Investing

Fixed Income

Government bonds continue to be a safe haven for many investors. Following the surprise results of the Brexit vote, equities sold off and money flooded into government bonds around the world, driving prices up and yields down.

German, euro, and Swiss 10-year bonds are all trading at negative yields, joining Japan, whose bond yields have been below zero since early 2016. It is interesting that the initial move for Italian and Spanish bond yields was higher immediately after the vote but then fell, along with other bond yields (Chart 6).

In the U.S., the benchmark bond yield fell sharply, coming close to multi-decade lows. Corporate bond yields also fell but not by as much as Treasury bonds (Chart 7), leaving spreads slightly wider than before the vote. In a yield-starved world, U.S. Treasury and corporate bond yields look attractive compared with other fixed-income investments.

Commodities

Government bonds may be the place investors turn for safety from equity-market volatility. But during times when political upheaval is at hand or inflation is a threat or risks to the entire financial system appear to be growing, investors have turned to the safety of gold. Over the past five decades, gold has gone through long, strong rallies and long periods of decline. Following the global financial crisis at the turn of the decade, gold rose to a high of around $1,900 an ounce. As fears of financial collapse and runaway inflation from quantitative easing began to slacken, gold fell to a low of under $1,100 an ounce by the end of 2015 (Chart 8).

In early 2016, gold began a new move higher and extended that run in the days following the Brexit vote (Chart 8 inset). No one can know whether the crisis in Europe will turn into a global economic and financial crisis or become a long, drawn-out, largely political quagmire, but gold can play a role in some investment portfolios as a hedge against unfavorable and unexpected developments.

U.S. Equities

The six trading days after the Brexit vote showed just how fickle markets can be. U.S. equity markets plunged in the two days following the vote and then rallied, recovering nearly the entire drop. Certainly, economic and profit prospects didn’t fluctuate as dramatically over that six-day period.

For U.S. equity markets, the challenging economic and profit backdrop has slowed price appreciation to a crawl. Major benchmarks have essentially moved sideways since the second quarter of 2015, with significant declines and rebounds in the third quarter of 2015 and first quarter of 2016.

For the current calendar year, U.S. large-cap stocks are trailing the mid- and small-cap indexes. Following the Brexit vote, all three indexes fell sharply for two days but quickly recovered most of the declines over the next four days (Chart 9).

Slow economic growth—domestic and global—is a difficult environment for profit growth, the key long-term driver of equity prices. The collapse in crude-oil prices has hurt the U.S. energy industry as well as the capital-goods companies that supply equipment to the energy industry. The combination of slow global growth and a strong dollar has hurt U.S. exports. All of these have combined to pull profits lower. Furthermore, the tightening labor market has the potential to push wage increases up more quickly and eventually could squeeze profit margins.

Despite these potential risks, U.S. equities compare favorably with most other global equity markets and with U.S. bonds. U.S. consumers, whose spending accounts for about 70 percent of U.S. GDP, are in relatively good financial shape. The tight labor market may push income up at a faster pace, supporting future gains in consumer spending.

Global Equities

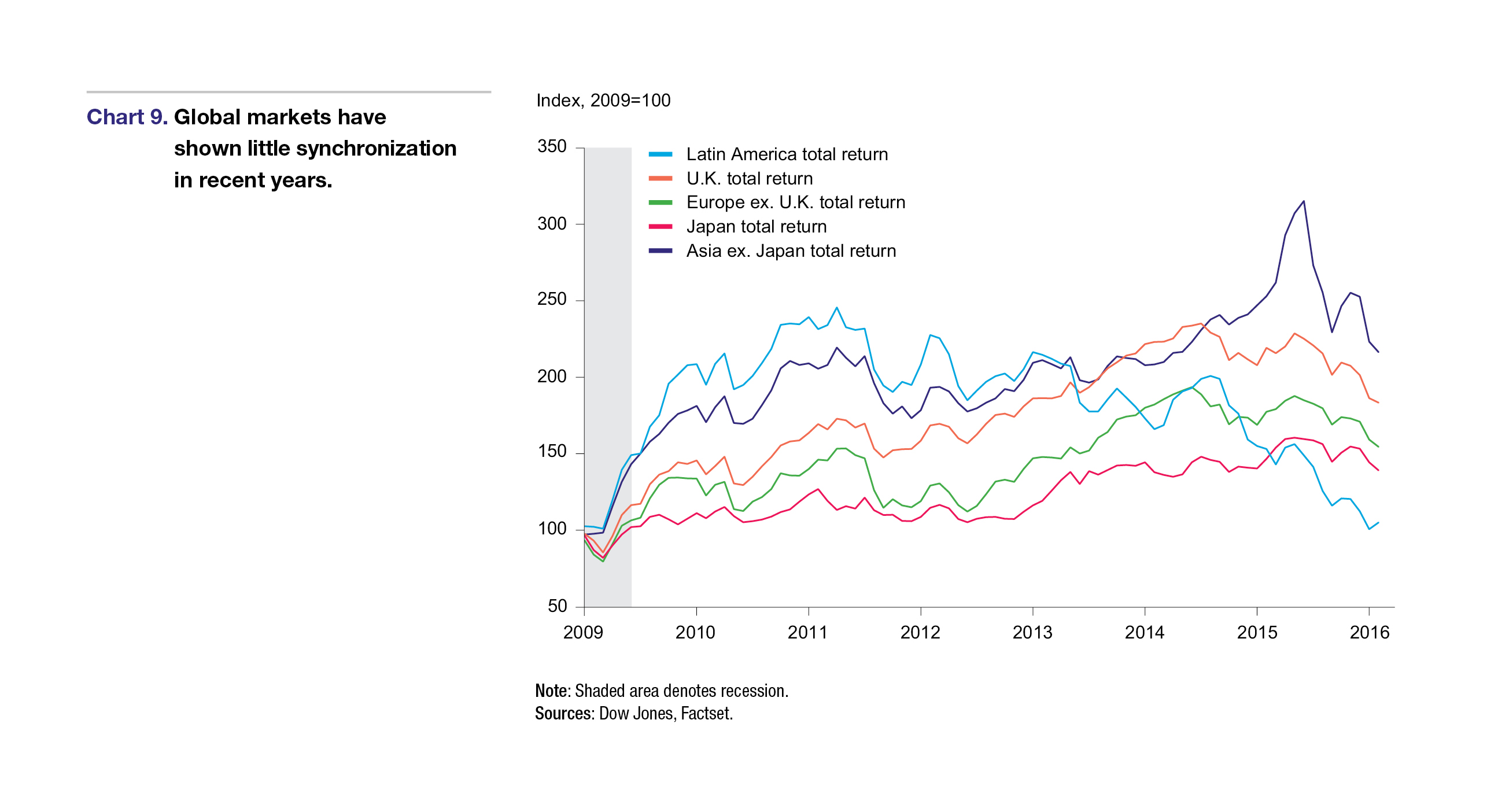

If the performance of the major U.S. equity market indexes has been less than impressive, then the performance of many of the world’s other major equity market indexes has been outright disappointing. Declines in global equity markets were seemingly universal in the days following the Brexit vote. Most of the major markets managed a rebound of some magnitude, however (Chart 10).

Like the U.S., many of the world’s economies and equity markets are struggling to produce sustained economic and corporate profit growth. Europe continues to delay decisive action on the banking problems of some member nations. Government fiscal positions are tenuous in a few nations, and labor market rigidities plague several countries. Recent political issues including immigration and the Brexit vote are adding to the list of difficult issues.

In Japan economic growth has been weak for years under the weight of unfavorable demographic trends and a strong yen. China is experiencing a significant slowdown in economic growth while attempting to move to a more consumption- oriented economy, develop a strong middle class, and transition its economy to more free-market principles.

Among emerging markets, the collapse in commodity prices has been detrimental to growth. Political instability continues in some places (Brazil). All in all, global prospects seem particularly challenging across the spectrum. However, a time when the outlook appears bleakest is when the best value opportunities can be found.

Next/Previous Section:

1.Overview

2. Economy

3. Inflation

4. Policy

5. Investing

6. Pulling It All Together/Appendix