Inflation

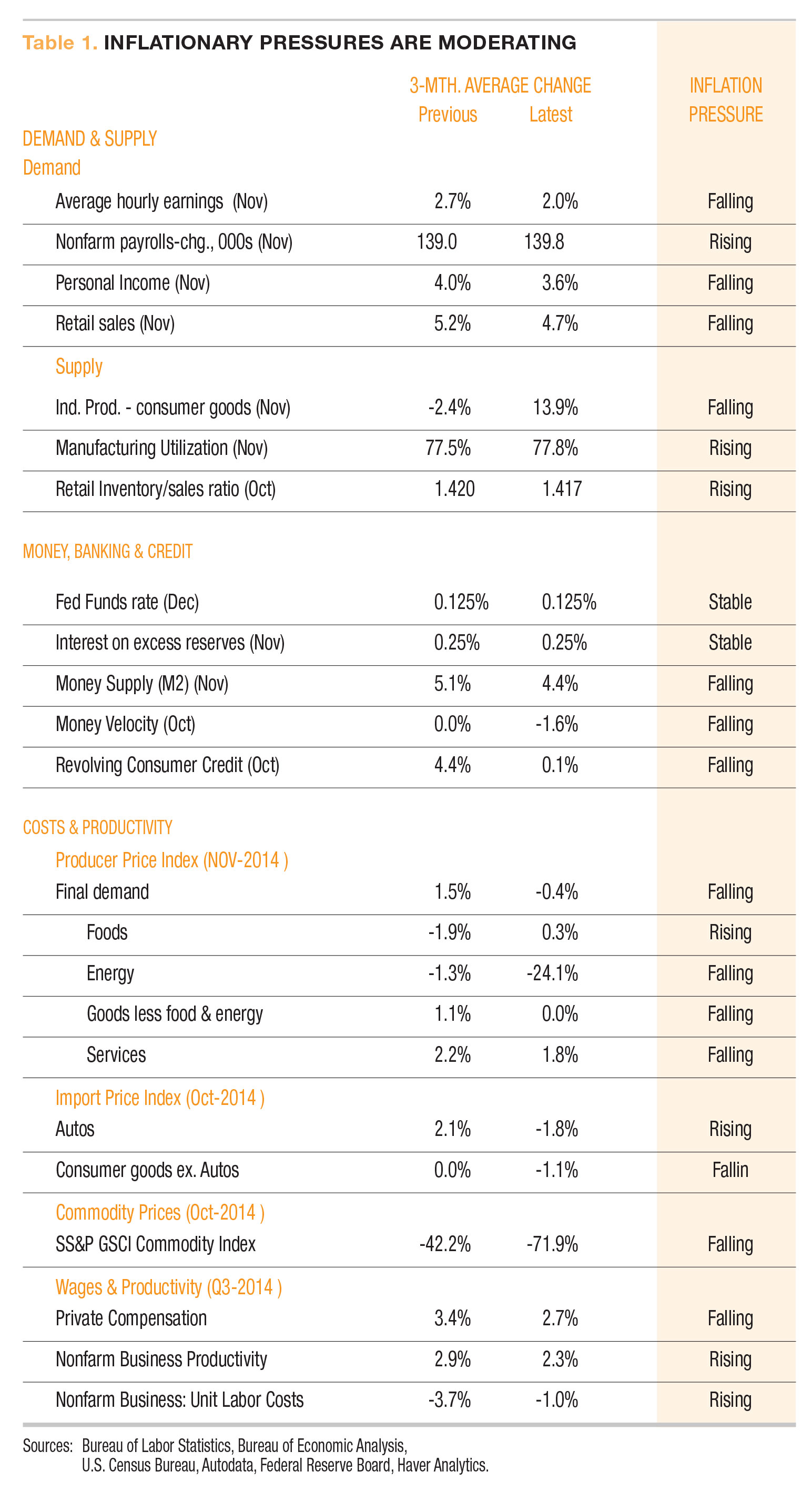

In our latest review, 14 of the 23 indicators show receding inflationary pressures, two are stable and seven show increases (Table 1). Overall, our scorecard suggests generally moderating inflationary pressures and supports our view that price gains are likely to remain tame in the months ahead. Two indicators in our scorecard, both in the Costs & Productivity section, reflect the sharp drop in energy prices. First, within Producer Price Index (PPI) data, the energy component of final demand declined far more steeply in the latest three months (-24.1 percent) compared with the prior three-month period (-1.3 percent). The collapse in oil can also be seen in the commodity price index indicator, which decreased at a 71.9 percent rate in the latest three months compared with a 42.2 percent slide in the prior three months. In both cases, these sharp drops should flow through to components of the CPI.

CPI

The Consumer Price Index (CPI) fell 0.3 percent in November as a sharp decline in energy costs offset small price increases in other goods and services. Over the past 12 months, the CPI has risen 1.3 percent, below a 2.3 percent 20-year average (Table 2). Because food and energy tend to be more volatile and subject to influences beyond typical economic forces such as severe weather patterns or geopolitical forces, we believe it’s important to analyze the core CPI as well. This gauge excludes food and energy and accounts for almost 77 percent of the total CPI. The core CPI rose 0.1 percent in November and 1.7 percent for the trailing 12 months. That’s 0.4 percentage points below the 2.1 percent average annual increase over the past 20 years.

We further break it down into core goods and core services in order to get a deeper understanding of price changes in the U.S. economy. Core goods have risen at an average annualized rate of just 0.3 percent over the past 20 years and are actually down 0.5 percent in the last 12 months. Core services have risen 2.7 percent over the past year and averaged 2.8 percent annual gains over the previous two decades. This significant long-term difference between core goods price changes (+0.3 percent) and core services price changes (+2.8 percent) is an important element in understanding the dynamics of consumer price increases. Core goods prices continue to benefit from gains in productivity as well as international trade, where lower labor costs increase competitive pressures on domestic producers. Services, however, tend to have lower productivity growth and are not easily replaced with foreign substitutes.

Offsetting this upward pressure on prices among services, some services may benefit from the recent decline in petroleum costs. The transportation industry including air travel and package delivery services may experience lower operating costs, which may be passed on to consumers through lower prices.

Energy Pulls the Everyday Price Index Down

AIER’s Everyday Price Index (EPI) decreased 1.2 percent in November. A drop in energy prices offset increases in prescription drugs and childcare services. On balance, food prices were unchanged in November. In contrast to the over 1 percent drop in the EPI, the CPI decreased 0.3 percent in November. The November pattern is different than the pattern over the past 12 months when the EPI rose 0.7 percent, approximately one half as much as the 1.3 percent gain in the CPI, primarily because gasoline makes a larger contribution to the EPI than it does to the CPI.

In November, energy prices fell 5.5 percent across the board. Only propane, kerosene and firewood registered increases. Regular grade gasoline sank 9.1 percent and both mid-grade and premium slid 8.1 percent. Food was unchanged in November because lower prices at grocery stores were offset by higher costs at restaurants. Prescription drug prices also gained for the month.

Next/Previous Section:

1. Overview

2. Economy

3. Inflation

4. Policy

5. Borrowing and Investing

6. Pulling It All Together/Appendix