Global Expectations Rising

The IMF also expects U.S. growth to accelerate in 2014 and 2015. That expectation is consistent with AIER’s research, led by our Business-Cycle Conditions (BCC) indicators, which finds that the outlook for economic growth in the U.S. remains positive. Continued gains in jobs and income are likely to support improving consumer spending and business investment, while stronger global growth will provide a tailwind for U.S. export growth. (See Statistical Indicators of Business-Cycle Changes.)

Raised Sights

The WEO Update shows that IMF expectations for global growth in 2014 were revised up by 0.1 percent to 3.7 percent, while the 2015 estimate remains unchanged at 3.9 percent. These represent increases from the 3.0 percent seen in 2013.

The upward revision was driven primarily by expected growth in developed economies, where 2014 GDP estimates were lifted by 0.2 percent, on average, to 2.2 percent. Notably, the U.K. forecast was raised by 0.6 percent (to 2.4 percent), and Japan’s was boosted by 0.4 percent (to 1.7 percent). Both Germany and the U.S. saw upward revisions of 0.2 percent (to 1.6 percent and 2.8 percent, respectively).

Expectations for emerging economies in total were unchanged, as a downward revision of 1.0 percent for Russia (to 1.5 percent) was offset by upward revisions for China (0.3 percent to 7.5 percent) and India (0.2 percent to 5.4 percent).

Substantial Growth Expected

While the IMF has boosted its overall projection for 2014 world GDP growth, they lowered their sights slightly for growth in world trade volumes this year. The IMF now expects world trade volumes to rise by 4.5 percent in 2014, down slightly from the 5.0 percent gain in its prior forecast (Table 1), but still a large jump from the 2.7 percent seen in 2013.

Accelerating global growth and rising trade activity can only be expected to benefit U.S. exports and U.S. GDP growth, particularly if key U.S. trading partners are experiencing strong growth.

Read the SPECIAL SECTION: Primer on U.S. Trade

U.S. Outlook Remains Upbeat

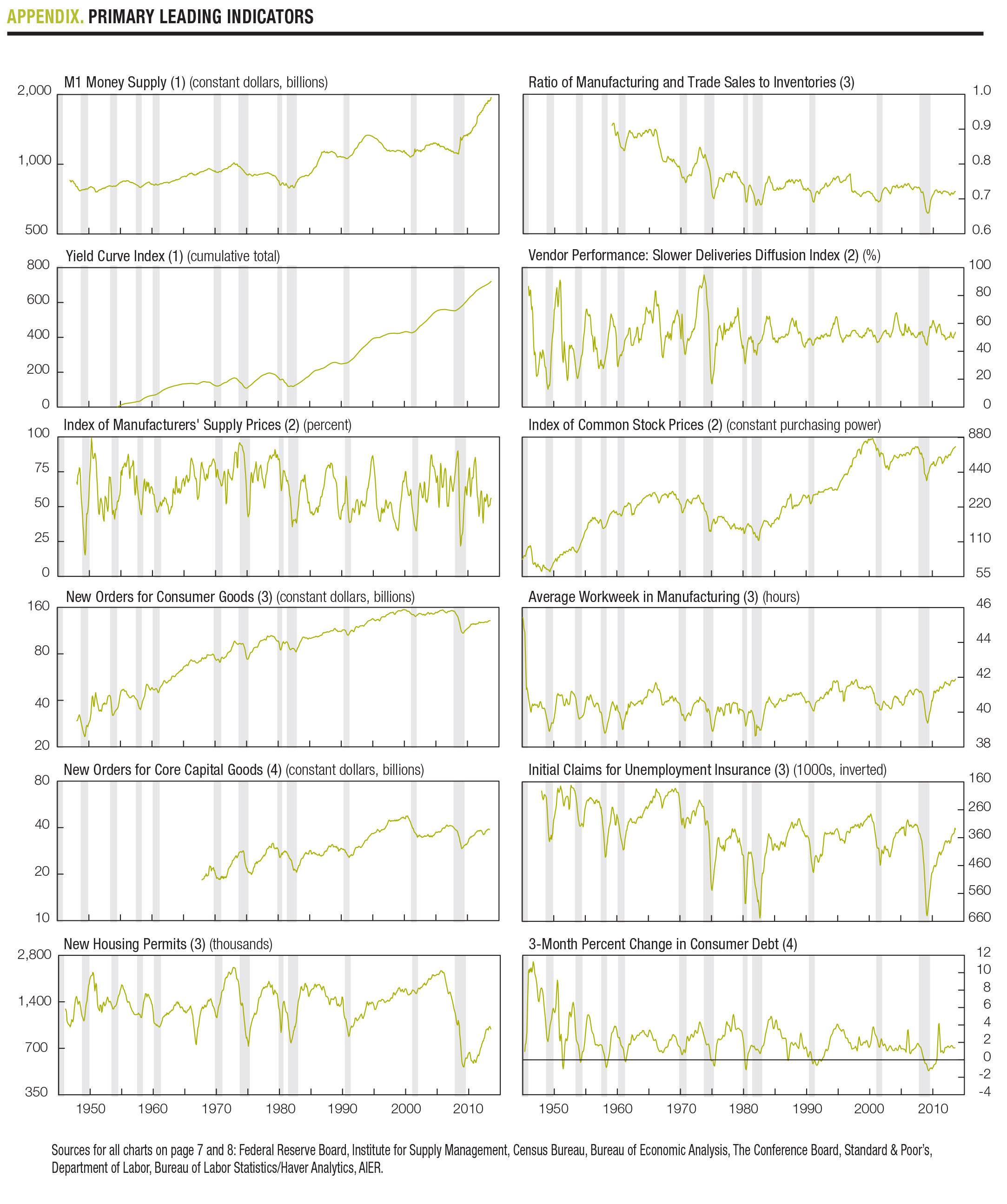

January is the fourth consecutive month of across-the-board 100 percent readings for the primary leading, coincident, and lagging indicators in our Business-Cycle Conditions index.

The cyclical score for the leading indicators, derived from a separate mathematical analysis, came in at a strong 90-out-of-100 reading in the latest month – up four points from 86 in the prior month (Chart 3).

Key takeaways from the latest readings of AIER’s BCC indicators include:

Leading: Among the leading indicators, nine were judged to have a positive trend in January. An impressive five of those nine hit new cycle highs in December: M1 money supply, the index of common stock prices, the yield curve index, the average workweek in manufacturing, and new orders for consumer goods.

Coincident: All six of our coincident indicators show positive trends, resulting in a perfect 100 reading for the 25th month in a row. Four of the six registered new highs in December: nonagricultural employment, the index of industrial production, manufacturing and trade sales, and gross domestic product.

Lagging: AIER’s index of lagging indicators posted its 21st straight month of perfect 100 readings. Among the individual indicators, December marked new highs for commercial and industrial loans, manufacturing and trade inventories, and the ratio of consumer debt to income.

In aggregate: In all, 12 of our 24 indicators hit new cycle highs last month.

Lagging: AIER’s index of lagging indicators posted its 21st straight month of perfect 100 readings. Among the individual indicators, December marked new highs for commercial and industrial loans, manufacturing and trade inventories, and the ratio of consumer debt to income.

In aggregate: In all, 12 of our 24 indicators hit new cycle highs last month.

Taken together, the AIER’s Business-Cycle Conditions indicators point to strong economic momentum and suggest continued economic expansion in early 2014. We see job and wage gains in the U.S. combining with rising household wealth – reflecting gains in equity prices and recovering home prices – to support growing consumer spending over the next few quarters. Gains in spending, in turn, should drive increased business investment, additional job creation, and further wage gains.

Risks Never Far Away

While our view is generally optimistic, there are, as always, risks to the outlook for both the U.S. economy and the global economy.

In the U.S., the risks include cautious consumers who are resistant to taking on debt, a shaky housing market, and a policy mistake, either monetary or fiscal. Globally, European growth remains very fragile, and the continent continues to be under a threat of deflation. The European banking system is under heightened scrutiny, particularly with regard to capital standards. Furthermore, in Europe the institutional capacity (i.e., regulatory structures and ECB authority) to deal with additional banking system crises is more limited than here in the U.S. Meanwhile, emerging markets are at risk of capital outflows potentially leading to weakening currencies, higher inflationary pressures, and rising interest rates.

Despite these risks, our research suggests that the U.S. economy is on track for improving economic conditions over the next several months.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals. Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.