Investing

Fixed Income

Like the economy in general, the U.S. Treasury market is in the midst of strong crosscurrents. Domestically, Fed policy tightening should be putting upward pressure on yields, particularly on the short end of the yield curve. Tighter Fed policy would be consistent with improving economic conditions. However, the recent run of conflicting economic data may be offsetting the upward policy pressure.

From a risk perspective, Treasurys are a safe haven in times of turbulence. In that regard, volatility in equity markets should lead to some marginal government-bond buying. Offsetting that may be the difficult economic conditions for two of the largest global holders of Treasury securities, China and Japan.

International buying of Treasury bonds has fallen dramatically over the past year (Chart 6). Both China and Japan have now become net sellers of Treasurys.

The bottom line is that while no one can predict markets with great precision, economic theory would suggest that at some point, better economic conditions, firming inflation expectations, and additional policy tightening should lead to higher yields.

Commodities

Holding gold and gold mining stocks has long been part of the investment philosophy at AIER. While plenty of experts disparage the precious metal as a portfolio investment, AIER views it as a viable option worthy of consideration.

Among the criticisms of gold is that the metal itself does not produce an income stream. Also, as an asset, its risk-to-return profile may not compare favorably with other assets, depending on how that profile is calculated.

On the positive side, gold and gold mining stocks tend to move in the opposite direction as other types of assets—described as a low price correlation—so over time, they can reduce portfolio volatility (Chart 7).

The role of gold can become more important in times of global instability, when inflation becomes a serious threat, or when systemic risks and threats to all financial markets rise. This was the case in the past when AIER strongly advocated for holding gold.

There are two key messages here. First, each investor has unique goals and circumstances, so the decision to include gold in a portfolio should be made on an individual basis. Gold can play a critical and helpful role for some investors. For investors who are particularly concerned about overall portfolio volatility, using gold to help reduce price swings makes sense.

Second, including gold in a portfolio, and how much, depends on economic conditions. Col. Harwood brilliantly foresaw the various periods of the deterioration of money, weakness in the banking system, poor policy, and the ups and downs of business cycles, and he guided his adherents through them. We at AIER continue to strive to live up to those high standards.

Click here to receive email notifications when the latest Business Conditions Monthly is available.

U.S. Equities

Our focus on the domestic economy has centered on core growth – private consumption and investment. Our analysis suggests that fundamentals for consumer spending and most parts of private investment remain generally healthy. We expect solid core economic growth in the U.S. to offset weak global growth, a strong dollar, and the negative effects of falling commodity prices on certain industries.

That analysis would appear to be justified by the performance of one stock sector, U.S. consumer discretionary stocks. If stocks are a forward-looking discount mechanism, meaning that their prices reflect the outlook for future earnings, then as forward expectations for this sector improve at a more robust pace than the broader market, consumer discretionary stocks should outperform the broader market.

In fact, since the market low on March 9, 2009, consumer discretionary stocks in all three market-cap segments—large-, mid-, and small-cap—have outperformed their broader benchmarks. It is interesting that the weakest performance among consumer discretionary segments came from mid-cap consumer discretionary stocks, yet this group still beat the best-performing broad index, the small-cap Standard & Poor’s 600 (Chart 8).

The risk, of course, is if and when future expectations become too high for these stocks to meet. Unrealistic expectations are a phenomenon that AIER has warned about throughout its history.

Global Equities

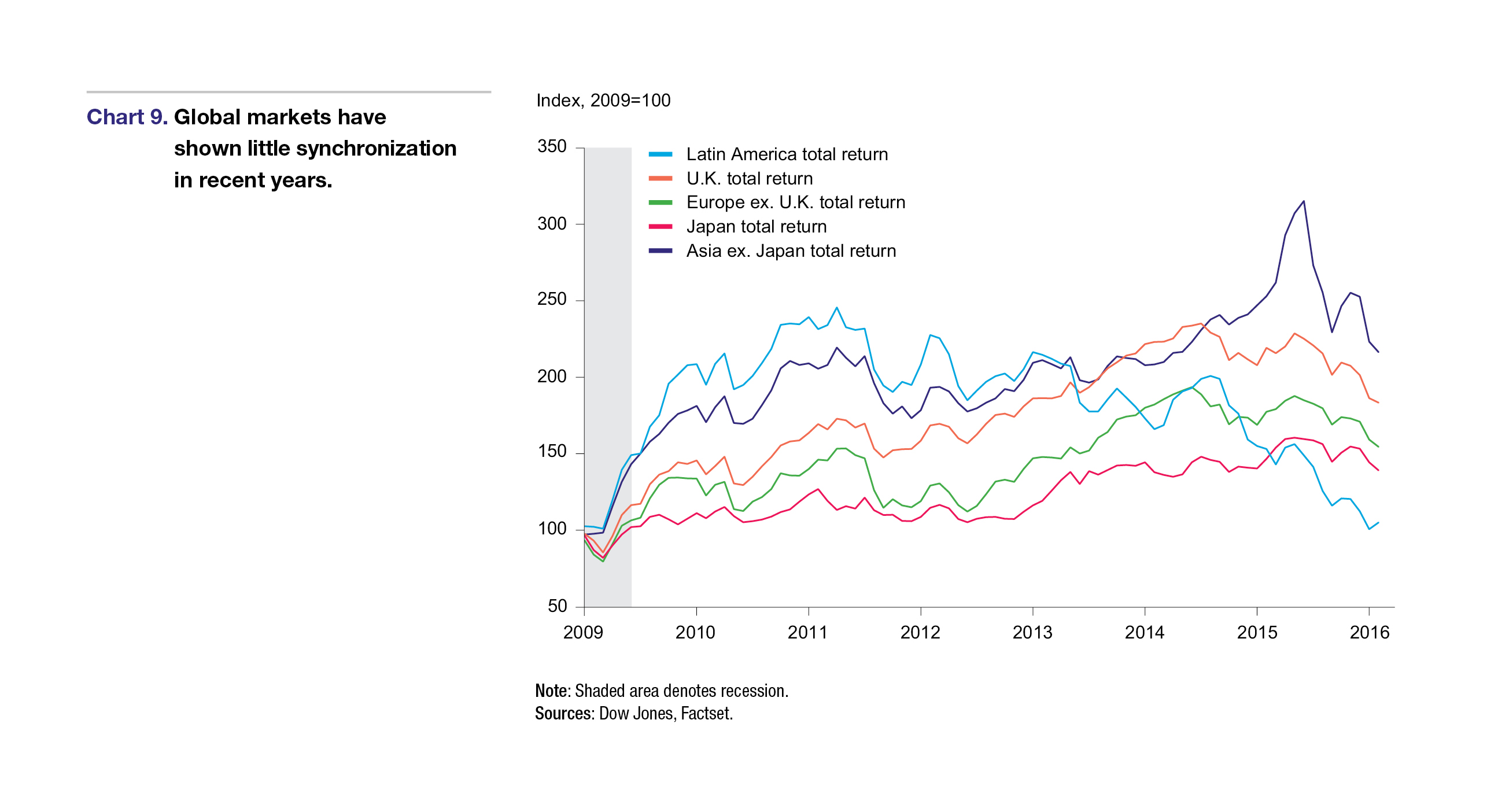

Global synchronization—the idea that the business cycles in the world’s economies are becoming synchronized—was hotly debated in prior decades. But that issue seems to have been replaced by unconventional monetary policy, structural shifts in key economies like China, and fears of persistent slow global growth and deflation.

The apparent lack of synchronization presents some interesting questions. How should investors categorize foreign markets when developing an asset allocation? Is lumping all foreign markets together the best approach? Can we simply divide economies into developed and emerging markets? What about regions – Europe vs. Asia vs. Latin America? With many asset-allocation models breaking U.S. equities down by market cap and sometimes styles (growth vs. value), should these characteristics be applied to foreign markets as well?

Applying our U.S. business-cycle research to foreign economies would seem a natural extension of AIER’s long traditions. At some point, AIER may pursue this endeavor if our supporters are interested. In the meantime, investors should be aware of both the opportunities and risks associated with foreign markets, particularly with economies and markets performing very differently.

Next/Previous Section:

1.Overview

5. Investing

6. Pulling It All Together/Appendix