Economy

Stronger economic growth could lead to greater private investment in structures.

Private investment Private investment in nonresidential structures covers a wide range of building types. The U.S. Census Bureau reports monthly on spending for 11 categories of nonresidential structures such as hotels, hospitals, airports, and schools. Among those 11 categories, four dominate: commercial (primarily retail), office buildings, power structures (gas, oil, and electric), and manufacturing plants (Chart 2). Combined, these four accounted for about 70 percent of private-structure spending in 2016.

Among these four, spending on commercial, office, and manufacturing facilities fell following the Great Recession. Power structures showed some smaller declines but generally trended upward (Chart 3). The three categories that suffered big declines have already posted solid rebounds. All four, as well as many lesser categories, should benefit from an improving economy and better profit growth.

More infrastructure spending is likely to be a public priority.

Public investment Infrastructure spending, an important part of overall investment in structures, is dominated by capital spending on education (classrooms, dorms, and athletic facilities, for example) and highway spending. Combined, education and highways account for about 57 percent of infrastructure spending. Adding transportation facilities (such as terminals, runways, and railroad tracks) and sewage treatment plants brings the total to about 76 percent of total public spending on structures (Chart 4). Highway and transportation spending are primarily federal programs, while education structures and sewage plants are typically paid for by state and local governments.

Several challenges face public infrastructure spending: politics perhaps not yielding optimal allocation among projects; improper bidding; waste and cost overruns; and long lead times. Those issues aside, increased public infrastructure spending is likely to be a priority in coming quarters.

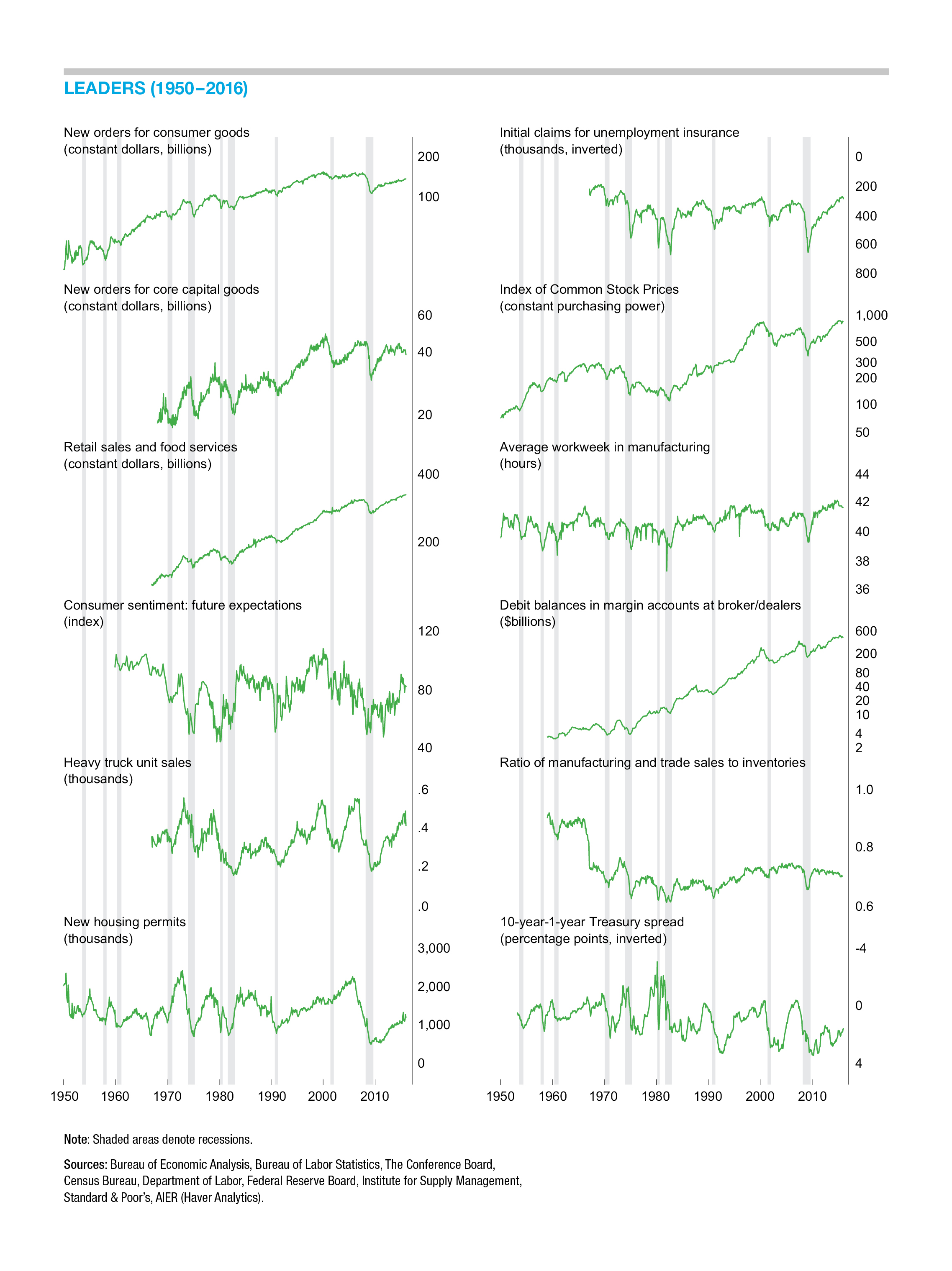

Economic Outlook

Our Business-Cycle Conditions Leaders index increased again in the latest month, rising to 75 in December, the highest level since 2014 and up from 67 in November (Chart 6). December also marks the first four-month stretch above the neutral 50 level for the Leaders since the end of 2015.

Among our 12 Leaders, seven are trending higher, four are trending flat, and just one is trending lower. Those trending higher are: initial claims for unemployment insurance, real retail sales, manufacturing and trade sales to inventories, consumer expectations, residential housing permits, real stock prices, and real debit balances in margin accounts. Flat trends have been identified in real new orders for consumer goods, real new orders for capital goods, the Treasury-yield spread, and the average workweek in manufacturing (hours). The lone decliner is real heavy-truck unit sales.

While the improvement in our Leaders index provides further evidence that the risk of recession in the near term has diminished significantly, we do not expect a sharply different pace of growth. Growth during the current recovery has been below its historical average. While new fiscal policy such as tax cuts and/or higher spending has the potential to boost growth in the short term, headwinds persist, such as unfavorable demographics, low productivity growth, and weak global growth.

Among our other indexes, the Coinciders retreated a bit to 83 in December from 92 in November while the Laggers held steady at 75 in the latest month.

Next/Previous Section:

1. Overview

2. Economy

3. Inflation

4. Policy

5. Investing