt sold by companies whose earnings are largely derived from sales in markets with weakening currencies.

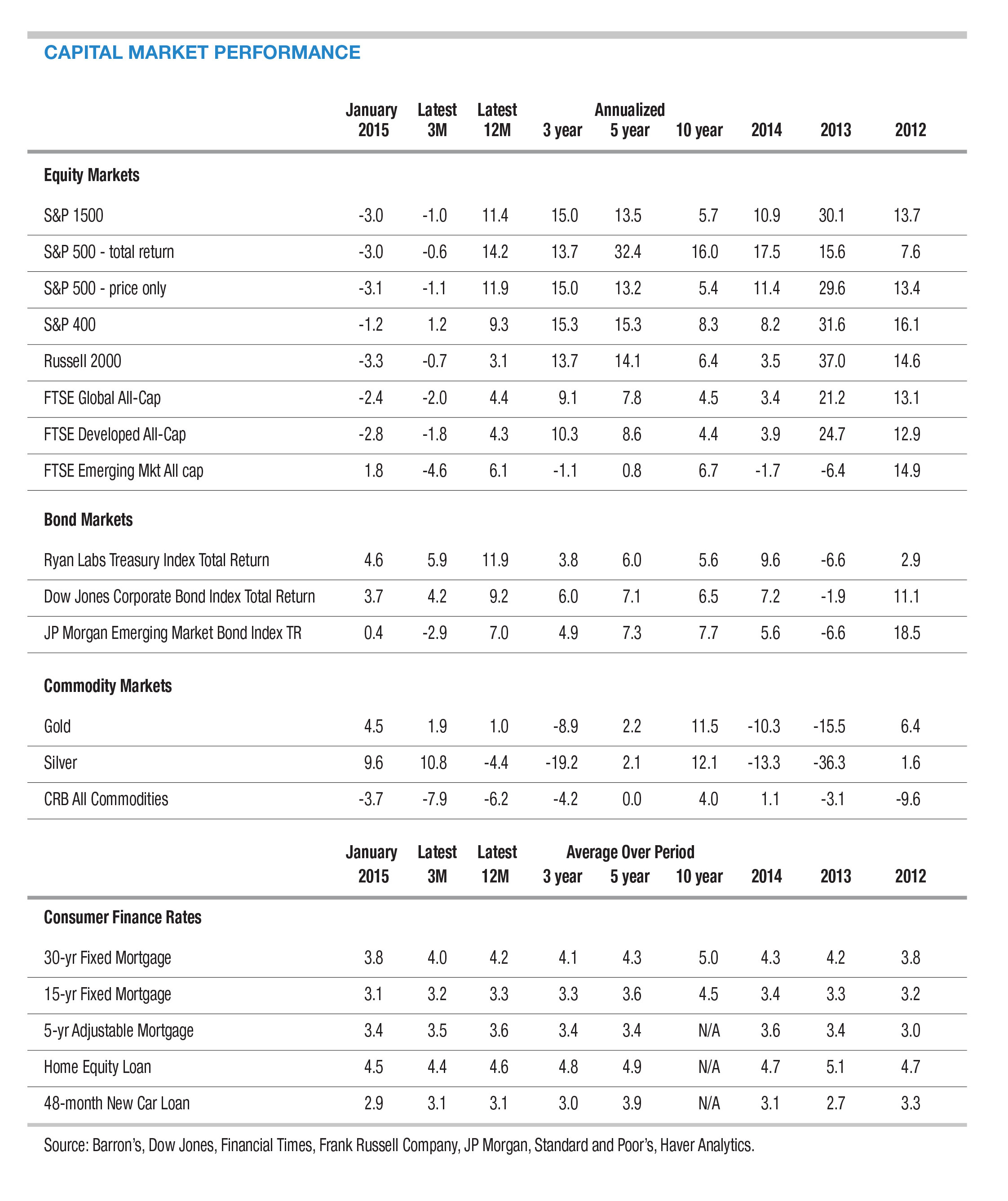

Equity market risks to American investors from a strengthening dollar come in two forms: U.S. companies that generate substantial portions of earnings in foreign currencies may see the value of those earnings erode, while holders of foreign equities may see their investments decline in value. Hedging these portfolios against the effects of a continued rise in the dollar can mitigate some of the damage, as shown by returns from a hedged index of global shares compared with an unhedged version.